pt bank permata tbk

TRANSCRIPT

Analyst Presentation

Prepared by Investor Relations

PT BANK PERMATA Tbk September 2020 Financial Result

as of 02 November 2020

Disclaimer Laporan ini disusun oleh PT Bank Permata Tbk secara independen dan diedarkan hanya untuk tujuan informasi

umum. Hal ini tidak dimaksudkan untuk orang tertentu yang mungkin menerima laporan ini. Informasi dalam laporan

ini telah diperoleh dari sumber-sumber yang kami anggap dapat dipercaya. Tidak ada jaminan (tersurat maupun

tersirat) yang dibuat untuk keakuratan atau kelengkapan informasi. Semua pendapat dan perkiraan yang termasuk

dalam laporan ini merupakan penilaian kami pada tanggal ini dan dapat berubah tanpa pemberitahuan sebelumnya.

Kami tidak bertanggung jawab atau memiliki kewajiban apa pun tanpa pemberitahuan sebelumnya dari PT Bank

Permata Tbk dan / atau karyawan dan / atau agen mereka masing-masing yang timbul yang dapat dibawa atau

diderita oleh orang lain sebagai akibat bertindak atas dasar seluruh atau sebagian dari isi laporan ini. Baik PT Bank

Permata Tbk dan / atau perusahaan afiliasinya dan / atau karyawan dan / atau agennya masing-masing tidak

bertanggung jawab atas kesalahan, kelalaian dalam laporan ini dan setiap ketidakakuratan atau kelalaian yang

mungkin timbul.

This report has been prepared by PT Bank Permata Tbk independently and is circulated for the purpose of general

information only. It is not intended to the specific person who may receive this report. The information in this report

has been obtained from sources which we deem reliable. No warranty (expressed or implied) is made to the

accuracy or completeness of the information. All opinions and estimations included in this report constitute our

judgment as of this date and are subject to change without prior notice.

We disclaim any responsibility or liability without prior notice of PT Bank Permata Tbk and/or their respective

employees and/or agents whatsoever arising which may be brought against or suffered by any person as a result of

acting in reliance upon the whole or any part of the contents of this report and neither PT Bank Permata Tbk and/or

its affiliated companies and/or their respective employees and/or agents accepts liability for any errors, omissions,

negligent or otherwise, in this report and any inaccuracy herein or omission here from which might otherwise arise.

Presentation Content

3

PERMATA BANK IN BRIEF 2

MACRO ECONOMY UPDATES 1

BUSINESS UPDATE 4

FINANCIAL PERFORMANCE HIGHLIGHTS 3

OTHER INFORMATION 5

14,245 13,700

16,825

15,669

14,231

14,780 14,543

14,554 14,951

30

-Se

p-1

9

31

-Oct

-19

30

-No

v-1

9

31

-De

c-1

9

31

-Jan

-20

29

-Fe

b-2

0

31

-Ma

r-2

0

30

-Ap

r-2

0

31

-Ma

y-2

0

30

-Ju

n-2

0

31

-Ju

l-2

0

31

-Au

g-2

0

30

-Se

p-2

0

USD/IDR

3.39%

3.00% 2.98%

1.54%1.32% 1.42%

2.0%

4.0%

Sep

-19

Oct

-19

No

v-1

9

Dec

-19

Jan-

20

Feb

-20

Mar

-20

Ap

r-20

May

-20

Jun

-20

Jul-

20

Au

g-20

Sep

-20

Inflation (yoy)

Macro Economy Decreasing interest rate to boost domestic growth

Rupiah is weakened since Feb-20, due to Covid-19 outbreak

Deflation trend and already below BI target

GDP Growth is starting rebound

low range target

high range target

5.25%5.00%

4.75%4.50%

4.50%4.00% 4.00%

Sep

-19

Oct

-19

Nov

-19

De

c-1

9

Jan

-20

Feb

-20

Mar

-20

Ap

r-2

0

May

-20

Jun

-20

Jul-2

0

Jul-2

0

Au

g-2

0

Sep

-20

7 Days Reverse Repo rate

5.17% 5.18% 5.07% 5.05% 5.02% 4.97%

2.97%

-5.32%

-3.0% est.

Q3-18 Q4-18 Q1-19 Q2-19 Q3-19 Q4-19 Q1-20 Q2-20 Q3-20

4

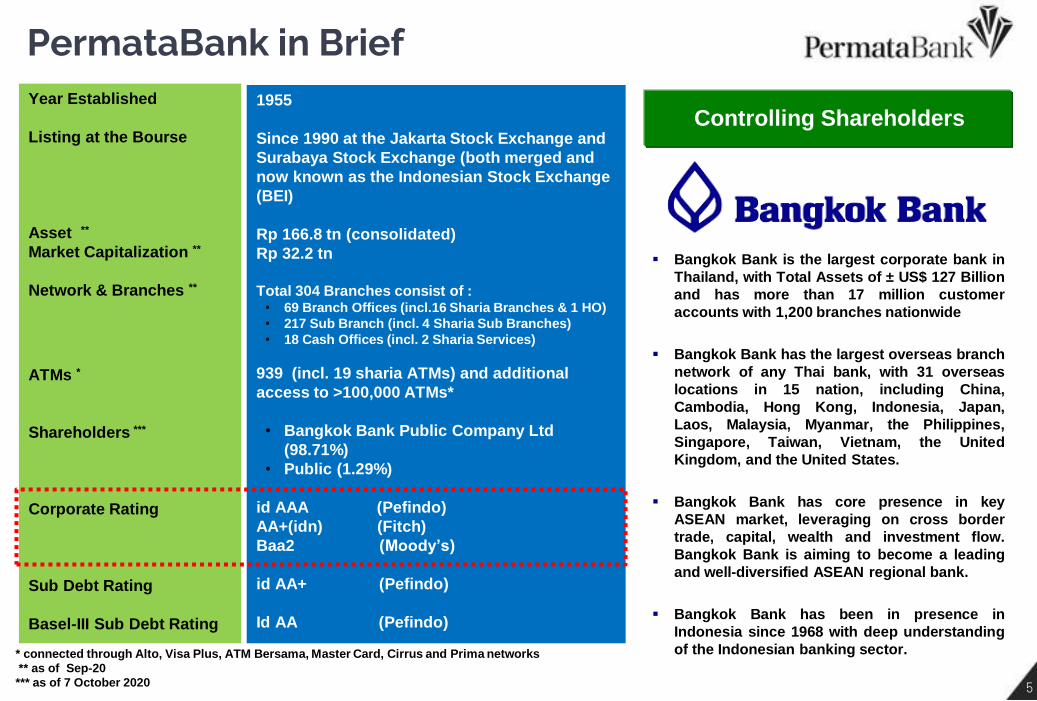

PermataBank in Brief Year Established

Listing at the Bourse

Asset **

Market Capitalization **

Network & Branches **

ATMs *

Shareholders ***

Corporate Rating

Sub Debt Rating

Basel-III Sub Debt Rating

1955

Since 1990 at the Jakarta Stock Exchange and

Surabaya Stock Exchange (both merged and

now known as the Indonesian Stock Exchange

(BEI)

Rp 166.8 tn (consolidated)

Rp 32.2 tn

Total 304 Branches consist of :

• 69 Branch Offices (incl.16 Sharia Branches & 1 HO)

• 217 Sub Branch (incl. 4 Sharia Sub Branches)

• 18 Cash Offices (incl. 2 Sharia Services)

939 (incl. 19 sharia ATMs) and additional

access to >100,000 ATMs*

• Bangkok Bank Public Company Ltd

(98.71%)

• Public (1.29%)

id AAA (Pefindo)

AA+(idn) (Fitch)

Baa2 (Moody’s)

id AA+ (Pefindo)

Id AA (Pefindo)

Bangkok Bank is the largest corporate bank in

Thailand, with Total Assets of ± US$ 127 Billion

and has more than 17 million customer

accounts with 1,200 branches nationwide

Bangkok Bank has the largest overseas branch

network of any Thai bank, with 31 overseas

locations in 15 nation, including China,

Cambodia, Hong Kong, Indonesia, Japan,

Laos, Malaysia, Myanmar, the Philippines,

Singapore, Taiwan, Vietnam, the United

Kingdom, and the United States.

Bangkok Bank has core presence in key

ASEAN market, leveraging on cross border

trade, capital, wealth and investment flow.

Bangkok Bank is aiming to become a leading

and well-diversified ASEAN regional bank.

Bangkok Bank has been in presence in

Indonesia since 1968 with deep understanding

of the Indonesian banking sector. * connected through Alto, Visa Plus, ATM Bersama, Master Card, Cirrus and Prima networks

** as of Sep-20

*** as of 7 October 2020

Controlling Shareholders

5

6

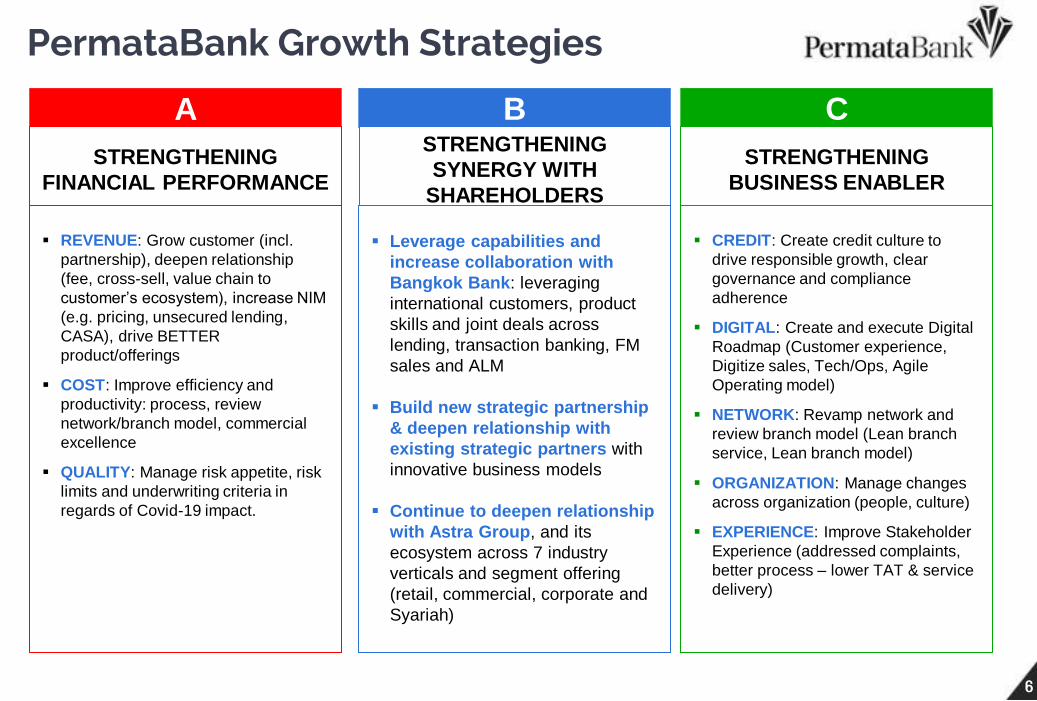

PermataBank Growth Strategies

6

REVENUE: Grow customer (incl.

partnership), deepen relationship

(fee, cross-sell, value chain to

customer’s ecosystem), increase NIM

(e.g. pricing, unsecured lending,

CASA), drive BETTER

product/offerings

COST: Improve efficiency and

productivity: process, review

network/branch model, commercial

excellence

QUALITY: Manage risk appetite, risk

limits and underwriting criteria in

regards of Covid-19 impact.

A

Leverage capabilities and

increase collaboration with

Bangkok Bank: leveraging

international customers, product

skills and joint deals across

lending, transaction banking, FM

sales and ALM

Build new strategic partnership

& deepen relationship with

existing strategic partners with

innovative business models

Continue to deepen relationship

with Astra Group, and its

ecosystem across 7 industry

verticals and segment offering

(retail, commercial, corporate and

Syariah)

B

CREDIT: Create credit culture to

drive responsible growth, clear

governance and compliance

adherence

DIGITAL: Create and execute Digital

Roadmap (Customer experience,

Digitize sales, Tech/Ops, Agile

Operating model)

NETWORK: Revamp network and

review branch model (Lean branch

service, Lean branch model)

ORGANIZATION: Manage changes

across organization (people, culture)

EXPERIENCE: Improve Stakeholder

Experience (addressed complaints,

better process – lower TAT & service

delivery)

C

STRENGTHENING

FINANCIAL PERFORMANCE

STRENGTHENING

SYNERGY WITH

SHAREHOLDERS

STRENGTHENING

BUSINESS ENABLER

Financial Performance

Financial Performance Highlights

• LOAN GROWTH – Slightly declined by -4.3% (YoY) to Rp.102.9 Trillion in Q3-20 in line with the decline in

credit demand due to the economic downturn as a result of COVID-19 outbreak. Bank continues to selectively

provide loan for customers and industrial sectors that are not affected by COVID-19 which predicted be able to

sustain in accordance with the Bank’s appetite and principle of prudence to maintain the quality of the loan.

• RESTRUCTURED LOAN – As of September 2020, the total requests for the Restructuring and Credit

Relaxation program related to COVID-19 received by Permata Bank amounted to IDR 11.97 trillion or 11.6%

of the total credit in Sep 2020, of which 91% have been approved and booked. Bank continues to focus on

helping affected debtors by carrying out loan restructuring and relaxation programs in accordance with OJK

direction.

• THIRD PARTY FUND – Total third party fund grew by 11.1% to Rp. 133.3 trillion, which majorly was

supported by CA and SA growth of 18.3% and 8.2%, resp., led to an increase in CASA by 13.4%. CASA ratio at

51% which showing that PemataBank continues to play an important role in supporting customers to manage

their business in difficult economic conditions. As of Sep-20, LDR was also well maintained at 74.5%.

• MANAGEABLE ASSET QUALITY WITH PRUDENT COVERAGE RATIO – The gross NPL ratio

increased to 3.8% compared to Sep 2019 which was 3.3% with NPL-net maintained at a level of 1.5%

compared to Sep 2019 position of 1.2%. This was influenced by the impact of the COVID-19 pandemic on the

financial capacity of debtors in almost all industry segments.

• THE NPL COVERAGE RATIO – Well maintained at 118% in Sep 2020, an increase compared to Jun

2020 position of 112%. This is in line with the efforts to improve credit quality that have been made while

maintaining conservatism and indicate the Bank's efforts to mitigate potential credit losses in a prudent manner.

8

Financial Performance Highlights

• REVENUE GROWTH – Pre Provision Operating Profit (PPOP) was recorded at IDR 2.6 Trillion or grew by

20.4% (YoY) compared to the same period last year, which was mainly contributed by an increase in Net

Interest Income of 8.6% (YoY) to IDR 4.7 Trillion by end Q3-20 and also the Operating Income other than

Interest (Fee Based Income) increased by 9.0% to IDR 1.6 Trillion. This led to the achievement of the NIM ratio

to 4.4% or an increase of 19bps compared to the position in Sep 2019 of 4.2%. Meanwhile the Fee Income to

Income (FIR) ratio was maintained at the level of 25.1%, increasing by 11bps compared to the position in Sep

2019 of 25.0%.

• OPERATIONAL COST – Business efficiency has continuously improved with the achievement of the Cost to

Income Ratio (CIR) of 59.8%, a significant improvement compared to last year position of 63.6%. This is

achieved through effective cost management efforts combined with the use of technology and digitized

transaction in enabling the Bank to be more adaptive during COVID-19 pandemic and continuously serving

potential customers effectively.

• NET INCOME - The increase in credit provision expenses and the effect of changing in Corporate Income Tax

rates has significantly affected the Bank's profits, however, up to Q3-20 the Bank still booked Profit After Tax of

Rp.430 billion, downed by 60.7% compared to last year's achievement. Normalized Profit After Tax (exclude LI

impact of COVID-19 and changing in CIT from 25% to 22%) will be approx. Rp.806 billion.

• STRONG LIQUIDTY - Common Equity Tier 1 (CET-1) and Capital Adequacy Ratio (CAR) were

maintained firmly in the position of Sep 2020 at 20.5% and 21.6%, respectively, an increase compared to 18.6%

and 19.8% in the period same year ago - much higher than the applicable minimum capital requirement. The

capital ratio even remained strong after incorporating the impact of the first implementation of PSAK 71

regarding the provision for losses of financial instruments effective from Jan 1, 2020.

9

Key Financial Highlights

Sep 2019 Sep 2020 ∆ (%)

Loans (Rp Tn) 107,6 → 102.9 -4.3%

Gross NPL Ratio

Net NPL Ratio

NPL Coverage Ratio

3.3%

1.2%

164%

→

→

→

3.8%

1.5%

118%

0.5%

0.3%

-46%

CASA Ratio

[CASA (Rp Tn)]*

50%

59.7

→

→ 51%

68

0.8%

13.4%

LDR 88% → 74.5% -13.5%

NIM 4.2% → 4.4% 0.2%

BOPO 87.2% → 92% 4.8%

CIR 62% → 60% -3.8%

Profit Before Tax (Rp Bn) 1,463 → 833 -43%

Profit After Tax (Rp Bn)

Profit After Tax (Rp Bn)**

1,093

1,093

→

→

430

806

-61%

-26%

Notes : * Including Sharia deposits

** Excluding the COVID-19 impact on the increasing allowance for impairment asset and the effect of decreasing CIT – PPh from 25% to 22%

Source : Published Report (Consolidated) 10

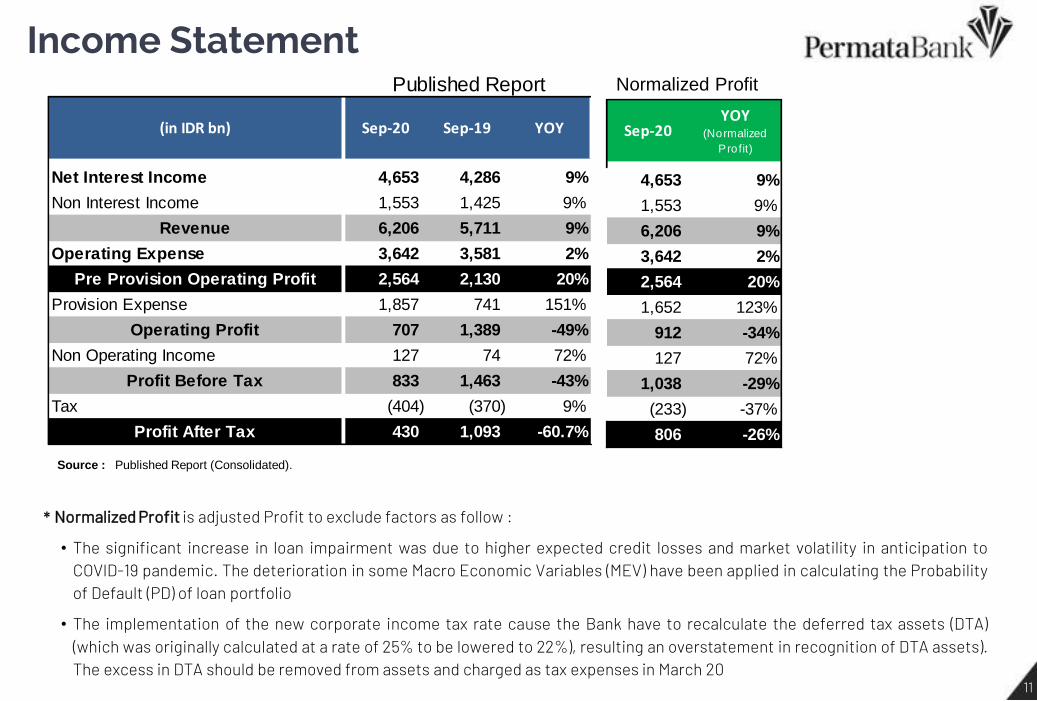

Income Statement

Source : Published Report (Consolidated).

* Normalized Profit is adjusted Profit to exclude factors as follow :

• The significant increase in loan impairment was due to higher expected credit losses and market volatility in anticipation to COVID-19 pandemic. The deterioration in some Macro Economic Variables (MEV) have been applied in calculating the Probability of Default (PD) of loan portfolio

• The implementation of the new corporate income tax rate cause the Bank have to recalculate the deferred tax assets (DTA) (which was originally calculated at a rate of 25% to be lowered to 22%), resulting an overstatement in recognition of DTA assets). The excess in DTA should be removed from assets and charged as tax expenses in March 20

Normalized Profit

Net Interest Income 4,653 4,286 9%

Non Interest Income 1,553 1,425 9%

Revenue 6,206 5,711 9%

Operating Expense 3,642 3,581 2%

Pre Provision Operating Profit 2,564 2,130 20%

Provision Expense 1,857 741 151%

Operating Profit 707 1,389 -49%

Non Operating Income 127 74 72%

Profit Before Tax 833 1,463 -43%

Tax (404) (370) 9%

Profit After Tax 430 1,093 -60.7%

(in IDR bn)

Published Report

YOYSep-20 Sep-19

4,653 9%

1,553 9%

6,206 9%

3,642 2%

2,564 20%

1,652 123%

912 -34%

127 72%

1,038 -29%

(233) -37%

806 -26%

Sep-20YOY

(Normalized

Profit)

11

Balance Sheet

Source : Published Report (Consolidated) Notes : * Including Reverse repo

** Including Sharia deposits

Cash 1.6 1.8 -11.9% 2.3 -31%

Placement with Bank Indonesia 16.5 14.8 11.5% 16.3 1%

Placement with Other Banks 4.0 7.3 -45.2% 9.6 -58%

Marketable Securities * 34.4 16.8 104.7% 11.9 190%

Loans (gross) 102.9 107.6 -4.3% 108.2 -5%

Allowance for Loan Impairment Losses (4.5) (5.8) -22.7% (3.9) 14%

Other Assets 12.0 12.7 -5.9% 17.2 -31%

Total Assets 166.8 155.1 7.5% 161.5 3%

Deposits ** 133.3 120.0 11.1% 122.9 8%

- Current Accounts 36.4 30.7 18.3% 32.4 12%

- Saving Accounts 31.3 29.0 8.2% 29.8 5%

- Time Deposits 65.7 60.3 8.9% 60.7 8%

Subordinated Debt 1.6 4.2 -62.5% 2.3 -31%

Others Liabilities 7.8 7.3 7.6% 12.3 -36%

Total Liabilities 142.7 131.4 8.6% 137.5 4%

Shareholders' Equity 24.1 23.7 1.5% 24.0 0%

Total Liabilities & Shareholders' Equity 166.8 155.1 7.5% 161.5 3%

(in IDR tn) Sep-20 Sep-19 YoY Dec-19 YTD

12

Financial Ratios

Source: Published and Management Report (Bank only)

Note: CASA Ratio includes Sharia deposits

CET-1 ratio 20.5 18.7 18.6 2.0

Total CAR 21.6 19.9 19.8 1.8

Loan to Deposit Ratio (LDR) 75 86 88 -13

CASA Ratio 51 51 50 1

ROA 0.7 1.3 1.3 -0.6

ROE 2.7 7.2 7.1 -4.5

BOPO 92 87 87 5

CIR 60 62 64 -4

NIM 4.4 4.4 4.2 0.2

NPL Gross 3.8 2.8 3.3 0.4

NPL Net 1.5 1.3 1.2 0.3

NPL Coverage ratio 118 133 164 -45

∆(in %) Sep-20 Dec-19 Sep-19

13

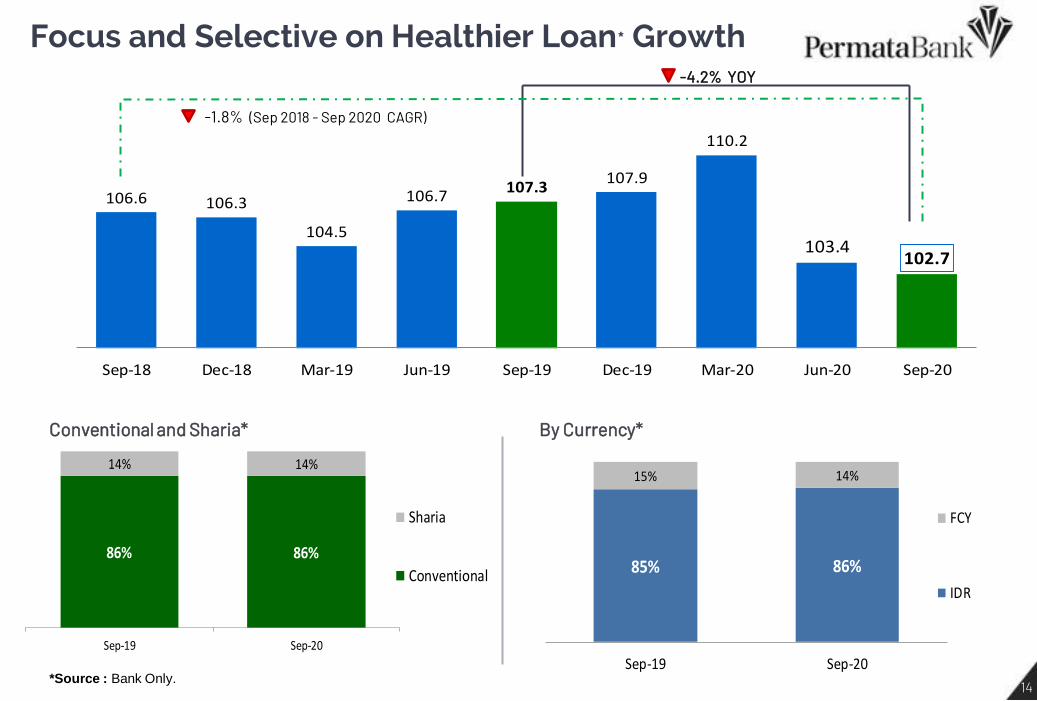

86% 86%

14% 14%

Sep-19 Sep-20

Sharia

Conventional

106.6 106.3

104.5

106.7107.3

107.9

110.2

103.4102.7

Sep-18 Dec-18 Mar-19 Jun-19 Sep-19 Dec-19 Mar-20 Jun-20 Sep-20

Focus and Selective on Healthier Loan* Growth

By Currency* Conventional and Sharia*

-4.2% YOY

-1.8% (Sep 2018 - Sep 2020 CAGR)

*Source : Bank Only.

85% 86%

15% 14%

Sep-19 Sep-20

FCY

IDR

14

164%

133%118%

168%

146% 145%

3.3%2.8%

3.8%

1.2% 1.3% 1.5%0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

20.0%

0%

30%

60%

90%

120%

150%

180%

210%

240%

Sep-19 Des-19 Sep-20

NPL Coverage Ratio Regulatory Coverage Ratio

Gross NPL ratio Net NPL

4.6% 4.6%4.3%

4.8%4.4%

3.8% 3.6%3.3%

2.8%3.2%

3.7% 3.8%

1.7% 1.7% 1.5% 1.7% 1.7% 1.6%1.3% 1.2% 1.3% 1.2%

1.8%1.5%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

Dec-17 Mar-18 Jun-18 Sep-18 Dec-18 Mar-19 Jun-19 Sep-19 Dec-19 Mar-20 Jun-20 Sep-20

Gross NPL

Net NPL

Loan Quality Weakened due to COVID-19

Loan by Collectability (% to total Loan) NPL Coverage Ratio (%)

Source : Published and Management Report (Bank Only)

+48 bps YOY

89.4% 91.2% 90.8%

7.3% 6.0% 5.5%

3.3% 2.7% 3.8%

Sep-19 Des-19 Sep-20

NPL

Coll.2

Coll.1

15

Restructured Loan Progress due to COVID-19

As per Sep 2020, total incoming requests (exclude cancel request) is at IDR 11.9tn, of which 90% is already

approved, 3% still in process and 7% rejected.

11.6%

88.4%

Loan Restructured & Relaxation

Non-Restructured & Non-Relaxed Loan

47%

33%

20%

Wholesale Banking

Retail Banking (excl. SME)

SME

90%

3% 7%

Approved On Progress Rejected

Loan Affected by Covid-19

IDR 11.9 Trillion Request for Restructuring & Relaxation

or 11.6% of Total Loan – Sep 2020

Restructuring Progress

90% Approved, 7% Rejected, 3% On progress

Restructuring by Segment

47% WB, 33% RB, 20% SME

16

Growth Deposit, focus on CASA Deposit Composition (IDR Trillion)

By Currencies CASA Ratio (%)

1.3 % (YTD)

11.1% YOY

Source : Published and Management Report

0.10 bps (YOY)

• The third party funds balances increased

by 11.1% from Sep-19 to Sep-20, mainly

driven by the increase in CASA by 13.4%

YoY.

• PB’s deposit strategy is continuously

focusing on low cost and sustainable funds

(CASA).

• The CASA percentage is maintained stable

at 51% in Sep-20 in line with PB’s deposit

strategy and in order to contribute a stable

NIM%.

+13%

YOY Growth %

+9%

59.7 62.3 67.7

60.3 60.7 65.7

120.0 122.9 133.3

Sep-19 Dec-19 Sep-20

CASA Time Deposits

50

51 51

Sep-19 Dec-19 Sep-20

84% 85% 83%

16% 15% 17%

Sep-19 Dec-19 Sep-20

IDR Non IDR

17

Increasing NIM and Overall Yield

• NIM ratio is 4.4% or increased by 28bps compared to the position of Sep-19 which is at 4.2%. Despite the uncertain

economy condition due to COVID-19, the Bank still continuously improving its NIM.

• The increase in NIM was mostly due contributed by decrease in the interest expense due to Bank’s subordinated

bond (Tier-2 Capital) and increase in CASA composition during the year. Both caused the cost of funds decrease

faster while the loan interest yield is slower to adjust following by its repricing period due to the decrease of BI rate

Source : Published and Management Report (Bank Only)

7.9% 8.0% 8.3% 8.4% 8.4% 8.4%8.1% 7.9% 7.6%

4.3% 4.3%4.8% 4.7% 4.6% 4.6%

4.0% 3.9%

3.8%4.0% 4.1% 4.0% 4.2% 4.2% 4.4% 4.6% 4.5%

4.4%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

Sep-18 Dec-18 Mar-19 Jun-19 Sep-19 Dec-19 Mar-20 Jun-20 Sep-20

Yield of Interest Earning Assets Cost of Interest Bearing Liabilities NIM

18

541 291

97 180 87 155 74

1,425

686

278 106 152 94 102 136

1,553

-

400

800

1,200

1,600

2,000

Net Gain andincr. value on

Mktbl Securitiestrx, Spot and

Derivative trx.

Loan RelatedFees

Trade Finance Bancassurance Security AgencyServices &Investment

Services

Credit Card & E-Channel

Others Total NonInterest Income

Sep-19 Sep-20

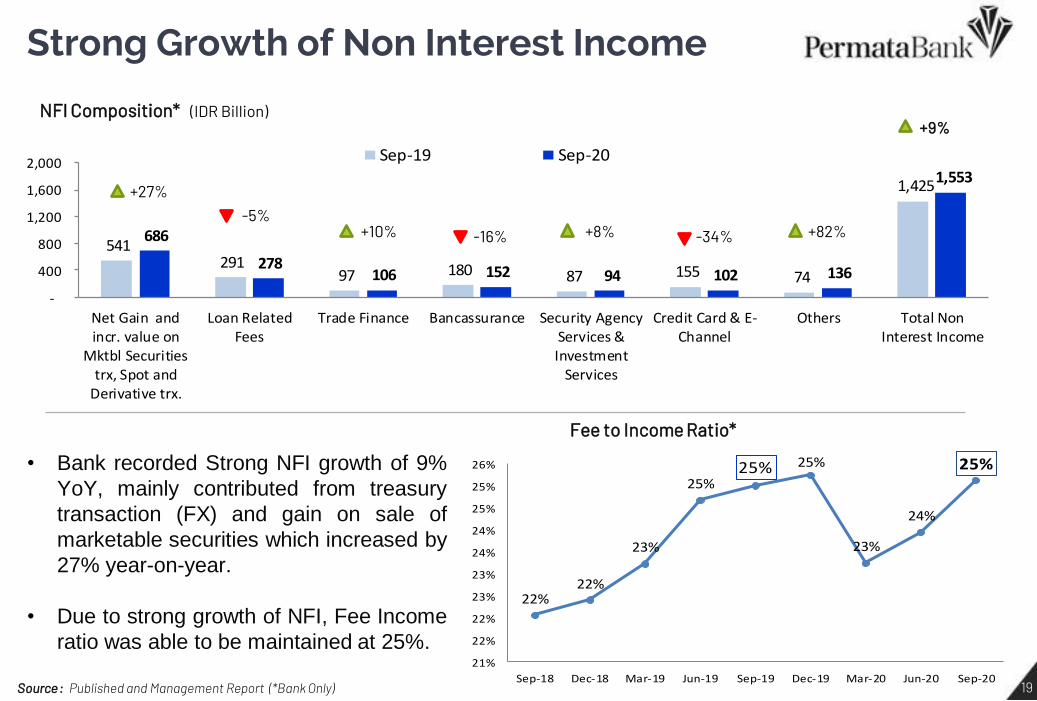

Strong Growth of Non Interest Income

NFI Composition* (IDR Billion)

Fee to Income Ratio*

+27% -5%

+10% -16% +82% -34%

+9%

+8%

Source : Published and Management Report (*Bank Only)

22%22%

23%

25%25% 25%

23%

24%

25%

21%

22%

22%

23%

23%

24%

24%

25%

25%

26%

Sep-18 Dec-18 Mar-19 Jun-19 Sep-19 Dec-19 Mar-20 Jun-20 Sep-20

• Bank recorded Strong NFI growth of 9%

YoY, mainly contributed from treasury

transaction (FX) and gain on sale of

marketable securities which increased by

27% year-on-year.

• Due to strong growth of NFI, Fee Income

ratio was able to be maintained at 25%.

19

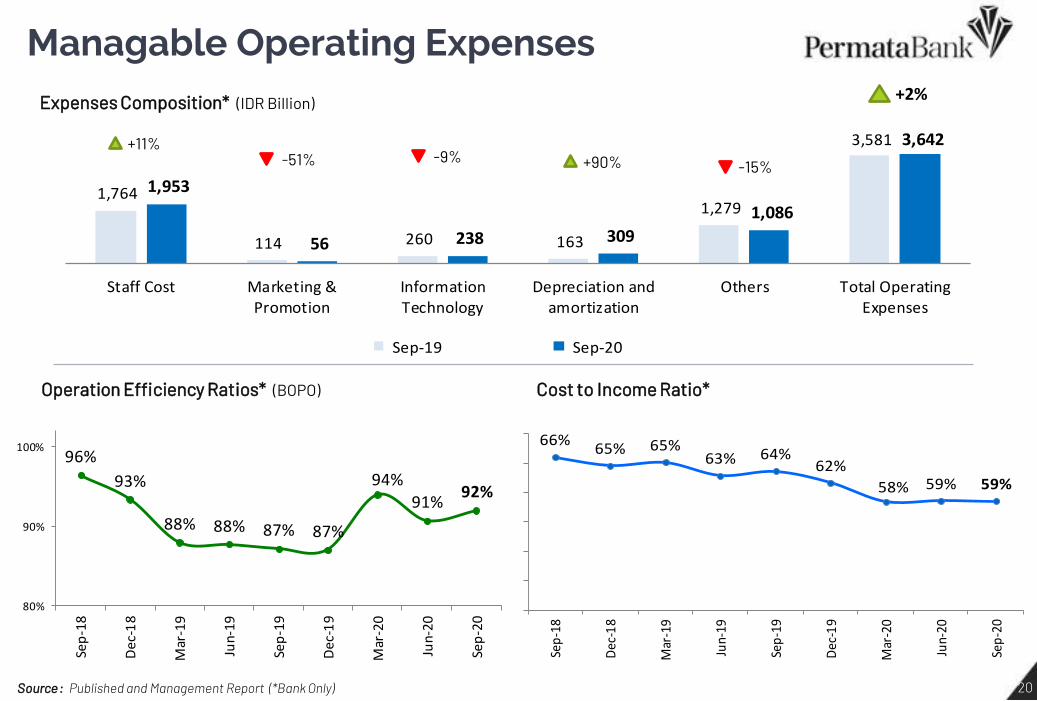

1,764

114 260 163

1,279

3,581

1,953

56 238 309

1,086

3,642

Staff Cost Marketing &Promotion

InformationTechnology

Depreciation andamortization

Others Total OperatingExpenses

Sep-19 Sep-20

Managable Operating Expenses

Expenses Composition* (IDR Billion)

Operation Efficiency Ratios* (BOPO)

+11% -51% -15% +90% -9%

+2%

Cost to Income Ratio*

Source : Published and Management Report (*Bank Only)

96%

93%

88% 88% 87% 87%

94%

91%92%

80%

90%

100%

Sep

-18

De

c-1

8

Mar

-19

Jun

-19

Sep

-19

Dec

-19

Mar

-20

Jun

-20

Sep

-20

66%65% 65%

63% 64%62%

58% 59% 59%

40%

45%

50%

55%

60%

65%

70%

Sep

-18

Dec

-18

Mar

-19

Jun-

19

Sep

-19

Dec

-19

Mar

-20

Jun-

20

Sep

-20

20

20.5

18.6

20.2

1.30.0 0.3 0.2 0.0 0.1

Sep-19 RWA Profit DTA MTM AFS Fixed AssetReval

Others Sep-20

Capital Position Remain Strong

Risk Weighted Asset (IDR Billion)

-4,7 % YOY +1.9% YOY

CET-1 Ratio (%)

19.8 19.9 19.6 21.3 21.6

18.6 18.7 18.4 20.2

20.5

12.5 12.5 12.5

10.0 10.0

Sep-19 Dec-19 Mar-20 Jun-20 Sep-20

Total CAR CET1 Minimum Requirement (incl. Buffer)

(3,249)(1,561) (341)

115,361 110,211

-

-

Sep-19 Credit Risk Market Risk OperationalRisk

Sep-2021

Business Updates

Retail Banking Business Strategy In 2020, PermataBank will focus on development of Consumer Loan products

FOCUS ON THE GROWTH OF PUBLIC AND CONSUMER FINANCING

INCREASING NON-INTEREST INCOME (FEE BASED)

IMPROVE RETAIL BUSINESS SCALE THROUGH COLLABORATING WITH NEW BUSINESS PARTNERS

MAINTAIN GOOD GOVERNANCE AND BUILD STRONG RISK MANAGEMENT

DOING DIGITALIZATION OF THE PROCESS FOR EFFICIENCY AND PRODUCTIVITY

CONTINUALLY DEVELOPING DIGITAL SOLUTIONS FOR CONSUMER AND SME NEEDS

The retail business strategy will focus on growing the number of customers, increasing third party funds, financing MSMEs / SMEs, digital transformation positioned to increase market share.

23

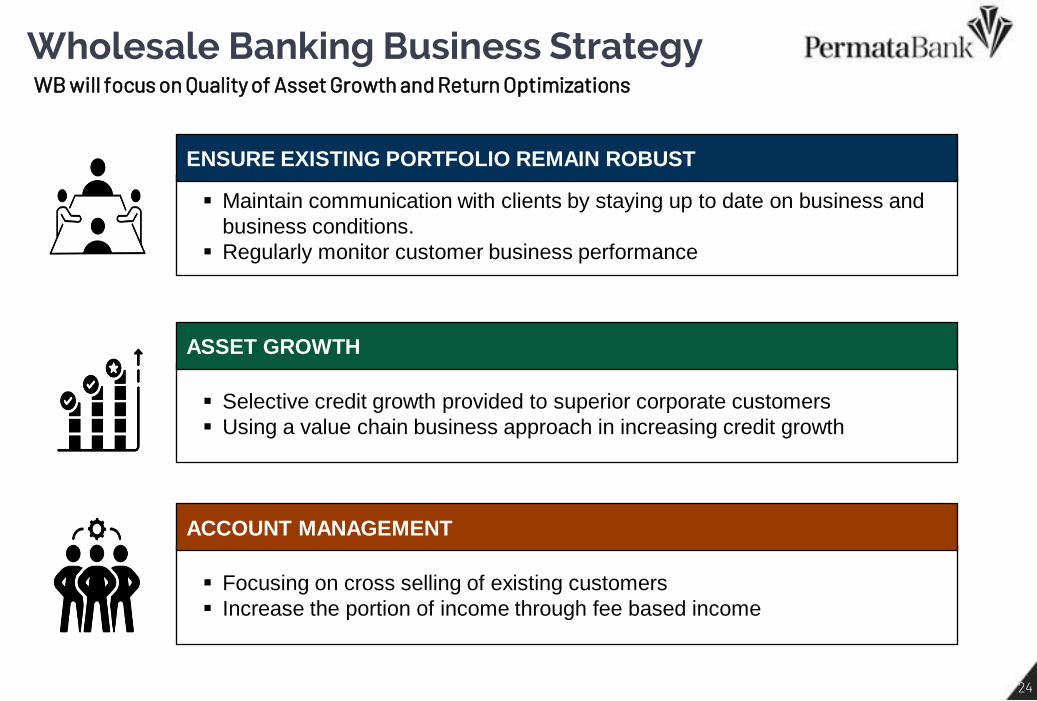

Wholesale Banking Business Strategy WB will focus on Quality of Asset Growth and Return Optimizations

Maintain communication with clients by staying up to date on business and

business conditions.

Regularly monitor customer business performance

ENSURE EXISTING PORTFOLIO REMAIN ROBUST

Selective credit growth provided to superior corporate customers

Using a value chain business approach in increasing credit growth

ASSET GROWTH

Focusing on cross selling of existing customers

Increase the portion of income through fee based income

ACCOUNT MANAGEMENT

24

Shariah Banking Business Strategy Key Achievements in 2020

25

We will continue to look at our data, draw insights,

identify area for improvement – experience,

stability, performance, new features, etc.

200+ FEATURES

PermataMobile X

LAUNCHED IN 2018

Permatabank.com

Designed to deliver experience that is consistent across all our digital platforms

LAUNCHED IN 2020

Permata Digital Branch

Version 1.23.1

Digital Banking Innovation Keep innovate and continuously improve to our customers

LAUNCHED IN 2019 26

PermataMobile X Powerful Digital Banking Platform

27

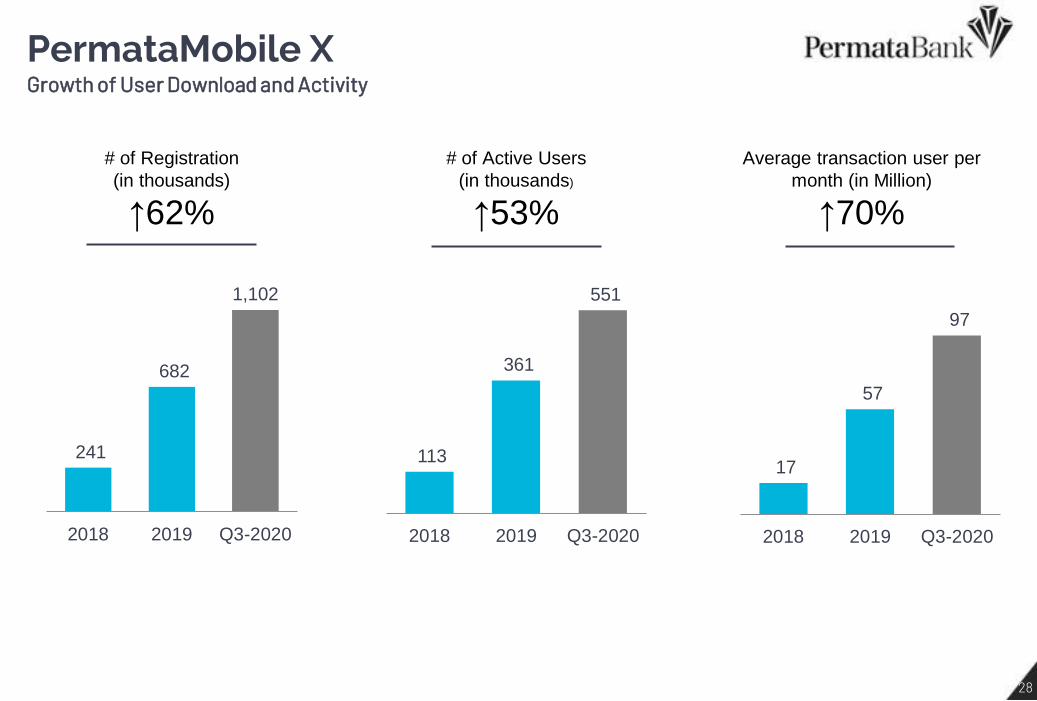

PermataMobile X Growth of User Download and Activity

Average transaction user per

month (in Million)

↑70%

# of Active Users

(in thousands)

↑53%

# of Registration

(in thousands)

↑62%

241

682

1,102

2018 2019 Q3-2020

113

361

551

2018 2019 Q3-2020

17

57

97

2018 2019 Q3-2020

28

Other Information

Board of Commissioner

Chartsiri Sophonpanich

President Commissioner

Chalit Tayjasanant

Commissioner

Chong Toh

Commissioner

Niramarn Laisathit

Commissioner

Haryanto Sahari

Independent Commissioner

Rahmat Waluyanto

Independent Commissioner

Goei Siauw Hong

Independent Commissioner

Yap Tjay Soen

Independent Commissioner

30

Board of Director

Ridha DM Wirakusumah

President Director

Dhien Tjahajani

Director

Lea Kusumawijaya

Director

Abdy Salimin

Director

Djumariah Tenteram

Director

Darwin Wibowo

Director

Herwin Bustaman

Director

Dayan sadikin

Director

31

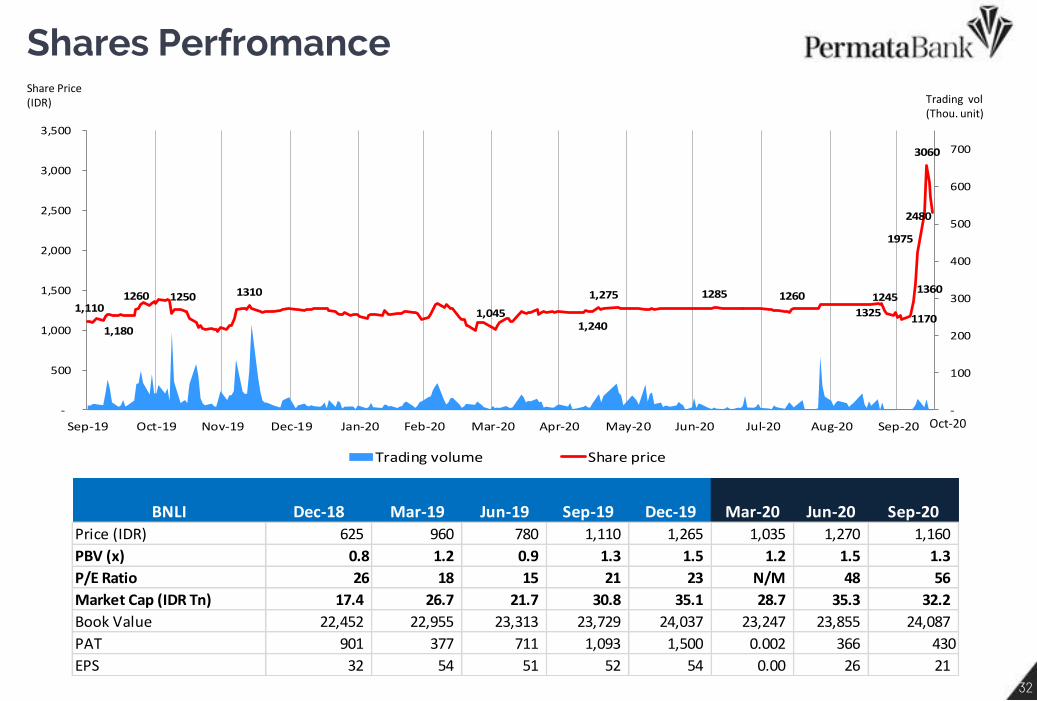

Shares Perfromance

1,110

1,180

1260 1250 1310

1,0451,240

1,275 1285 1260

1325

1245

1170

1360

1975

3060

2480

-

100

200

300

400

500

600

700

-

500

1,000

1,500

2,000

2,500

3,000

3,500

Sep-19 Oct-19 Nov-19 Dec-19 Jan-20 Feb-20 Mar-20 Apr-20 May-20 Jun-20 Jul-20 Aug-20 Sep-20

Trading volume Share price

Oct-20

Share Price (IDR) Trading vol

(Thou. unit)

BNLI Dec-18 Mar-19 Jun-19 Sep-19 Dec-19 Mar-20 Jun-20 Sep-20Price (IDR) 625 960 780 1,110 1,265 1,035 1,270 1,160

PBV (x) 0.8 1.2 0.9 1.3 1.5 1.2 1.5 1.3

P/E Ratio 26 18 15 21 23 N/M 48 56

Market Cap (IDR Tn) 17.4 26.7 21.7 30.8 35.1 28.7 35.3 32.2

Book Value 22,452 22,955 23,313 23,729 24,037 23,247 23,855 24,087

PAT 901 377 711 1,093 1,500 0.002 366 430

EPS 32 54 51 52 54 0.00 26 21

32

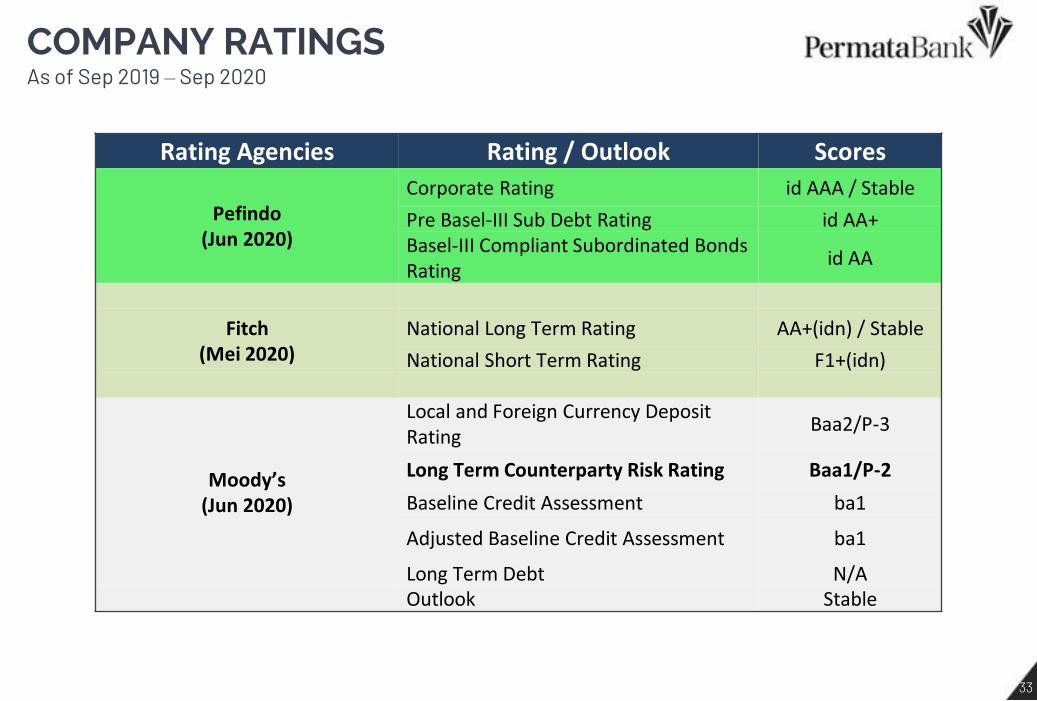

COMPANY RATINGS As of Sep 2019 – Sep 2020

Rating Agencies Rating / Outlook Scores

Pefindo (Jun 2020)

Corporate Rating id AAA / Stable

Pre Basel-III Sub Debt Rating id AA+ Basel-III Compliant Subordinated Bonds Rating

id AA

Fitch (Mei 2020)

National Long Term Rating AA+(idn) / Stable

National Short Term Rating F1+(idn)

Moody’s (Jun 2020)

Local and Foreign Currency Deposit Rating

Baa2/P-3

Long Term Counterparty Risk Rating Baa1/P-2

Baseline Credit Assessment ba1

Adjusted Baseline Credit Assessment ba1

Long Term Debt N/A Outlook Stable

33

Thank You! Investor Relations Unit World Trade Center II Jl. Jend. Sudirman Kav. 29-31 Jakarta 12920 - Indonesia Phone : (62-21) 523 - 7899 / 7999 Website : www.permatabank.com Email : [email protected]

Disclaimer: This report has been prepared by PT Bank Permata Tbk independently and is circulated for the purpose of general information only. It is not intended to the specific person who may

receive this report. The information in this report has been obtained from sources which we deem reliable. No warranty (expressed or implied) is made to the accuracy or completeness of the

information. All opinions and estimations included in this report constitute our judgment as of this date and are subject to change without prior notice.

We disclaim any responsibility or liability without prior notice of PT Bank Permata Tbk and/or their respective employees and/or agents whatsoever arising which may be brought against or suffered

by any person as a result of acting in reliance upon the whole or any part of the contents of this report and neither PT Bank Permata Tbk and/or its affiliated companies and/or their respective

employees and/or agents accepts liability for any errors, omissions, negligent or otherwise, in this report and any inaccuracy herein or omission here from which might otherwise arise.