nova nadia p, fixed assets xi akuntansi

DESCRIPTION

Pengertian, soal beserta jawaban tentang Aktiva TetapTRANSCRIPT

KELAS IX AKUNTANSI 1

KATA PENGANTARKATA PENGANTAR

Puji dan syukur senantiasa saya panjatkan ke hadirat Tuhan Yang Maha Esa,Puji dan syukur senantiasa saya panjatkan ke hadirat Tuhan Yang Maha Esa, karena berkat rahmat dan karunia-Nya saya dapat menyelesaikan makalah Kartu karena berkat rahmat dan karunia-Nya saya dapat menyelesaikan makalah Kartu Aktiva Tetap Kelas XI SMK ini.Aktiva Tetap Kelas XI SMK ini.

Makalah Kartu Aktiva Tetap ini membahas tentang pengertian dari aktiva Makalah Kartu Aktiva Tetap ini membahas tentang pengertian dari aktiva tetap itu dan metode-metode cara menghitung aktiva tetap tersebut. Makalah ini tetap itu dan metode-metode cara menghitung aktiva tetap tersebut. Makalah ini saya buat untuk seluruh siswa memahami pembelajaran aktiva tetap dengan saya buat untuk seluruh siswa memahami pembelajaran aktiva tetap dengan contoh-contoh yang saya berikan didalam metode-metode tersebut.contoh-contoh yang saya berikan didalam metode-metode tersebut.

Penulisan dan perbaikan makalah ini telah saya usahakan semaksimal Penulisan dan perbaikan makalah ini telah saya usahakan semaksimal mungkin, dengan segala kerendahan hati saya mengakui makalah ini jauh dari mungkin, dengan segala kerendahan hati saya mengakui makalah ini jauh dari kesempurnaan, oleh karena itu saya sangat mengharapkan kritik dan saran untuk kesempurnaan, oleh karena itu saya sangat mengharapkan kritik dan saran untuk kesempurnaan makalah ini.kesempurnaan makalah ini.

Semoga makalah ini dapat memberikan informasi bagi seluruh siswa dan Semoga makalah ini dapat memberikan informasi bagi seluruh siswa dan bermanfaat untuk pengembangan ilmu pengetahuan bagi kita semua.bermanfaat untuk pengembangan ilmu pengetahuan bagi kita semua.

Jakarta, November 2013Jakarta, November 2013

Nova Nadia PutriNova Nadia Putri

ii

DAFTAR ISIDAFTAR ISI

Kata Pengantar ………………………………………………………………………………………………… iKata Pengantar ………………………………………………………………………………………………… i

Daftar Isi ………………………………………………………………………………………………………….. iiDaftar Isi ………………………………………………………………………………………………………….. ii

a.Aktiva Tetap a.Aktiva Tetap 1. Pengertian Aktiva Tetap …………………………………………………………………………….. 1 1. Pengertian Aktiva Tetap …………………………………………………………………………….. 1 b.Metode perhitungan penyusutanb.Metode perhitungan penyusutan2. Metode Garis Lurus ( Straight Line ) ……………………………………………………………. 22. Metode Garis Lurus ( Straight Line ) ……………………………………………………………. 23. Metode Saldo Menurun Dengan Dua Garis Lurus (Declining balance method) 33. Metode Saldo Menurun Dengan Dua Garis Lurus (Declining balance method) 34. Metode Jumlah Angka Tahun (The Sum Of The Year Method) ……………………. 54. Metode Jumlah Angka Tahun (The Sum Of The Year Method) ……………………. 55. Metode Unit Produksi ( Units Of Production Method ) ……………………………….. 65. Metode Unit Produksi ( Units Of Production Method ) ……………………………….. 66. Metode Jam Kerja ( Office Hours Method ) …………………………………………………. 96. Metode Jam Kerja ( Office Hours Method ) …………………………………………………. 9 c.Penghentian Pemakaian Aktiva Tetapc.Penghentian Pemakaian Aktiva Tetap7. Penghentian pemakaian Aktiva Tetap secara Dibuang atau Disingkirkan …….. 127. Penghentian pemakaian Aktiva Tetap secara Dibuang atau Disingkirkan …….. 128. Penghentian pemakaian Aktiva Tetap secara Dijual …………………………………….. 138. Penghentian pemakaian Aktiva Tetap secara Dijual …………………………………….. 139. Penghentian pemakaian Aktiva Tetap secara Tukar Tambah sejenis …..……….. 149. Penghentian pemakaian Aktiva Tetap secara Tukar Tambah sejenis …..……….. 1410. Penghentian Aktiva Tetap secara Tukar Tambah Tidak Sejenis …………………. 1610. Penghentian Aktiva Tetap secara Tukar Tambah Tidak Sejenis …………………. 1611. Penutup……………………………………………………………………………………………………. 1811. Penutup……………………………………………………………………………………………………. 1812. Daftar Pustaka ………………………………………………………………………………………….. 1912. Daftar Pustaka ………………………………………………………………………………………….. 19

iiii

A.A. AKTIVA TETAPAKTIVA TETAP

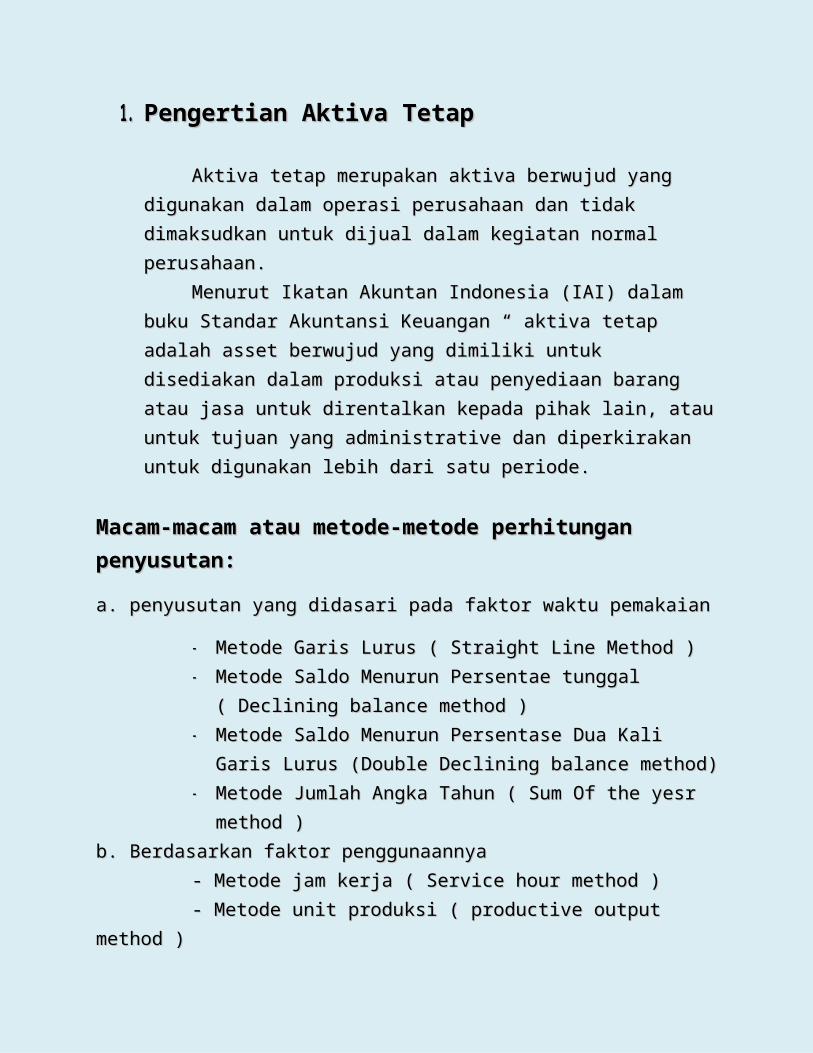

1.1. Pengertian Aktiva TetapPengertian Aktiva Tetap

Aktiva tetap merupakan aktiva berwujud yang digunakan dalam Aktiva tetap merupakan aktiva berwujud yang digunakan dalam operasi perusahaan dan tidak dimaksudkan untuk dijual dalam kegiatan operasi perusahaan dan tidak dimaksudkan untuk dijual dalam kegiatan normal perusahaan.normal perusahaan.

Menurut Ikatan Akuntan Indonesia (IAI) dalam buku Standar Menurut Ikatan Akuntan Indonesia (IAI) dalam buku Standar Akuntansi Keuangan “ aktiva tetap adalah asset berwujud yang dimiliki Akuntansi Keuangan “ aktiva tetap adalah asset berwujud yang dimiliki untuk disediakan dalam produksi atau penyediaan barang atau jasa untuk untuk disediakan dalam produksi atau penyediaan barang atau jasa untuk direntalkan kepada pihak lain, atau untuk tujuan yang administrative dan direntalkan kepada pihak lain, atau untuk tujuan yang administrative dan diperkirakan untuk digunakan lebih dari satu periode.diperkirakan untuk digunakan lebih dari satu periode.

Macam-macam atau metode-metode perhitungan penyusutan:Macam-macam atau metode-metode perhitungan penyusutan:

a. penyusutan yang didasari pada faktor waktu pemakaiana. penyusutan yang didasari pada faktor waktu pemakaian

-- Metode Garis Lurus ( Straight Line Method )Metode Garis Lurus ( Straight Line Method )-- Metode Saldo Menurun Persentae tunggal ( Declining balance Metode Saldo Menurun Persentae tunggal ( Declining balance

method )method )-- Metode Saldo Menurun Persentase Dua Kali Garis Lurus (Double Metode Saldo Menurun Persentase Dua Kali Garis Lurus (Double

Declining balance method)Declining balance method)-- Metode Jumlah Angka Tahun ( Sum Of the yesr method ) Metode Jumlah Angka Tahun ( Sum Of the yesr method )

b. Berdasarkan faktor penggunaannyab. Berdasarkan faktor penggunaannya- Metode jam kerja ( Service hour method )- Metode jam kerja ( Service hour method )- Metode unit produksi ( productive output method )- Metode unit produksi ( productive output method )

Penghentian Aktiva Tetap ( Retirement Of Plant Asset )Penghentian Aktiva Tetap ( Retirement Of Plant Asset )a.a. Dibuang atau disingkirkanDibuang atau disingkirkanb.b. DijualDijualc.c. Tukar tambahTukar tambah

Aktiva TetapAktiva Tetap 11

2.2. Metode Garis Lurus ( Straight Line )Metode Garis Lurus ( Straight Line )

Metode ini bahwa harta tetap dimanfaatkan dengan cara yang sama dari tahun-Metode ini bahwa harta tetap dimanfaatkan dengan cara yang sama dari tahun-ketahun, sehingga besarnya penyusutan harta tetap tiap periode akuntansi adalahketahun, sehingga besarnya penyusutan harta tetap tiap periode akuntansi adalah sama.sama.Rumus :Rumus :

P = P = HP−NSUE

Keterangan :Keterangan :PP = Penyusutan per periode= Penyusutan per periodeHPHP = Harga perolehan dari harta tetap= Harga perolehan dari harta tetapNSNS = Nilai residu= Nilai residuUEUE = Umur manfaat= Umur manfaatRumus ini bisa dimodifikasi :Rumus ini bisa dimodifikasi :

P= 1UE

×100%×(HP−NS)

Contoh :Contoh :Early 2001 PT. Putri Angkasa buy machines for Rp. 18.000.000, transport Early 2001 PT. Putri Angkasa buy machines for Rp. 18.000.000, transport cost Rp. 2.000.000, trial costs Rp. 1.100.000, installation costs Rp. 1.000.000cost Rp. 2.000.000, trial costs Rp. 1.100.000, installation costs Rp. 1.000.000 and is expected to be used for 5 years with a value of remaining Rp.100.000and is expected to be used for 5 years with a value of remaining Rp.100.000Requested:Requested:a. compute the cost of depreciation by the straight line methoda. compute the cost of depreciation by the straight line methodb. make a chart of depreciationb. make a chart of depreciationAnswer:Answer:

a.a. Depreciation expenseDepreciation expensePurchase pricePurchase price Rp. 7.000.000Rp. 7.000.000transport costtransport cost Rp. 2.000.000Rp. 2.000.000trial costtrial cost Rp. 1.100.000Rp. 1.100.000installation costinstallation cost Rp. 1.000.000 +Rp. 1.000.000 +

Rp. 3.100.000 +Rp. 3.100.000 +Acquisition priceAcquisition price Rp. 10.100.000Rp. 10.100.000

Depreciation expense/yearDepreciation expense/year : : Rp .10 .100 .000−Rp .100 .000

5=Rp .2 .000 .000

Aktiva TetapAktiva Tetap 22b.b. Depreciation Table :Depreciation Table :

Date Depreciation Expense Accumulated Depreciation Book Value31/12/01 Rp 2,000,000 Rp 2,000,000 Rp 8,000,00031/12/02 Rp 2,000,000 Rp 4,000,000 Rp 6,000,00031/12/03 Rp 2,000,000 Rp 6,000,000 Rp 4,000,00031/12/04 Rp 2,000,000 Rp 8,000,000 Rp 2,000,00031/12/05 Rp 2,000,000 Rp 10,000,000 -

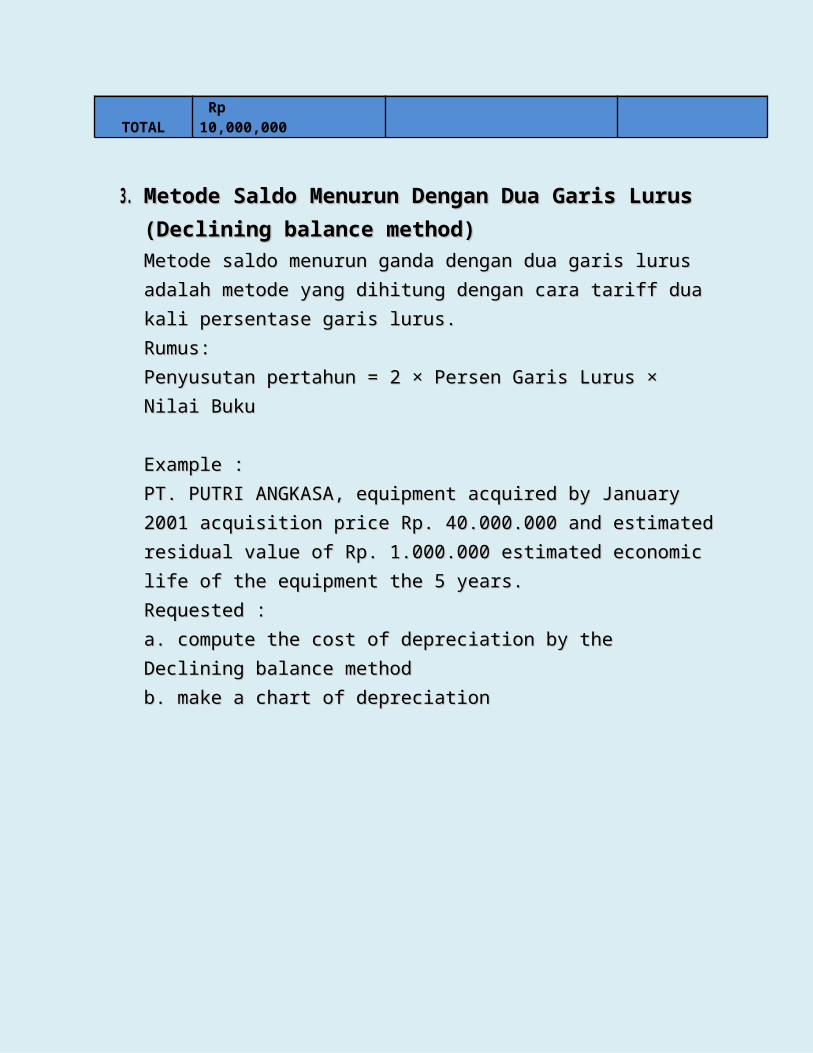

TOTAL Rp 10,000,000

3.3. Metode Saldo Menurun Dengan Dua Garis Lurus (Declining Metode Saldo Menurun Dengan Dua Garis Lurus (Declining balance method)balance method)Metode saldo menurun ganda dengan dua garis lurus adalah metode yang Metode saldo menurun ganda dengan dua garis lurus adalah metode yang dihitung dengan cara tariff dua kali persentase garis lurus.dihitung dengan cara tariff dua kali persentase garis lurus.Rumus:Rumus:Penyusutan pertahun = 2 × Persen Garis Lurus × Nilai BukuPenyusutan pertahun = 2 × Persen Garis Lurus × Nilai Buku

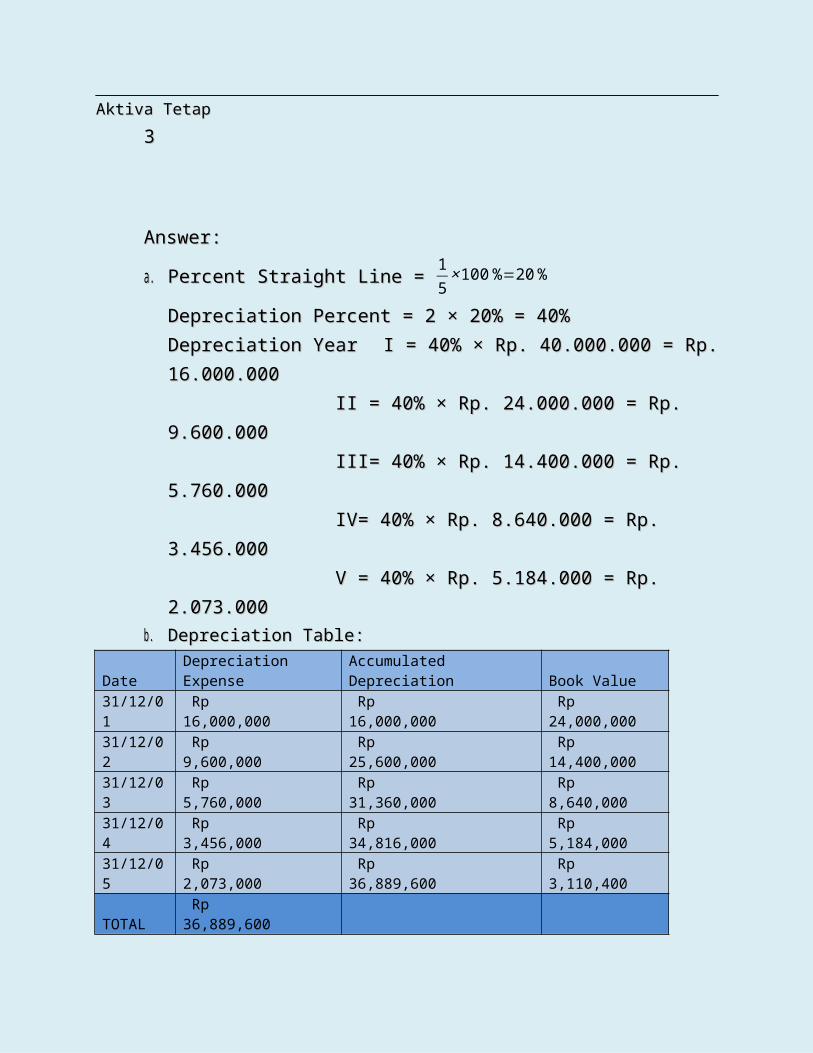

Example :Example :PT. PUTRI ANGKASA, equipment acquired by January 2001 acquisition price PT. PUTRI ANGKASA, equipment acquired by January 2001 acquisition price Rp. 40.000.000 and estimated residual value of Rp. 1.000.000 estimated Rp. 40.000.000 and estimated residual value of Rp. 1.000.000 estimated economic life of the equipment the 5 years.economic life of the equipment the 5 years.Requested :Requested :a. compute the cost of depreciation by the a. compute the cost of depreciation by the Declining balanceDeclining balance method methodb. make a chart of depreciationb. make a chart of depreciation

Aktiva TetapAktiva Tetap 33

Answer:Answer:

a.a. Percent Straight Line = Percent Straight Line = 15×100%=20%

Depreciation Percent = 2 × 20% = 40%Depreciation Percent = 2 × 20% = 40%Depreciation Year Depreciation Year I = 40% × Rp. 40.000.000 = Rp. 16.000.000I = 40% × Rp. 40.000.000 = Rp. 16.000.000

II = 40% × Rp. 24.000.000 = Rp. 9.600.000II = 40% × Rp. 24.000.000 = Rp. 9.600.000III= 40% × Rp. 14.400.000 = Rp. 5.760.000III= 40% × Rp. 14.400.000 = Rp. 5.760.000IV= 40% × Rp. 8.640.000 = Rp. 3.456.000IV= 40% × Rp. 8.640.000 = Rp. 3.456.000V = 40% × Rp. 5.184.000 = Rp. 2.073.000V = 40% × Rp. 5.184.000 = Rp. 2.073.000

b.b. Depreciation Table:Depreciation Table:Date Depreciation Expense Accumulated Depreciation Book Value31/12/01 Rp 16,000,000 Rp 16,000,000 Rp 24,000,00031/12/02 Rp 9,600,000 Rp 25,600,000 Rp 14,400,00031/12/03 Rp 5,760,000 Rp 31,360,000 Rp 8,640,00031/12/04 Rp 3,456,000 Rp 34,816,000 Rp 5,184,00031/12/05 Rp 2,073,000 Rp 36,889,600 Rp 3,110,400TOTAL Rp 36,889,600

Aktiva TetapAktiva Tetap 44

4.4. Metode Jumlah Angka Tahun (The Sum Of The Year Metode Jumlah Angka Tahun (The Sum Of The Year Method)Method)Metode ini, metode yang dapat dicari penyusutannya dengan cara Metode ini, metode yang dapat dicari penyusutannya dengan cara menjumlahkan semua angka dari umur ekonomis dari harta tetap yang menjumlahkan semua angka dari umur ekonomis dari harta tetap yang bersangkutan.bersangkutan.

Rumus = Rumus = sisaumur aktiva

jumlah angka tahunumuraktiva tetap× jumlah yangharus disusutkan

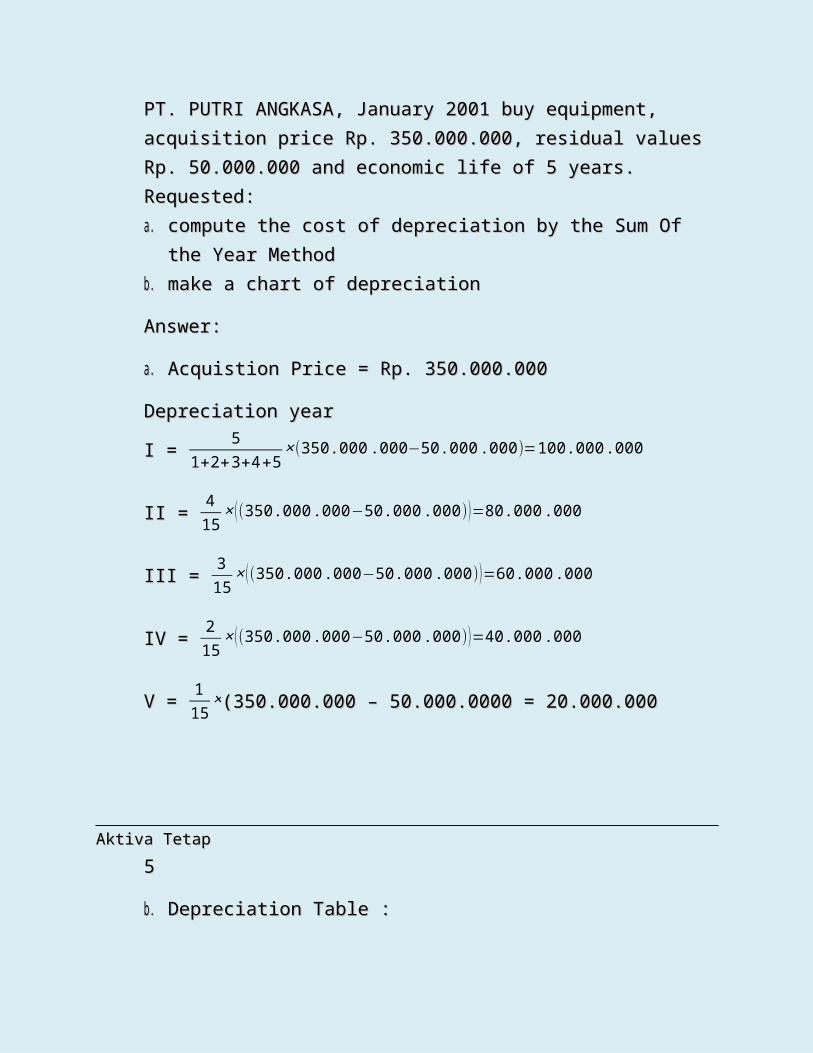

Contoh :Contoh :PT. PUTRI ANGKASA, January 2001 buy equipment, acquisition price Rp. PT. PUTRI ANGKASA, January 2001 buy equipment, acquisition price Rp. 350.000.000, residual values Rp. 50.000.000 and economic life of 5 years.350.000.000, residual values Rp. 50.000.000 and economic life of 5 years.Requested:Requested:a.a. compute the cost of depreciation by the Sum Of the Year Methodcompute the cost of depreciation by the Sum Of the Year Methodb.b. make a chart of depreciationmake a chart of depreciation

Answer:Answer:

a.a. Acquistion Price = Rp. 350.000.000Acquistion Price = Rp. 350.000.000

Depreciation year Depreciation year

I = I = 5

1+2+3+4+5×(350.000 .000−50.000.000)=100.000.000

II = II = 415× ((350.000 .000−50.000 .000))=80.000.000

III = III = 315× ((350.000 .000−50.000 .000))=60.000.000

IV = IV = 215× ((350.000 .000−50.000 .000))=40.000 .000

V = V = 115×(350.000.000 – 50.000.0000 = 20.000.000(350.000.000 – 50.000.0000 = 20.000.000

Aktiva TetapAktiva Tetap 55

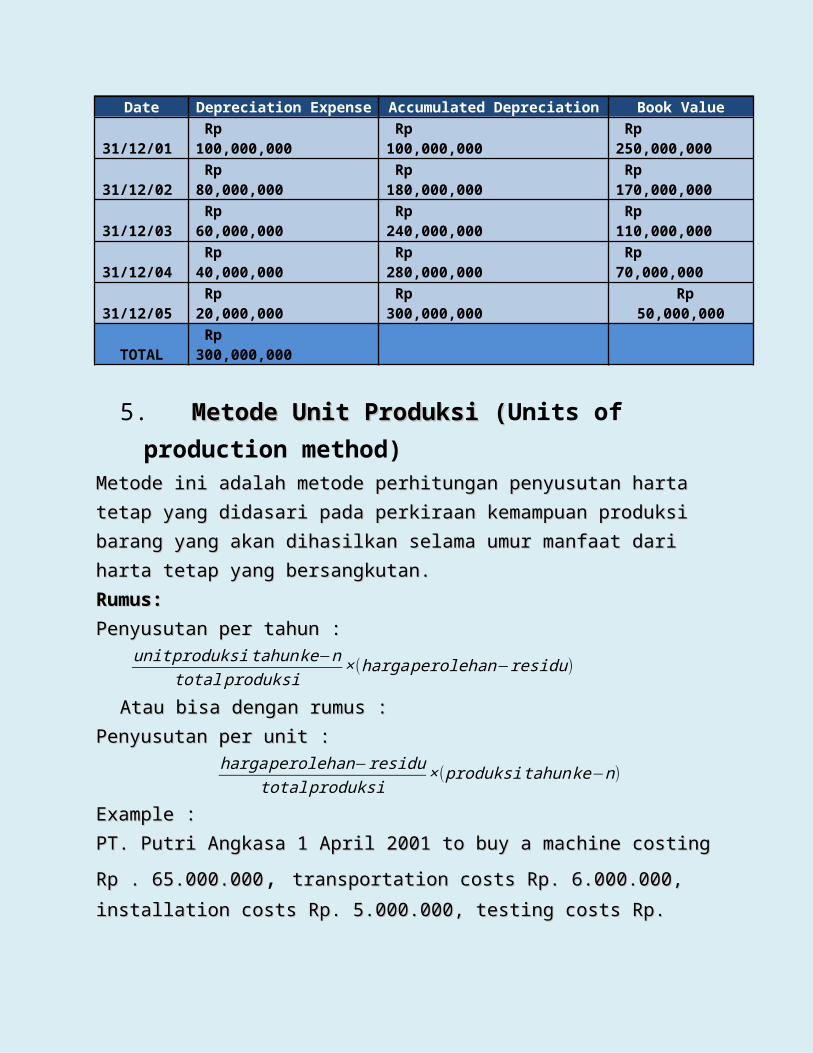

b.b. Depreciation Table :Depreciation Table :

Date Depreciation Expense Accumulated Depreciation Book Value31/12/01 Rp 100,000,000 Rp 100,000,000 Rp 250,000,00031/12/02 Rp 80,000,000 Rp 180,000,000 Rp 170,000,00031/12/03 Rp 60,000,000 Rp 240,000,000 Rp 110,000,00031/12/04 Rp 40,000,000 Rp 280,000,000 Rp 70,000,00031/12/05 Rp 20,000,000 Rp 300,000,000 Rp 50,000,000

TOTAL Rp 300,000,000

5. Metode Unit Produksi (Metode Unit Produksi (Units of production method)Metode ini adalah metode perhitungan penyusutan harta tetap yang didasari Metode ini adalah metode perhitungan penyusutan harta tetap yang didasari pada perkiraan kemampuan produksi barang yang akan dihasilkan selama umur pada perkiraan kemampuan produksi barang yang akan dihasilkan selama umur manfaat dari harta tetap yang bersangkutan. manfaat dari harta tetap yang bersangkutan. Rumus:Rumus:Penyusutan per tahun :Penyusutan per tahun :

unit produksi tahun ke−n

total produksi×(harga perolehan−residu)

Atau bisa dengan rumus :Atau bisa dengan rumus :Penyusutan per unit :Penyusutan per unit :

harga perolehan−residutotal produksi

×(produksi tahunke−n)

Example :Example :

PT. Putri Angkasa 1 April 2001 to buy a machine costing Rp . 65.000.000PT. Putri Angkasa 1 April 2001 to buy a machine costing Rp . 65.000.000, transportation costs Rp. 6.000.000, installation costs Rp. 5.000.000, testing costs transportation costs Rp. 6.000.000, installation costs Rp. 5.000.000, testing costs Rp. 4.000.000, economic life of 5 years, residual values Rp. 4.000.000, economic life of 5 years, residual values Rp. 8.000.000Rp. 8.000.000

Year Production Unit Office Hours2001 Rp 60,000 Rp 2,0002002 Rp 105,000 Rp 6,0002003 Rp 120,000 Rp 6,2002004 Rp 115,000 Rp 6,3002005 Rp 100,000 Rp 4,000

TOTAL Rp 500,000 Rp 24,500

Aktiva TetapAktiva Tetap 66

Requested :Requested :

a.a. compute the cost of depreciation by Units Of Production Methodcompute the cost of depreciation by Units Of Production Methodb.b. make a chart of depreciationmake a chart of depreciation

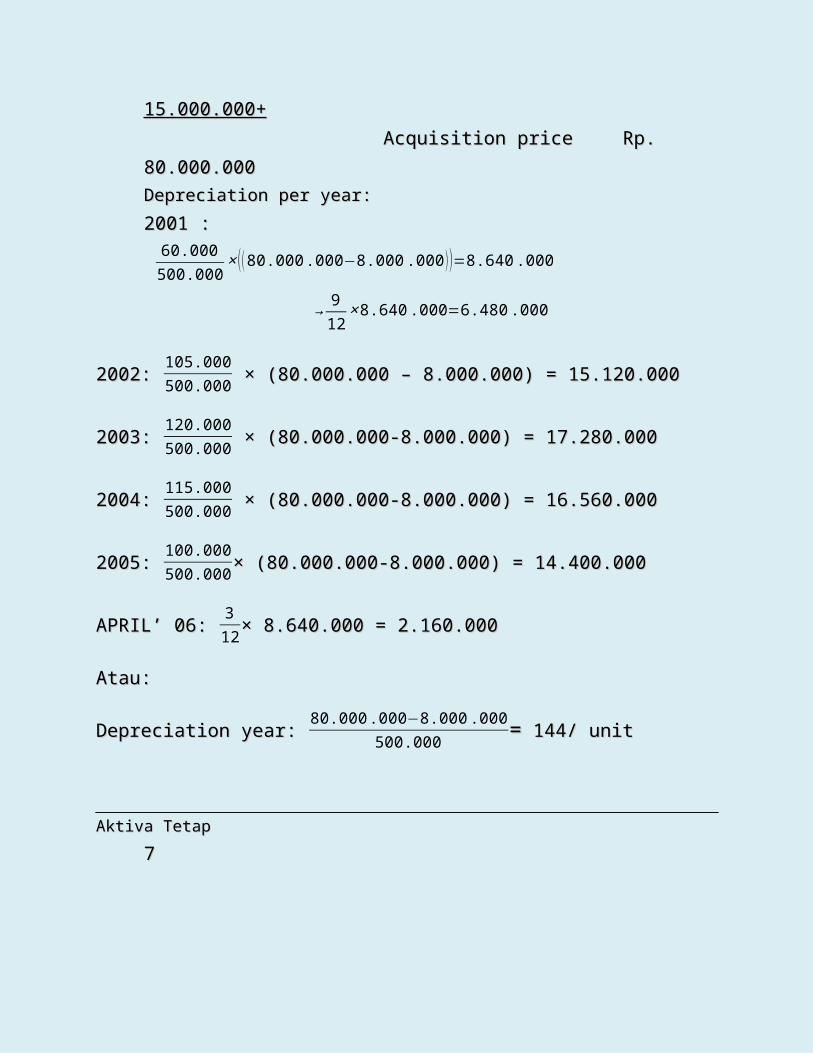

Answer:Answer:a.a. Acquisition price=Acquisition price=

purchase pricepurchase price Rp. 65.000.000Rp. 65.000.000transportation costtransportation cost Rp. 6.000.000Rp. 6.000.000installation costinstallation cost Rp. 5.000.000Rp. 5.000.000testing costtesting cost Rp. 4.000.000 +Rp. 4.000.000 +

Rp. 15.000.000+Rp. 15.000.000+Acquisition priceAcquisition price Rp. 80.000.000Rp. 80.000.000

Depreciation per year:Depreciation per year:

2001 :2001 :

60.000500.000

× ( (80.000 .000−8.000 .000 ) )=8.640 .000

→912×8.640 .000=6.480 .000

2002: 2002: 105.000500.000 × (80.000.000 – 8.000.000) = 15.120.000 × (80.000.000 – 8.000.000) = 15.120.000

2003: 2003: 120.000500.000 × (80.000.000-8.000.000) = 17.280.000 × (80.000.000-8.000.000) = 17.280.000

2004: 2004: 115.000500.000 × (80.000.000-8.000.000) = 16.560.000 × (80.000.000-8.000.000) = 16.560.000

2005: 2005: 100.000500.000× (80.000.000-8.000.000) = 14.400.000× (80.000.000-8.000.000) = 14.400.000

APRIL’ 06: APRIL’ 06: 312× 8.640.000 = 2.160.000× 8.640.000 = 2.160.000

Atau:Atau:

Depreciation year: Depreciation year: 80.000 .000−8.000 .000

500.000 == 144/ unit 144/ unit

Aktiva TetapAktiva Tetap 77

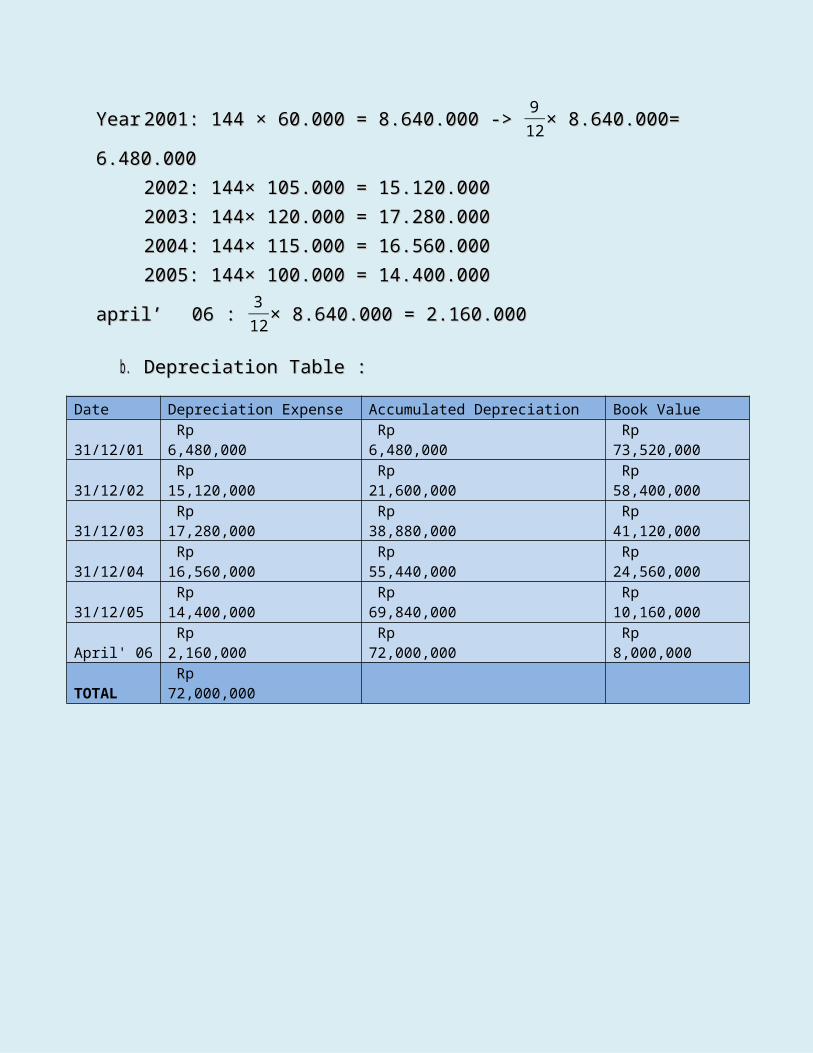

YearYear 2001: 144 × 60.000 = 8.640.000 -> 2001: 144 × 60.000 = 8.640.000 -> 912× 8.640.000= 6.480.000× 8.640.000= 6.480.000

2002: 144× 105.000 = 15.120.0002002: 144× 105.000 = 15.120.0002003: 144× 120.000 = 17.280.0002003: 144× 120.000 = 17.280.0002004: 144× 115.000 = 16.560.0002004: 144× 115.000 = 16.560.0002005: 144× 100.000 = 14.400.0002005: 144× 100.000 = 14.400.000

april’april’ 06 : 06 : 312× 8.640.000 = 2.160.000× 8.640.000 = 2.160.000

b.b. Depreciation Table :Depreciation Table :

Date Depreciation Expense Accumulated Depreciation Book Value

31/12/01 Rp 6,480,000 Rp 6,480,000 Rp 73,520,000

31/12/02 Rp 15,120,000 Rp 21,600,000 Rp 58,400,000

31/12/03 Rp 17,280,000 Rp 38,880,000 Rp 41,120,000

31/12/04 Rp 16,560,000 Rp 55,440,000 Rp 24,560,000

31/12/05 Rp 14,400,000 Rp 69,840,000 Rp 10,160,000

April' 06 Rp 2,160,000 Rp 72,000,000 Rp 8,000,000

TOTAL Rp 72,000,000

Aktiva TetapAktiva Tetap 88

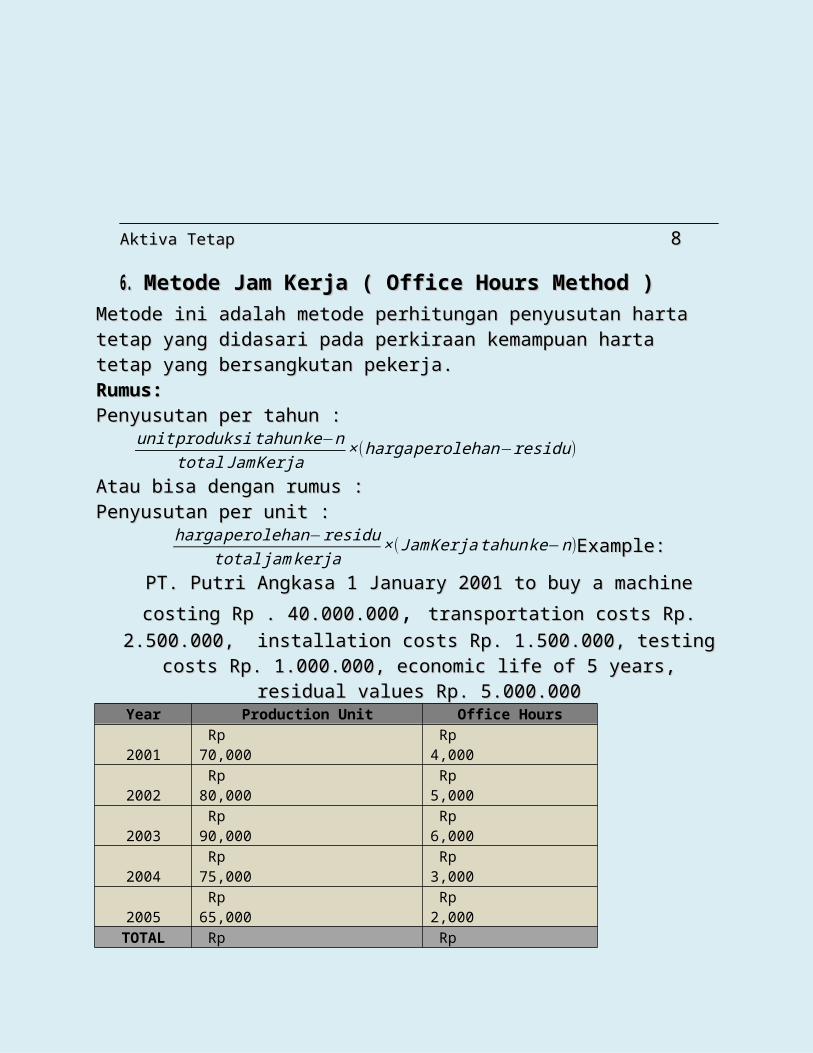

6.6. Metode Jam Kerja ( Office Hours Method )Metode Jam Kerja ( Office Hours Method )Metode ini adalah metode perhitungan penyusutan harta tetap yang didasari Metode ini adalah metode perhitungan penyusutan harta tetap yang didasari pada perkiraan kemampuan harta tetap yang bersangkutan pekerja.pada perkiraan kemampuan harta tetap yang bersangkutan pekerja.Rumus:Rumus:Penyusutan per tahun :Penyusutan per tahun :

unit produksi tahun ke−ntotal Jam Kerja×(harga perolehan−residu)

Atau bisa dengan rumus :Atau bisa dengan rumus :Penyusutan per unit :Penyusutan per unit :

harga perolehan−residutotal jam kerja

×(Jam Kerjatahunke−n)Example:Example:

PT. Putri Angkasa 1 January 2001 to buy a machine costing Rp . 40.000.000PT. Putri Angkasa 1 January 2001 to buy a machine costing Rp . 40.000.000, transportation costs Rp. 2.500.000, installation costs Rp. 1.500.000, testingtransportation costs Rp. 2.500.000, installation costs Rp. 1.500.000, testing costs Rp. 1.000.000, economic life of 5 years, residual values costs Rp. 1.000.000, economic life of 5 years, residual values Rp. 5.000.000Rp. 5.000.000

Year Production Unit Office Hours2001 Rp 70,000 Rp 4,0002002 Rp 80,000 Rp 5,0002003 Rp 90,000 Rp 6,0002004 Rp 75,000 Rp 3,0002005 Rp 65,000 Rp 2,000

TOTAL Rp 380,000 Rp 20,000

Requested :Requested :a.a. compute the cost of depreciation by Units Of Production Methodcompute the cost of depreciation by Units Of Production Methodb.b. make a chart of depreciationmake a chart of depreciation

Answer:Answer:a.a. Acquisition price=Acquisition price=

purchase pricepurchase price Rp. 40.000.000Rp. 40.000.000transportation costtransportation cost Rp. 2.500.000Rp. 2.500.000installation costinstallation cost Rp. 1.500.000Rp. 1.500.000testing costtesting cost Rp. 1.000.000 +Rp. 1.000.000 +

Rp. 5.000.000+Rp. 5.000.000+Acquisition priceAcquisition price Rp. 45.000.000Rp. 45.000.000

Aktiva TetapAktiva Tetap 99

Depreciation per year:Depreciation per year:

2001 :2001 : 4.00020.000× (45.000.000-5.000.000) = 8.000.000× (45.000.000-5.000.000) = 8.000.000

2002: 2002: 5.00020.000 × (45.000.000 – 5.000.000) = 10.000.000 × (45.000.000 – 5.000.000) = 10.000.000

2003: 2003: 6.00020.000 × (45.000.000-5.000.000) = 12.000.000 × (45.000.000-5.000.000) = 12.000.000

2004: 2004: 3.00020.000 × (45.000.000-5.000.000) = 6.000.000 × (45.000.000-5.000.000) = 6.000.000

2005: 2005: 2.00020.000× (45.000.000-5.000.000) = 4.000.000× (45.000.000-5.000.000) = 4.000.000

Atau dengan:Atau dengan:

Depreciation year: Depreciation year: 45.000 .000−5.000 .000

20.000 == 2.000/ unit 2.000/ unit

YearYear 2001: 2000 × 4.000 = 8.000.0002001: 2000 × 4.000 = 8.000.0002002: 2000× 5.000 = 10.000.0002002: 2000× 5.000 = 10.000.0002003: 2000× 6.000 = 12.000.0002003: 2000× 6.000 = 12.000.0002004: 2000× 3.000 = 6.000.0002004: 2000× 3.000 = 6.000.0002005: 2000× 2.000 = 4.000.0002005: 2000× 2.000 = 4.000.000

b.b. Depreciation Table:Depreciation Table:

Date Depreciation Expense Accumulated Depreciation Book Value

31/12/01 Rp 8,000,000 Rp 8,000,000 Rp 37,000,000

31/12/02 Rp 10,000,000 Rp 18,000,000 Rp 27,000,000

31/12/03 Rp 12,000,000 Rp 30,000,000 Rp 15,000,000

31/12/04 Rp 6,000,000 Rp 36,000,000 Rp 9,000,000

31/12/05 Rp 4,000,000 Rp 40,000,000 Rp 5,000,000

TOTAL Rp 40,000,000

Aktiva TetapAktiva Tetap 1010

C.Penghentian Pemakaian Aktiva Tetap(C.Penghentian Pemakaian Aktiva Tetap( TERMINATION OFTERMINATION OF USE OF FIXED ASSETS)USE OF FIXED ASSETS)

Penghentian atau penyingkiran aktiva tetap adalah usaha untuk Penghentian atau penyingkiran aktiva tetap adalah usaha untuk menghapuskan atau menghilangkan aktiva tetap dari catatan perusahaan. menghapuskan atau menghilangkan aktiva tetap dari catatan perusahaan. Penyingkiran aktiva tetap dapat disebabkan karena keusangan, kebakran, dijual Penyingkiran aktiva tetap dapat disebabkan karena keusangan, kebakran, dijual atau dituka dengan aktiva lain yang sejenis atau dengan aktiva tidak sejenis.atau dituka dengan aktiva lain yang sejenis atau dengan aktiva tidak sejenis.Penghentian pemakaian aktiva tetap terbagi menjadi:Penghentian pemakaian aktiva tetap terbagi menjadi:

a.a. Dibuang atau disingkirkan (discarded or removed)Dibuang atau disingkirkan (discarded or removed)Jurnal :Jurnal :AA1 1 == Umur ekonomis yang habisUmur ekonomis yang habis AA22 = = umur ekonomis tidak habisumur ekonomis tidak habis

Akm. Penyusutan mesinAkm. Penyusutan mesin Akm. PenyusutanAkm. PenyusutanRugi pembuangan mesinRugi pembuangan mesin

b.b. Dijual (sales)Dijual (sales)Jurnal:Jurnal:BB11=Apabila Rugi=Apabila Rugi BB2 2 = Apabila Laba= Apabila LabaKasKas KasKasAkm. PenyusutanAkm. Penyusutan Akm. penyusutanAkm. penyusutanRugiRugi MesinMesin

MesinMesin LabaLaba

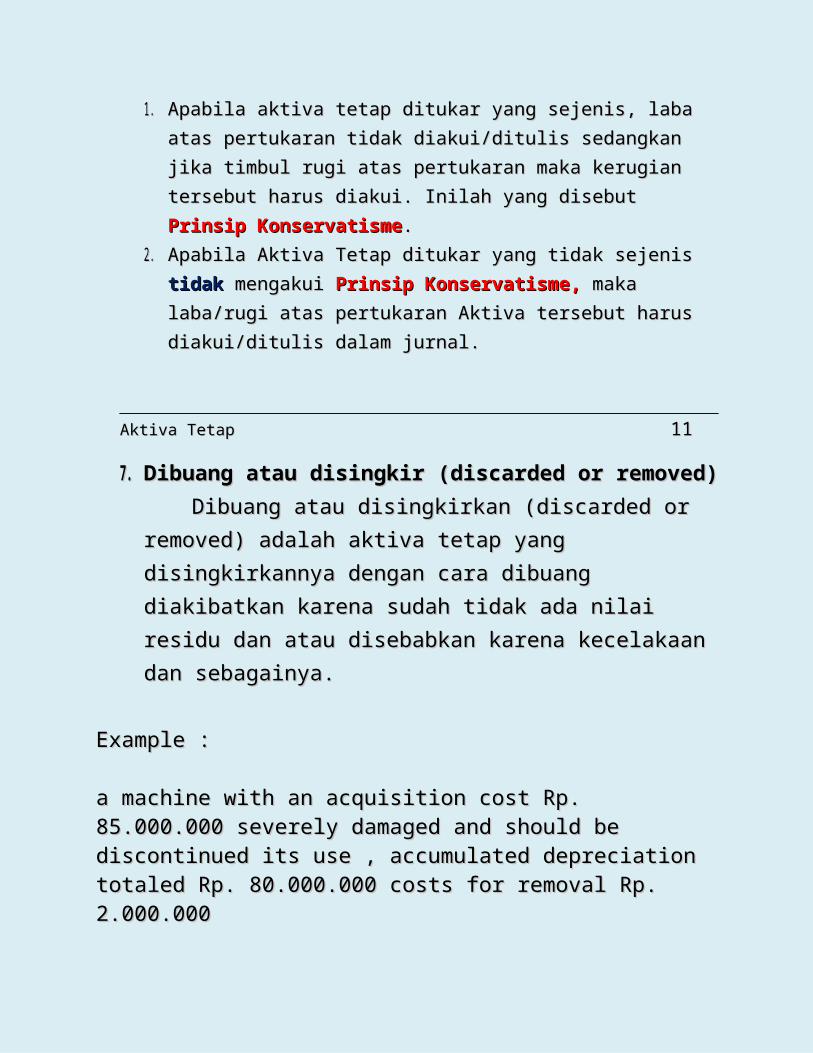

c.c. Tukar TambahTukar TambahDalam pertukaran Aktiva Tetap, mungkin akan menimbulkan laba/rugi:Dalam pertukaran Aktiva Tetap, mungkin akan menimbulkan laba/rugi:1.1. Apabila aktiva tetap ditukar yang sejenis, laba atas pertukaran tidak Apabila aktiva tetap ditukar yang sejenis, laba atas pertukaran tidak

diakui/ditulis sedangkan jika timbul rugi atas pertukaran maka kerugian diakui/ditulis sedangkan jika timbul rugi atas pertukaran maka kerugian tersebut harus diakui. Inilah yang disebut tersebut harus diakui. Inilah yang disebut Prinsip KonservatismePrinsip Konservatisme..

2.2. Apabila Aktiva Tetap ditukar yang tidak sejenis Apabila Aktiva Tetap ditukar yang tidak sejenis tidaktidak mengakui mengakui Prinsip Prinsip Konservatisme, Konservatisme, maka laba/rugi atas pertukaran Aktiva tersebut harus maka laba/rugi atas pertukaran Aktiva tersebut harus diakui/ditulis dalam jurnal.diakui/ditulis dalam jurnal.

Aktiva TetapAktiva Tetap 1111

7.7. Dibuang atau disingkir (discarded or removed)Dibuang atau disingkir (discarded or removed)Dibuang atau disingkirkan (discarded or removed) adalah Dibuang atau disingkirkan (discarded or removed) adalah

aktiva tetap yang disingkirkannya dengan cara dibuang aktiva tetap yang disingkirkannya dengan cara dibuang diakibatkan karena sudah tidak ada nilai residu dan atau diakibatkan karena sudah tidak ada nilai residu dan atau disebabkan karena kecelakaan dan sebagainya.disebabkan karena kecelakaan dan sebagainya.

Example :Example :

a machine with an acquisition cost Rp. 85.000.000 severely damaged a machine with an acquisition cost Rp. 85.000.000 severely damaged and should be discontinued its use , accumulated depreciation totaled and should be discontinued its use , accumulated depreciation totaled Rp. 80.000.000 costs for removal Rp. 2.000.000Rp. 80.000.000 costs for removal Rp. 2.000.000

Requested:Requested:make journal discontinuation of fixed assets!make journal discontinuation of fixed assets!

Answer:Answer:acquisition priceacquisition price Rp. 85.000.000Rp. 85.000.000accumulated depreciationaccumulated depreciation Rp. 80.000.000 –Rp. 80.000.000 –

lossloss Rp. 5.000.000Rp. 5.000.000transportation coststransportation costs Rp. 2.000.000 +Rp. 2.000.000 +total costtotal cost Rp. 7.000.000Rp. 7.000.000

Journal :Journal :accumulated depreciationaccumulated depreciation Rp. 80.000.000Rp. 80.000.000lossloss Rp. 7.000.000Rp. 7.000.000 machinemachine Rp. 87.000.000Rp. 87.000.000

Aktiva TetapAktiva Tetap 1212

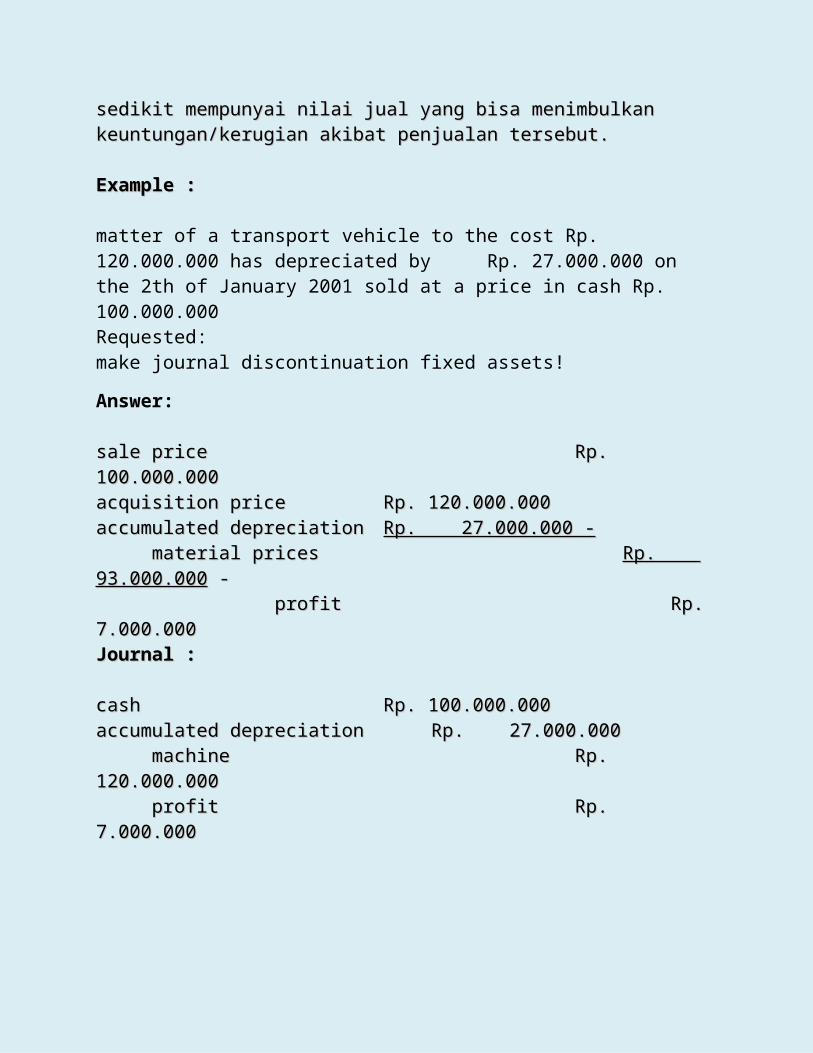

8.8. Dijual ( sales )Dijual ( sales )

Dijual (sales) adalah dikarenakan ingin mengganti barang yang baru, dan barang Dijual (sales) adalah dikarenakan ingin mengganti barang yang baru, dan barang lama dijual. Atau karena barang tersebut sudah tidak ingin dipakai yang masih lama dijual. Atau karena barang tersebut sudah tidak ingin dipakai yang masih sedikit mempunyai nilai jual yang bisa menimbulkan keuntungan/kerugian akibat sedikit mempunyai nilai jual yang bisa menimbulkan keuntungan/kerugian akibat penjualan tersebut.penjualan tersebut.

Example :Example :

matter of a transport vehicle to the cost Rp. 120.000.000 has depreciated by Rp. 27.000.000 on the 2th of January 2001 sold at a price in cash Rp. 100.000.000Requested:make journal discontinuation fixed assets!

Answer:

sale pricesale price Rp. 100.000.000Rp. 100.000.000acquisition priceacquisition price Rp. 120.000.000Rp. 120.000.000accumulated depreciationaccumulated depreciation Rp. 27.000.000 -Rp. 27.000.000 - material pricesmaterial prices Rp. 93.000.000Rp. 93.000.000 - - profitprofit Rp. 7.000.000Rp. 7.000.000Journal :Journal :

cashcash Rp. 100.000.000Rp. 100.000.000accumulated depreciationaccumulated depreciation Rp. 27.000.000Rp. 27.000.000 machinemachine Rp. 120.000.000Rp. 120.000.000 profitprofit Rp. 7.000.000Rp. 7.000.000

Aktiva TetapAktiva Tetap 1313

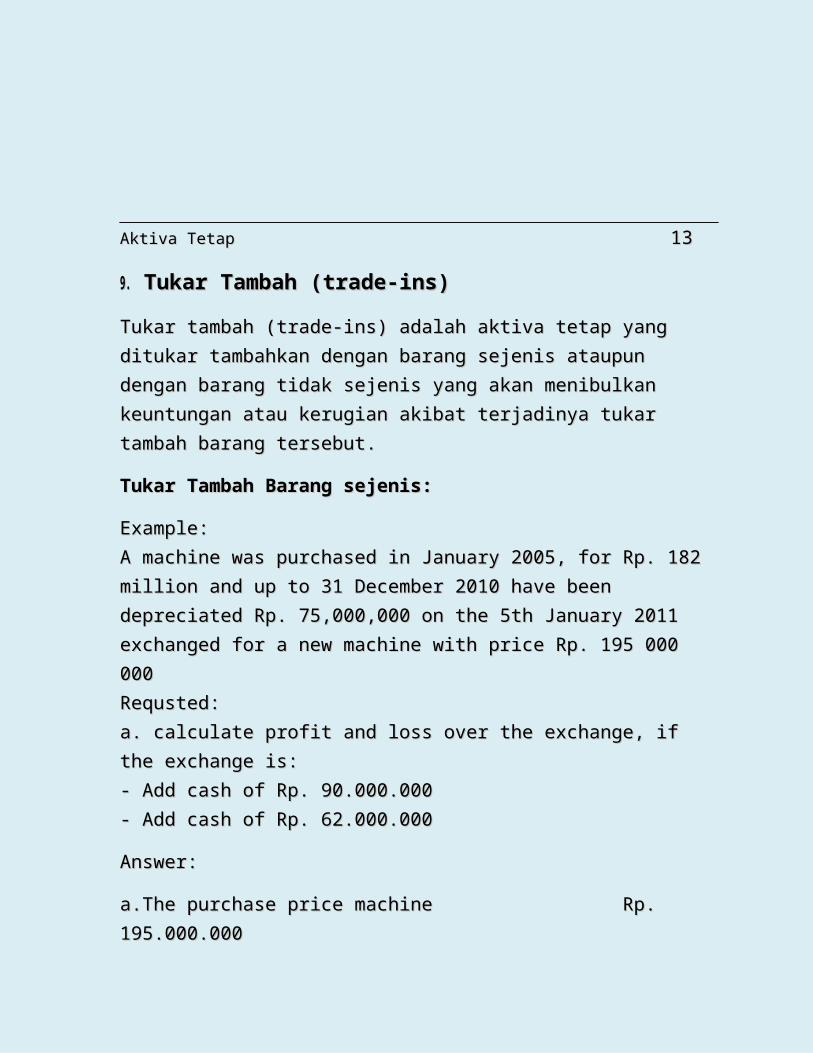

9.9. Tukar Tambah (trade-ins)Tukar Tambah (trade-ins)

Tukar tambah (trade-ins) adalah aktiva tetap yang ditukar tambahkan dengan Tukar tambah (trade-ins) adalah aktiva tetap yang ditukar tambahkan dengan barang sejenis ataupun dengan barang tidak sejenis yang akan menibulkan barang sejenis ataupun dengan barang tidak sejenis yang akan menibulkan keuntungan atau kerugian akibat terjadinya tukar tambah barang tersebut.keuntungan atau kerugian akibat terjadinya tukar tambah barang tersebut.

Tukar Tambah Barang sejenis:Tukar Tambah Barang sejenis:

Example:Example:A machine was purchased in January 2005, for Rp. 182 million and up to 31 A machine was purchased in January 2005, for Rp. 182 million and up to 31 December 2010 have been depreciated Rp. 75,000,000 on the 5th January December 2010 have been depreciated Rp. 75,000,000 on the 5th January 2011 exchanged for a new machine with price Rp. 195 000 0002011 exchanged for a new machine with price Rp. 195 000 000Requsted:Requsted:a. calculate profit and loss over the exchange, if the exchange is:a. calculate profit and loss over the exchange, if the exchange is:- Add cash of Rp. 90.000.000- Add cash of Rp. 90.000.000- Add cash of Rp. 62.000.000- Add cash of Rp. 62.000.000

Answer:Answer:

a.The purchase price machinea.The purchase price machine Rp. 195.000.000Rp. 195.000.000 The price of the old machine The price of the old machine Rp.182.000.000Rp.182.000.000 Accumulated depreciation Accumulated depreciation Rp. 75.000.000 -Rp. 75.000.000 - The book value of the old machine The book value of the old machine Rp. 107.000.000 -Rp. 107.000.000 -

the difference between the book valuethe difference between the book value Rp. 88.000.000Rp. 88.000.000

Aktiva TetapAktiva Tetap 1414

** add cash add cash Rp. 90.000.000 Rp. 90.000.000the difference between the book valuethe difference between the book value Rp. 88.000.000Rp. 88.000.000additionaladditional Rp. 90.000.000 -Rp. 90.000.000 -

LossLoss Rp. 2.000.000Rp. 2.000.000

Journal :Journal :

The new engineThe new engine Rp. 195.000.000Rp. 195.000.000accumulated depreciationaccumulated depreciation Rp. 75.000.000Rp. 75.000.000Loss on exchangeLoss on exchange Rp. 2.000.000Rp. 2.000.000

old machineold machine Rp. 182.000.000Rp. 182.000.000cashcash Rp. 90.000.000Rp. 90.000.000

**add cash Rp. 62.000.000add cash Rp. 62.000.000the difference between the book valuethe difference between the book value Rp. 88.000.000Rp. 88.000.000additionaladditional Rp. 62.000.000 -Rp. 62.000.000 -

profitprofit Rp. 26.000.000Rp. 26.000.000

Jurnal :Jurnal :old machineold machine Rp. 182.000.000Rp. 182.000.000accumulated depreciationaccumulated depreciation Rp. 75.000.000Rp. 75.000.000

The new engineThe new engine Rp. 195.000.000Rp. 195.000.000cashcash Rp. 62.000.000Rp. 62.000.000

Aktiva TetapAktiva Tetap 1515

Tukar tambah tidak sejenis:Tukar tambah tidak sejenis:

Example:Example:

a box car with a purchase price of Rp. Rp 150,000,000 has been a box car with a purchase price of Rp. Rp 150,000,000 has been depreciated. 50,000,000 on the 2nd of January 2012 exchanged with depreciated. 50,000,000 on the 2nd of January 2012 exchanged with a truck at a price of Rp. 200,000,000a truck at a price of Rp. 200,000,000

Requested:Requested:Keep a journal to add cash:Keep a journal to add cash:- cash Rp. 120.000.000- cash Rp. 120.000.000- cash Rp. 95.000.000- cash Rp. 95.000.000

Answer:Answer:

The purchase price machineThe purchase price machine Rp. 200.000.000Rp. 200.000.000The price of the old machineThe price of the old machine Rp.150.000.000Rp.150.000.000Accumulated depreciationAccumulated depreciation Rp. 50.000.000 -Rp. 50.000.000 -The book value of the old machineThe book value of the old machine Rp. 100.000.000 -Rp. 100.000.000 - the difference between the book value the difference between the book value Rp. 100.000.000Rp. 100.000.000

Aktiva TetapAktiva Tetap 1616

**add cash Rp. 120.000.000add cash Rp. 120.000.000the difference between the book valuethe difference between the book value Rp.100.000.000Rp.100.000.000additionaladditional Rp.120.000.000 -Rp.120.000.000 -

lossloss Rp. 20.000.000Rp. 20.000.000

Journal :Journal :The new engineThe new engine Rp.200.000.000Rp.200.000.000accumulated depreciationaccumulated depreciation Rp. 50.000.000Rp. 50.000.000Loss on exchangeLoss on exchange Rp. 20.000.000Rp. 20.000.000

old machineold machine Rp. 150.000.000Rp. 150.000.000cashcash Rp. 120.000.000Rp. 120.000.000

**add cash Rp.95.000.000add cash Rp.95.000.000the difference between the book valuethe difference between the book value Rp.100.000.000Rp.100.000.000additionaladditional Rp. 95.000.000 -Rp. 95.000.000 -

ProfitProfit Rp. 5.000.000Rp. 5.000.000

Journal :Journal :The new engineThe new engine Rp.200.000.000Rp.200.000.000accumulated depreciationaccumulated depreciation Rp. 50.000.000Rp. 50.000.000

old machineold machine Rp.150.000.000Rp.150.000.000

cashcash Rp. 95.000.000Rp. 95.000.000Gain on exchangeGain on exchange Rp. 5.000.000Rp. 5.000.000

Aktiva TetapAktiva Tetap 1717

PENUTUPPENUTUP

Dari semua atau hasil dari makalah saya ini mungkin belum Dari semua atau hasil dari makalah saya ini mungkin belum mencapai titik kesempurnaan, maka dari itu saya mengucapkan mencapai titik kesempurnaan, maka dari itu saya mengucapkan mohon maaf atas segala kekurangan dengan makalah ini. Dan saya mohon maaf atas segala kekurangan dengan makalah ini. Dan saya terima kasih atas guru pembimbing saya Ibu Lestari Manurung S,sd terima kasih atas guru pembimbing saya Ibu Lestari Manurung S,sd dan teman-teman yang sudah sedikit membantu saya dan dan teman-teman yang sudah sedikit membantu saya dan menyemangati saya dalam membuat makalah ini. Saya berharap menyemangati saya dalam membuat makalah ini. Saya berharap agar makalah ini bisa bermanfaat dengan baik dan dapat dimengerti.agar makalah ini bisa bermanfaat dengan baik dan dapat dimengerti. Saya menerima akan kritik dan sarannya terhadap teman-teman Saya menerima akan kritik dan sarannya terhadap teman-teman sekitar. Atas perhatiannya saya ucapkan terima kasih.sekitar. Atas perhatiannya saya ucapkan terima kasih.NamaNama : Nova Nadia Putri: Nova Nadia Putri

Tempat tanggal lahirTempat tanggal lahir : Jakarta, : Jakarta, 02 november 199702 november 1997

Twitter : @NovaNdyaTwitter : @NovaNdyaEmail : Email : [email protected]@yahoo.co.id

Menurut saya, kesuksesan berawal Menurut saya, kesuksesan berawal dari kemauan jika ada kemauan semuadari kemauan jika ada kemauan semua akan terlaksana. Belajarlah dari akan terlaksana. Belajarlah dari kegagalan karena kegagalan karena KESUKSESANKESUKSESAN menunggu kita di Masa Depan.menunggu kita di Masa Depan.

Jakarta, November 2013Jakarta, November 2013

Nova Nadia Putri

Aktiva Tetap 18

DAFTAR PUSTAKA

Harti, Dwi.2008,Modul Akuntansi 2B untuk SMK dan MAK, Jakarta, Erlangga.

www. Google Translate.com

Aktiva TetapAktiva Tetap 1919