struktur biaya

TRANSCRIPT

Principles of Engineering Economic Analysis, 5th edition

Bab 16Bab 16Mendapatkan dan

Mengestimasi

Cash Flows

Principles of Engineering Economic Analysis, 5th edition

Think of Chapter 16 as Two Separate but Related Topics

1. Terminologi ongkos dan estimasi – untuk mengerti dan membuat cash flows (16.1-16.3)

2. Prinsip2 Akuntansi – untuk mengerti dan membantu analisa ekonomi dari sisi perspektip bisnis (16.4-16.5)

Principles of Engineering Economic Analysis, 5th edition

Terminologi Ongkos dan Estimasi (16.1-16.3)

• Pendahuluan Mengapa hal ini penting?

• Five Cost Viewpoints Different perspectives yield different insights

• Estimasi Biaya Mencari nilai numeris

Principles of Engineering Economic Analysis, 5th edition

Mengapa Hal ini Penting?(16-1)

Pengambilan keputusan ekonomi membutuhkan pengumpulan data dari nilai dan waktu cash flow. Dibutuhkan sumber yg bervariasi. Pengumpulan cash flow yang relevan. Cash flows perlu diinterpetasikan secara

benar..

Principles of Engineering Economic Analysis, 5th edition

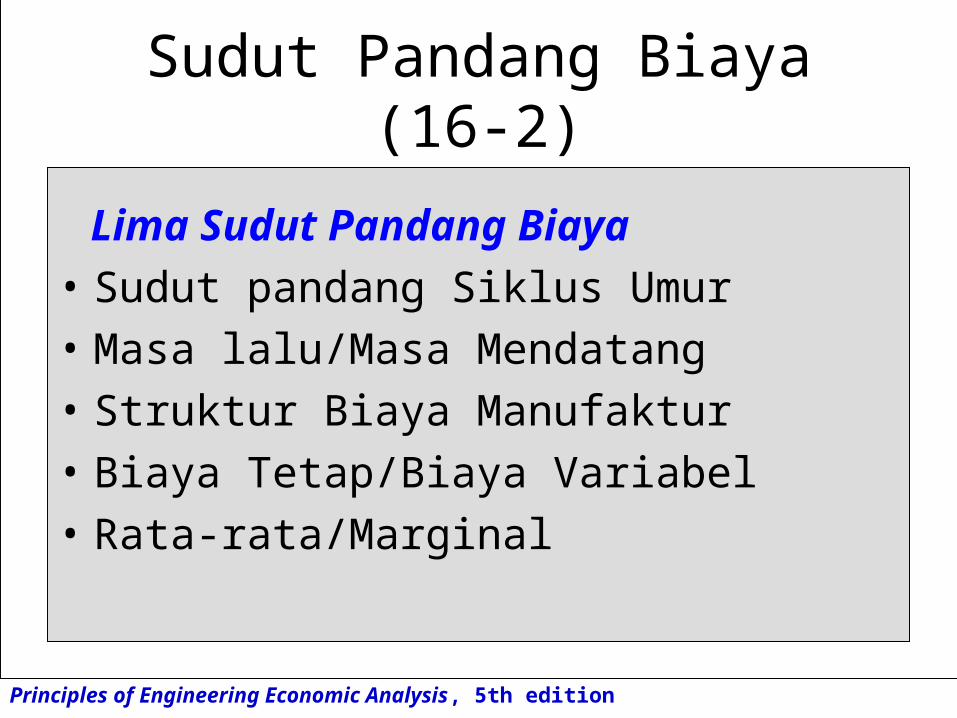

Sudut Pandang Biaya(16-2)

Lima Sudut Pandang Biaya

• Sudut pandang Siklus Umur

• Masa lalu/Masa Mendatang

• Struktur Biaya Manufaktur

• Biaya Tetap/Biaya Variabel

• Rata-rata/Marginal

Principles of Engineering Economic Analysis, 5th edition

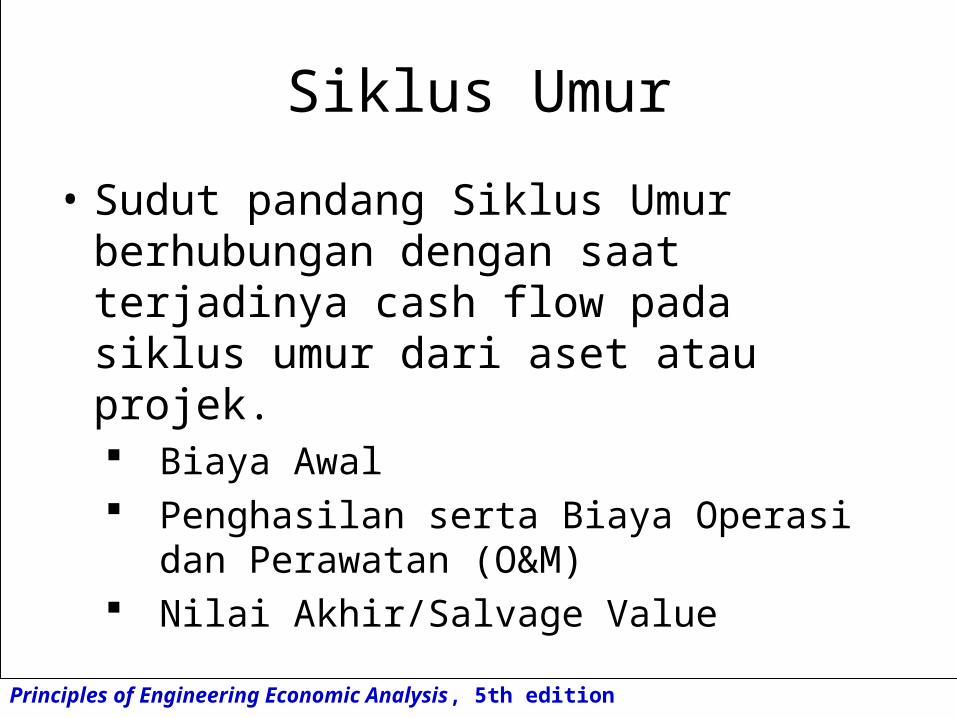

Siklus Umur

• Sudut pandang Siklus Umur berhubungan dengan saat terjadinya cash flow pada siklus umur dari aset atau projek. Biaya Awal Penghasilan serta Biaya Operasi dan

Perawatan (O&M) Nilai Akhir/Salvage Value

Principles of Engineering Economic Analysis, 5th edition

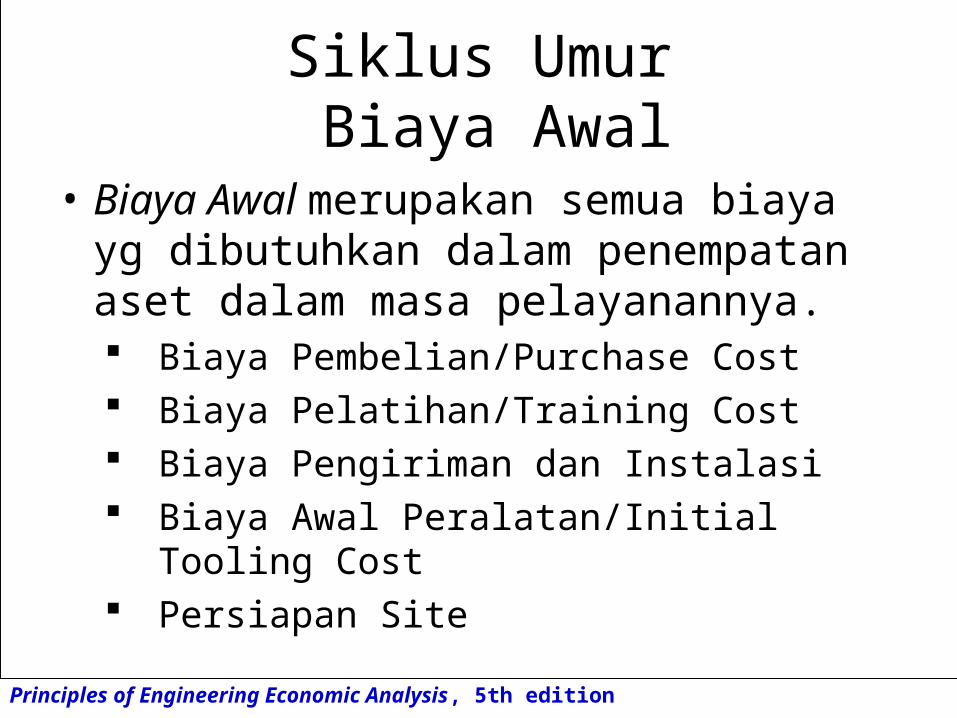

Siklus UmurBiaya Awal

• Biaya Awal merupakan semua biaya yg dibutuhkan dalam penempatan aset dalam masa pelayanannya. Biaya Pembelian/Purchase Cost Biaya Pelatihan/Training Cost Biaya Pengiriman dan Instalasi Biaya Awal Peralatan/Initial Tooling Cost Persiapan Site

Principles of Engineering Economic Analysis, 5th edition

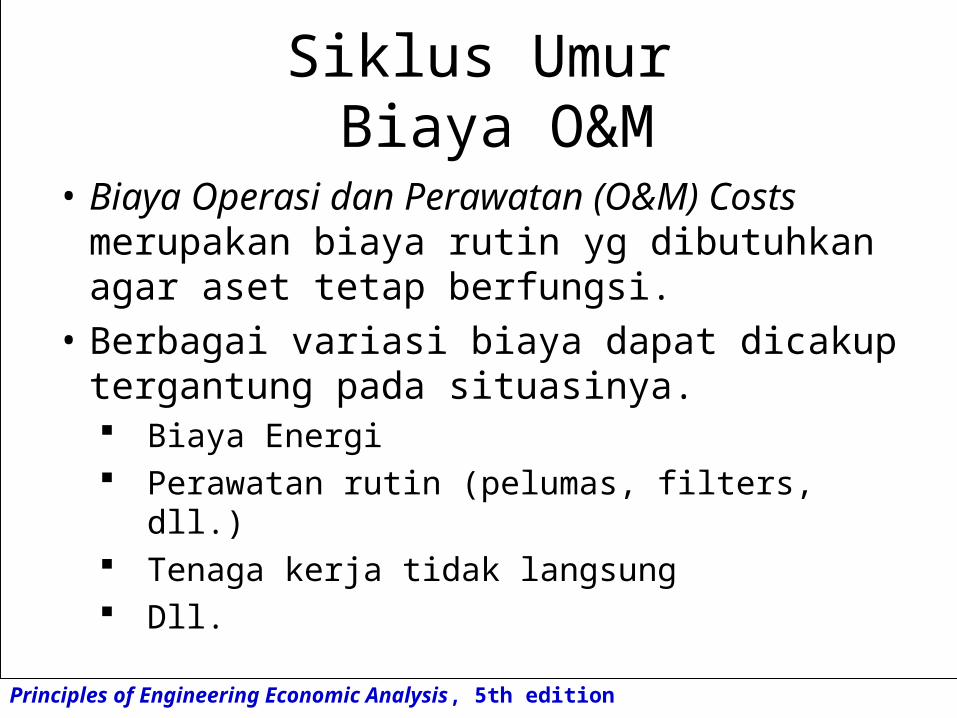

Siklus UmurBiaya O&M

• Biaya Operasi dan Perawatan (O&M) Costs merupakan biaya rutin yg dibutuhkan agar aset tetap berfungsi.

• Berbagai variasi biaya dapat dicakup tergantung pada situasinya. Biaya Energi Perawatan rutin (pelumas, filters, dll.) Tenaga kerja tidak langsung Dll.

Principles of Engineering Economic Analysis, 5th edition

Siklus UmurPenghasilan Operasi

• Penghasilan Operasi semua penghasilan sbg hasil dari kepemilikan dan penggunaan aset.

• Penghasilan biasanya di estimasi berdasarkan volume dan nilai parts yg memanfaatkan atau hasil proyek.

• Penghasilan ini tidak terjadi selam aset atau prok tidak termanfaatkan.

Principles of Engineering Economic Analysis, 5th edition

Siklus UmurNiali Akhir/Salvage Value

• Nilai Akhir/alvage Value adalah hasil cash flow bersih/net dari pelepasan aset atau saat akhir projek.

• Salvage Value dapat bernilai positip atau or negatip.

• Salvage Value didapat dari pengurang biaya pelapasan dari nilai pasar pada saat aset dilepas.

• Salvage value biasanya yg paling suli di estimasi.

Principles of Engineering Economic Analysis, 5th edition

Masa Lalu/Masa Mendatang

• Masa Lalu/Masa Mendatang fokus pada bilamana terjadinya biaya dan pendapatan relatip terhadap “saat ini”.

• Biaya masa lalu adalah semua biaya yang terjadi sebelum “saat ini”.

• Biaya masa mendatang adalah segala biaya yg diharapkan akan terjadi setelah “sdaat ini”.

• Interpretasi yg sama berlaku terhadap ppendapatan masa lalu dan pendapatan masa mendatang.

Principles of Engineering Economic Analysis, 5th edition

Masa Lalu/Masa MendatangTerminologi Tambahan

• Sunk Cost adalah setiap biaya masa lalu yg tidak dapat dikembalikan.

• Read Examples 16.2 and 16.3 for additional insight.

• Opportunity Cost adalah biaya kesempatan untuk mendapatkan bunga ataupun return.

• Dana terinvestasi adalah salah satu kesempatan untuk tidak dapat digunakan pada keperluan lain .

• Perbedaan harapan pengembalian adalah pilihan biaya kesempatan.

• Biaya kesempatan tahunan untuyk menyimpan Rp. 6 milyar adalah Rp.900 juta apbl diasumsikan suku bunga sebesar 15%/tahun.

Principles of Engineering Economic Analysis, 5th edition

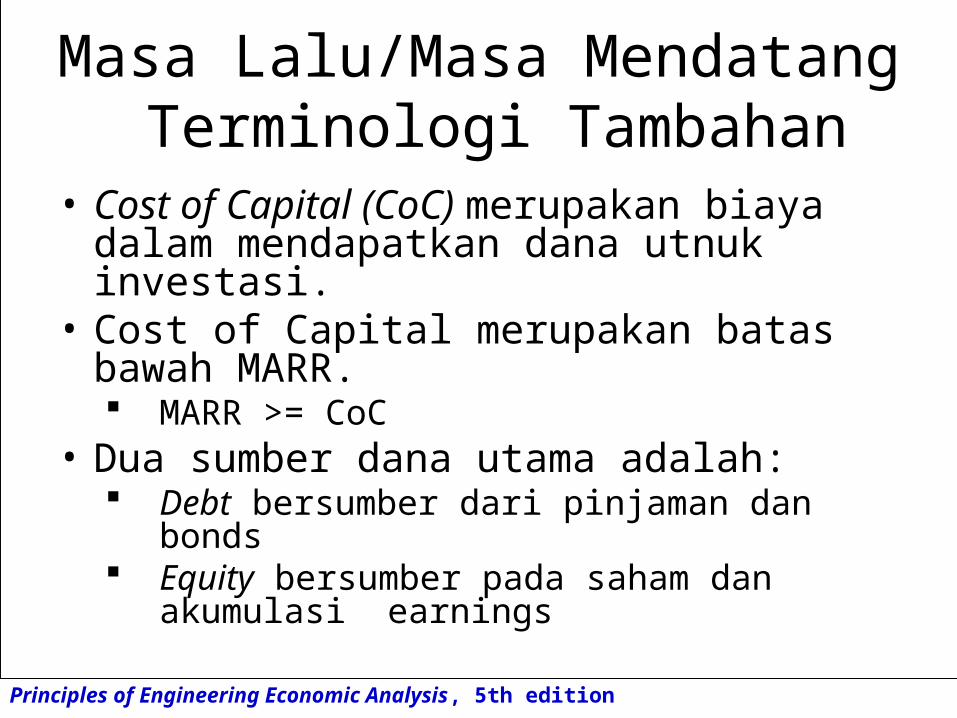

Masa Lalu/Masa MendatangTerminologi Tambahan

• Cost of Capital (CoC) merupakan biaya dalam mendapatkan dana utnuk investasi.

• Cost of Capital merupakan batas bawah MARR. MARR >= CoC

• Dua sumber dana utama adalah: Debt bersumber dari pinjaman dan bonds Equity bersumber pada saham dan akumulasi

earnings

Principles of Engineering Economic Analysis, 5th edition

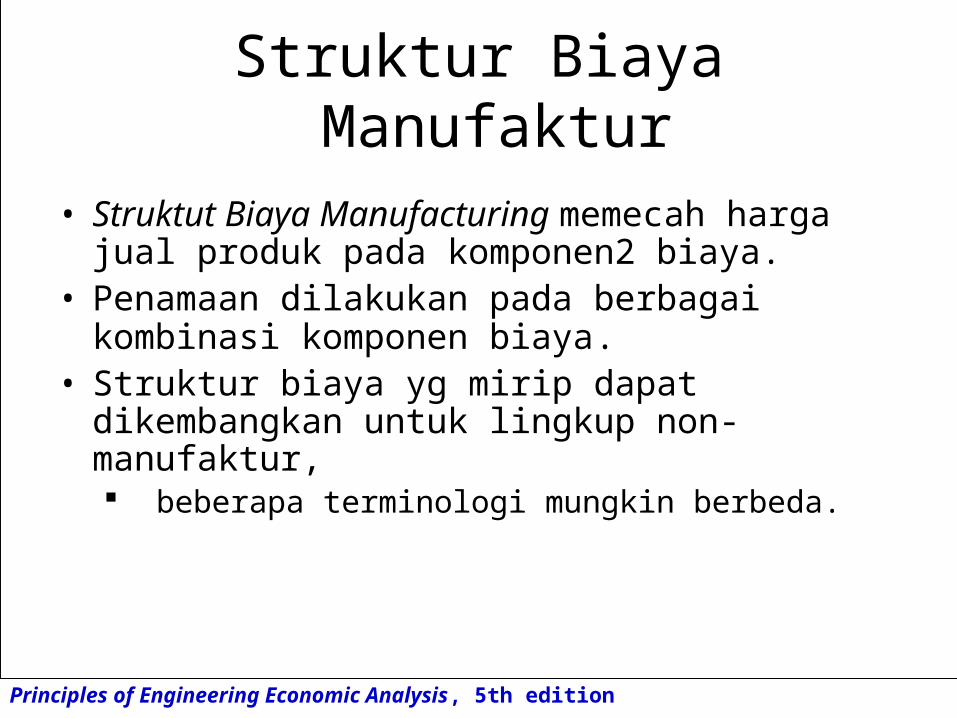

Struktur Biaya Manufaktur

• Struktut Biaya Manufacturing memecah harga jual produk pada komponen2 biaya.

• Penamaan dilakukan pada berbagai kombinasi komponen biaya.

• Struktur biaya yg mirip dapat dikembangkan untuk lingkup non-manufaktur, beberapa terminologi mungkin berbeda.

Principles of Engineering Economic Analysis, 5th edition

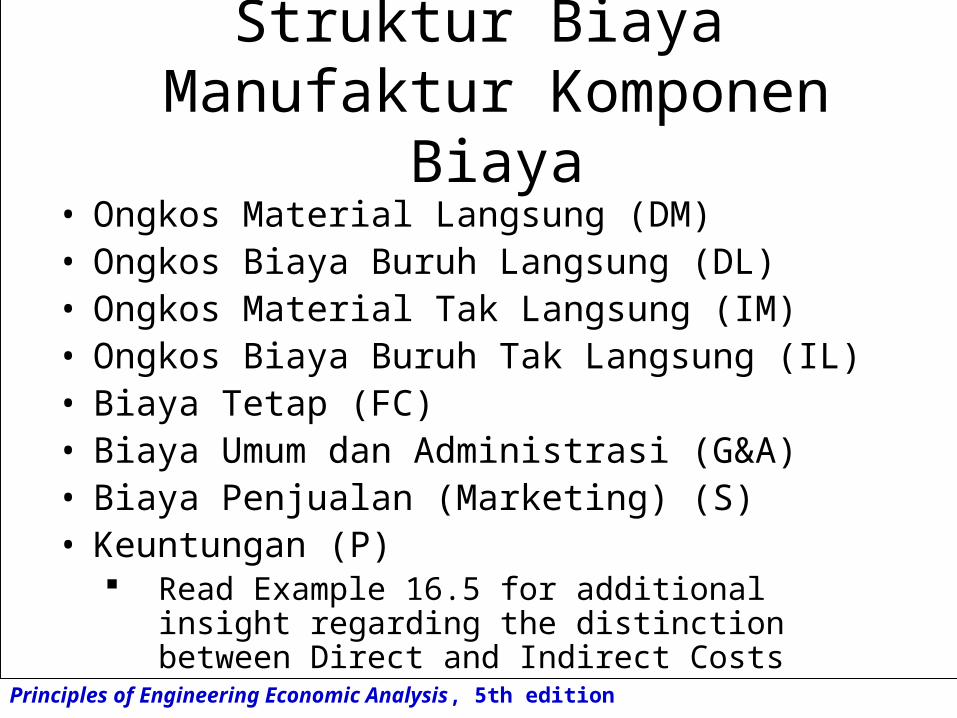

Struktur Biaya Manufaktur Komponen Biaya

• Ongkos Material Langsung (DM)• Ongkos Biaya Buruh Langsung (DL)• Ongkos Material Tak Langsung (IM)• Ongkos Biaya Buruh Tak Langsung (IL)• Biaya Tetap (FC)• Biaya Umum dan Administrasi (G&A)• Biaya Penjualan (Marketing) (S)• Keuntungan (P)

Read Example 16.5 for additional insight regarding the distinction between Direct and Indirect Costs

Principles of Engineering Economic Analysis, 5th edition

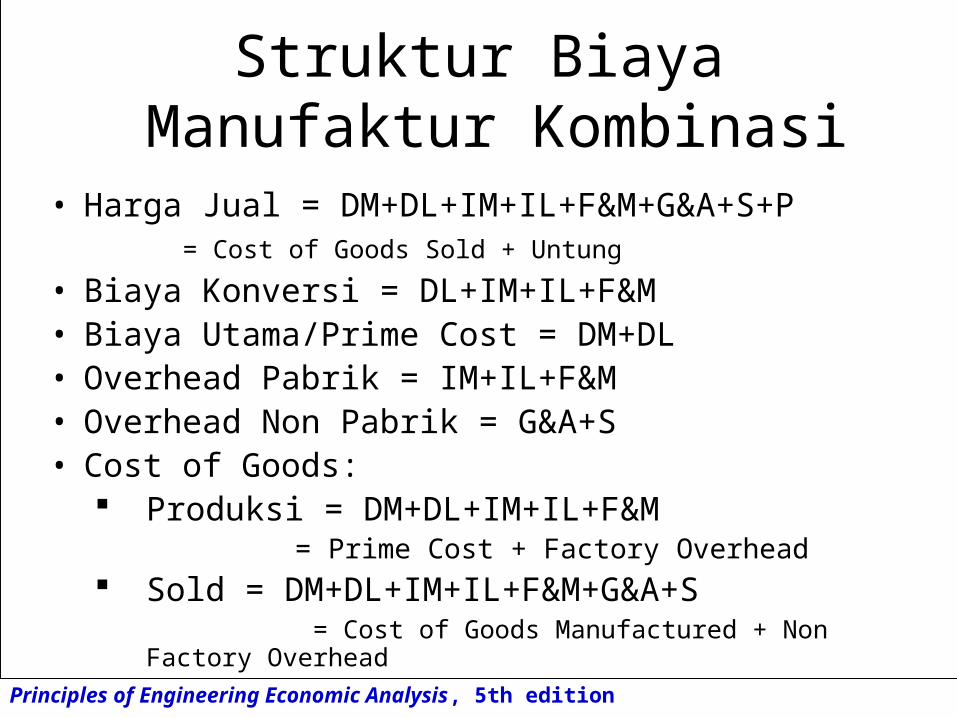

Struktur Biaya Manufaktur Kombinasi

• Harga Jual = DM+DL+IM+IL+F&M+G&A+S+P = Cost of Goods Sold + Untung

• Biaya Konversi = DL+IM+IL+F&M• Biaya Utama/Prime Cost = DM+DL• Overhead Pabrik = IM+IL+F&M• Overhead Non Pabrik = G&A+S• Cost of Goods:

Produksi = DM+DL+IM+IL+F&M = Prime Cost + Factory

Overhead Sold = DM+DL+IM+IL+F&M+G&A+S

= Cost of Goods Manufactured + Non Factory Overhead

Principles of Engineering Economic Analysis, 5th edition

Biaya Tetap dan Variabel

• Biaya Tetap (FC) semua biaya yg tidak bervariasi terhadap output. MIsalkan; biaya sewa, depresiasi, penerangan

dan gaji supervisor. Fixed Costs biasany bersifat tetap sepanjang

jumlah produksi tertentu, yang disebut relevant range.

Sebagai contoh gaji supervisor ataupun penerangan bersifat tetap untuk satu shift operasi tetapi akian meningkat untuk dua shift operasi.

Principles of Engineering Economic Analysis, 5th edition

Biaya Tetap dan Variabel

• Biaya Variabel (VC) adalah biaya yg bervariasi terhadap proporsi jumlah output. Umumnya terdiri dari biaya meteraial langsung

dan biaya buruh langsung. Biasanya direpesentasikan sebagai fungsi linier

dari output• VC(x) = rate * x; where x is the level of production

• Biaya Total adalah jumlah dari biaya tetap dan biaya variabel

TC(x) = FC + VC(x)

Principles of Engineering Economic Analysis, 5th edition

Breakeven

• Total Revenue (TR) adalah jumlah pengdapatandari penjualan unit produksi.

• Total Revenue seringkali direpresentasikan sebagai fungsi linier dari jumlah unit terjual.

• TR(x) = harga * x; where x is the number of units sold

• Apbl diasumsikan inventory bersifat tetap maka jumlah unit terjual sama dengan jumlah unit produksi.

• Titik Breakeven, adalah dimana biaya total sama dengan biaya pendapatan

TR(x) = FC + VC(x)

Principles of Engineering Economic Analysis, 5th edition

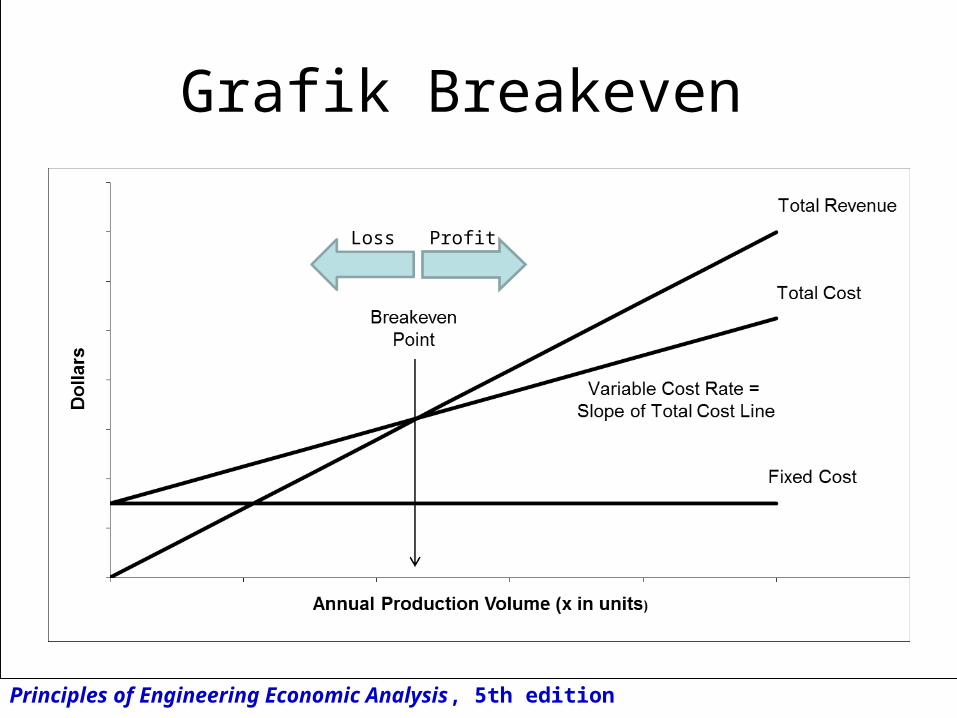

Grafik Breakeven

ProfitLoss

Principles of Engineering Economic Analysis, 5th edition

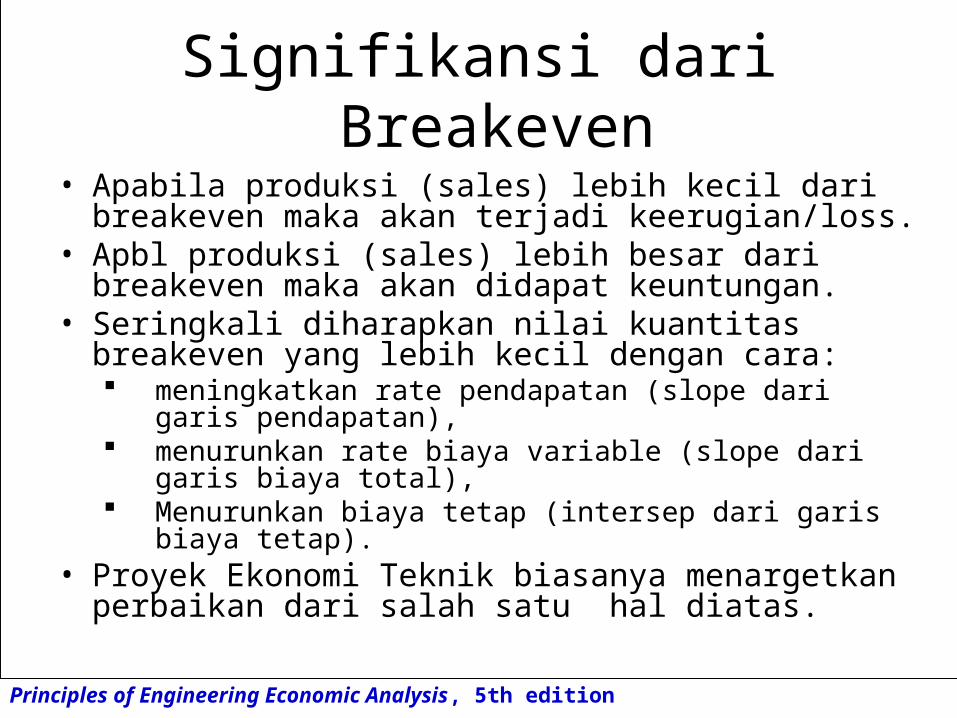

Signifikansi dari Breakeven

• Apabila produksi (sales) lebih kecil dari breakeven maka akan terjadi keerugian/loss.

• Apbl produksi (sales) lebih besar dari breakeven maka akan didapat keuntungan.

• Seringkali diharapkan nilai kuantitas breakeven yang lebih kecil dengan cara: meningkatkan rate pendapatan (slope dari garis

pendapatan), menurunkan rate biaya variable (slope dari garis biaya

total), Menurunkan biaya tetap (intersep dari garis biaya tetap).

• Proyek Ekonomi Teknik biasanya menargetkan perbaikan dari salah satu hal diatas.

Principles of Engineering Economic Analysis, 5th edition

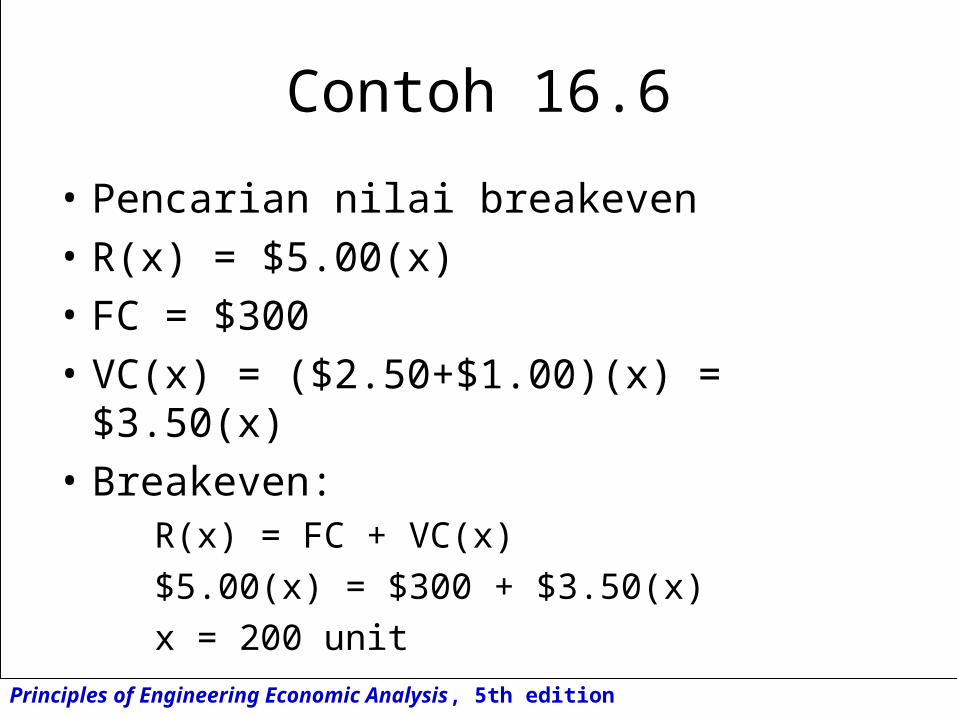

Contoh 16.6

• Pencarian nilai breakeven

• R(x) = $5.00(x)

• FC = $300

• VC(x) = ($2.50+$1.00)(x) = $3.50(x)

• Breakeven:R(x) = FC + VC(x)

$5.00(x) = $300 + $3.50(x)

x = 200 unit

Principles of Engineering Economic Analysis, 5th edition

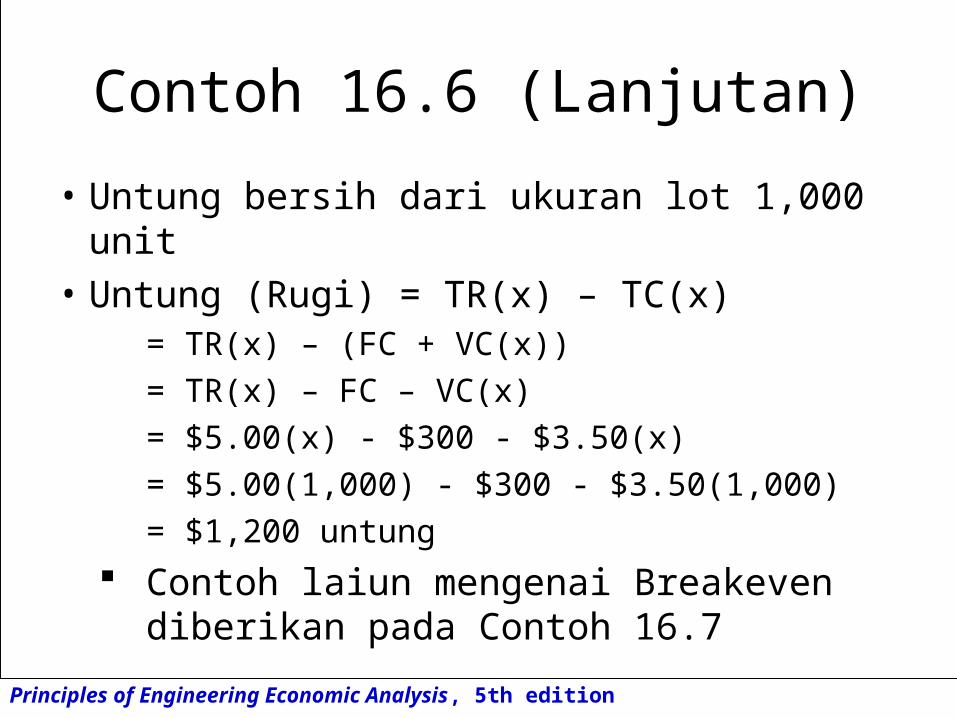

Contoh 16.6 (Lanjutan)

• Untung bersih dari ukuran lot 1,000 unit

• Untung (Rugi) = TR(x) – TC(x)= TR(x) – (FC + VC(x))

= TR(x) – FC – VC(x)

= $5.00(x) - $300 - $3.50(x)

= $5.00(1,000) - $300 - $3.50(1,000)

= $1,200 untung

Contoh laiun mengenai Breakeven diberikan pada Contoh 16.7

Principles of Engineering Economic Analysis, 5th edition

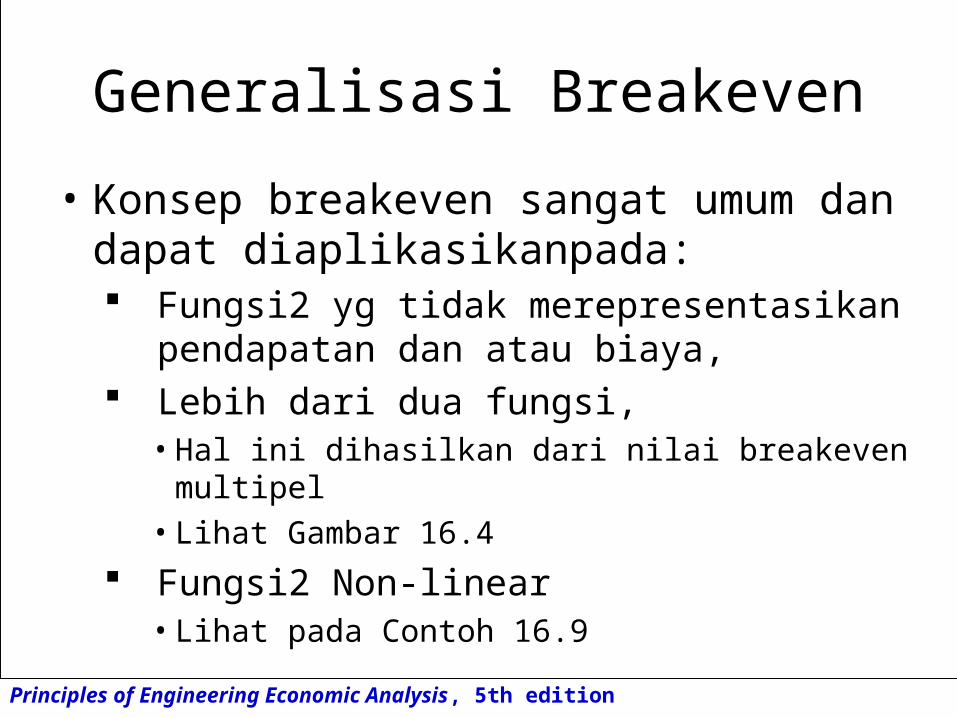

Generalisasi Breakeven

• Konsep breakeven sangat umum dan dapat diaplikasikanpada: Fungsi2 yg tidak merepresentasikan

pendapatan dan atau biaya, Lebih dari dua fungsi,

• Hal ini dihasilkan dari nilai breakeven multipel• Lihat Gambar 16.4

Fungsi2 Non-linear• Lihat pada Contoh 16.9

Principles of Engineering Economic Analysis, 5th edition

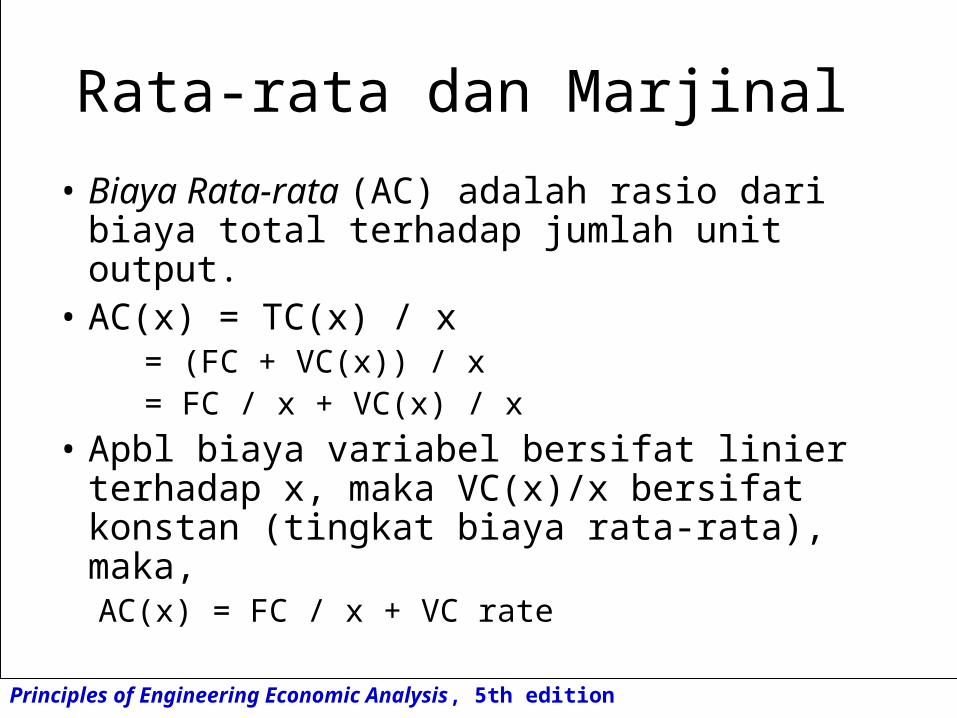

Rata-rata dan Marjinal

• Biaya Rata-rata (AC) adalah rasio dari biaya total terhadap jumlah unit output.

• AC(x) = TC(x) / x= (FC + VC(x)) / x= FC / x + VC(x) / x

• Apbl biaya variabel bersifat linier terhadap x, maka VC(x)/x bersifat konstan (tingkat biaya rata-rata), maka,AC(x) = FC / x + VC rate

Principles of Engineering Economic Analysis, 5th edition

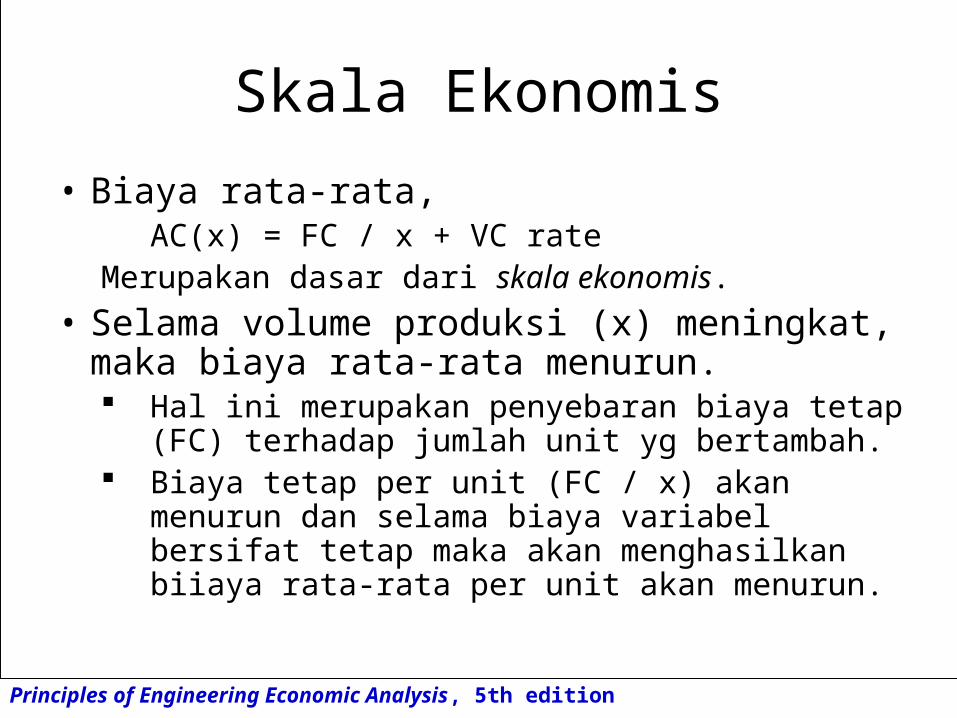

Skala Ekonomis

• Biaya rata-rata,AC(x) = FC / x + VC rate

Merupakan dasar dari skala ekonomis.

• Selama volume produksi (x) meningkat, maka biaya rata-rata menurun. Hal ini merupakan penyebaran biaya tetap (FC)

terhadap jumlah unit yg bertambah. Biaya tetap per unit (FC / x) akan menurun dan

selama biaya variabel bersifat tetap maka akan menghasilkan biiaya rata-rata per unit akan menurun.

Principles of Engineering Economic Analysis, 5th edition

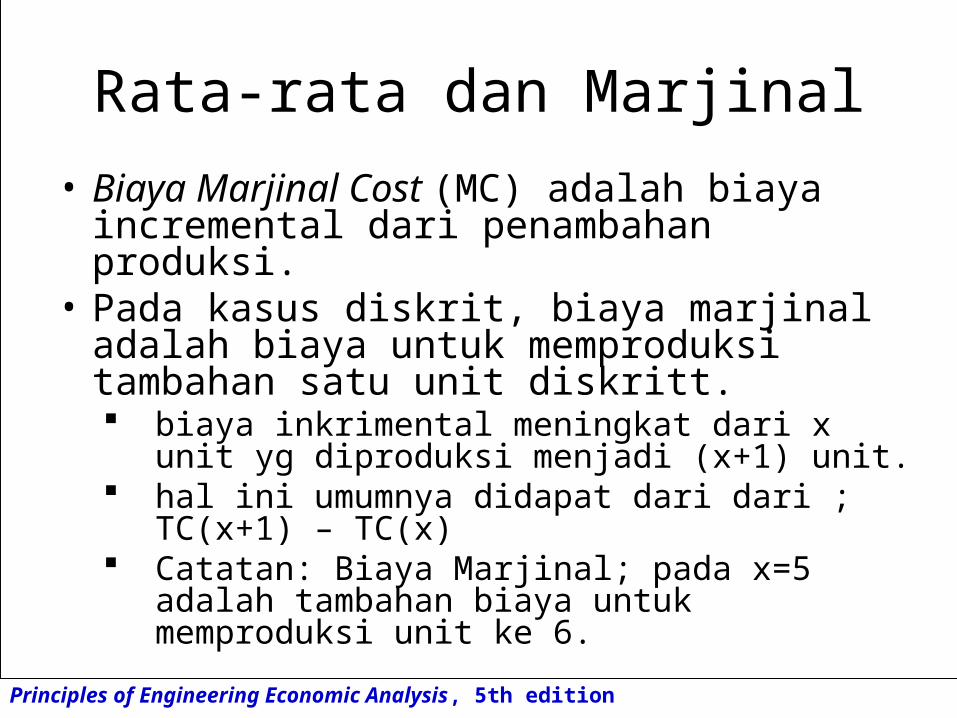

Rata-rata dan Marjinal

• Biaya Marjinal Cost (MC) adalah biaya incremental dari penambahan produksi.

• Pada kasus diskrit, biaya marjinal adalah biaya untuk memproduksi tambahan satu unit diskritt. biaya inkrimental meningkat dari x unit yg

diproduksi menjadi (x+1) unit. hal ini umumnya didapat dari dari ; TC(x+1) –

TC(x) Catatan: Biaya Marjinal; pada x=5 adalah

tambahan biaya untuk memproduksi unit ke 6.

Principles of Engineering Economic Analysis, 5th edition

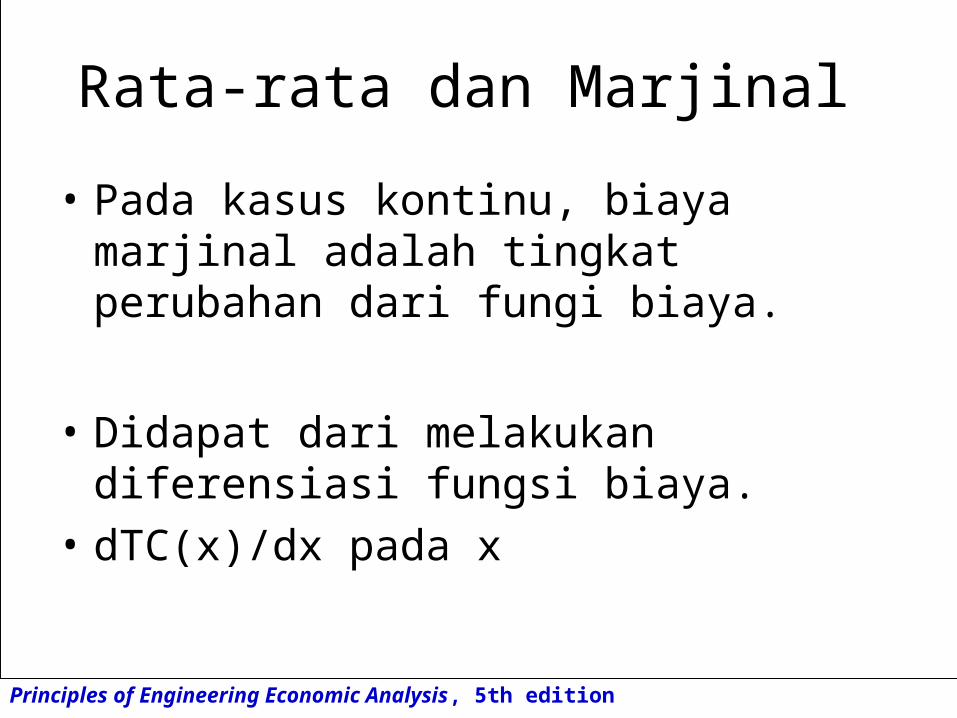

Rata-rata dan Marjinal

• Pada kasus kontinu, biaya marjinal adalah tingkat perubahan dari fungi biaya.

• Didapat dari melakukan diferensiasi fungsi biaya.

• dTC(x)/dx pada x

Principles of Engineering Economic Analysis, 5th edition

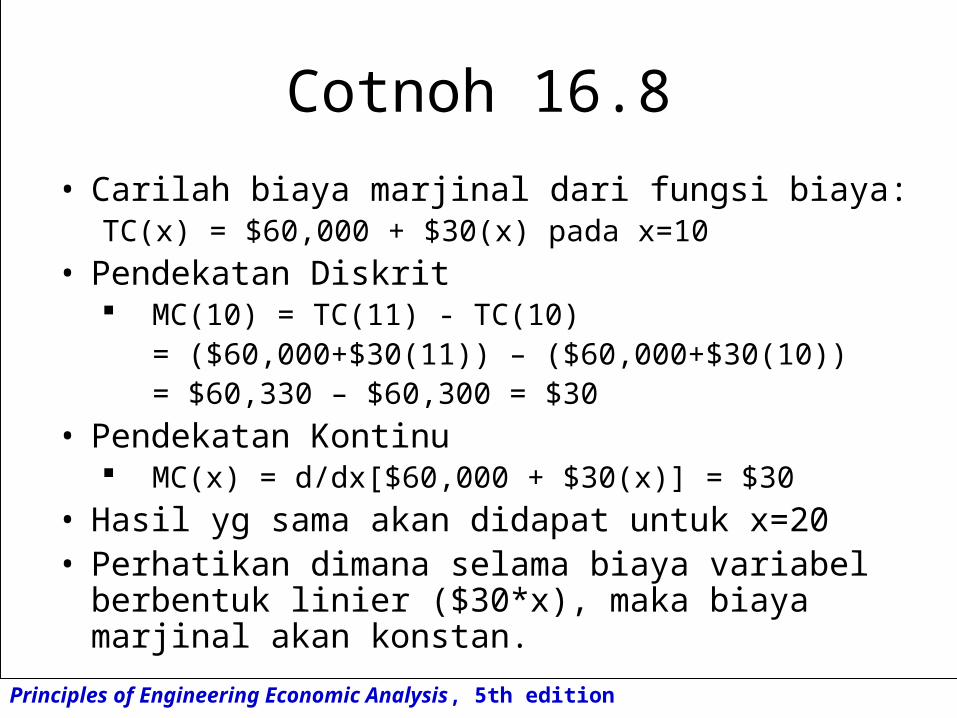

Cotnoh 16.8

• Carilah biaya marjinal dari fungsi biaya: TC(x) = $60,000 + $30(x) pada x=10

• Pendekatan Diskrit MC(10) = TC(11) - TC(10)

= ($60,000+$30(11)) – ($60,000+$30(10))= $60,330 – $60,300 = $30

• Pendekatan Kontinu MC(x) = d/dx[$60,000 + $30(x)] = $30

• Hasil yg sama akan didapat untuk x=20• Perhatikan dimana selama biaya variabel berbentuk

linier ($30*x), maka biaya marjinal akan konstan.

Principles of Engineering Economic Analysis, 5th edition

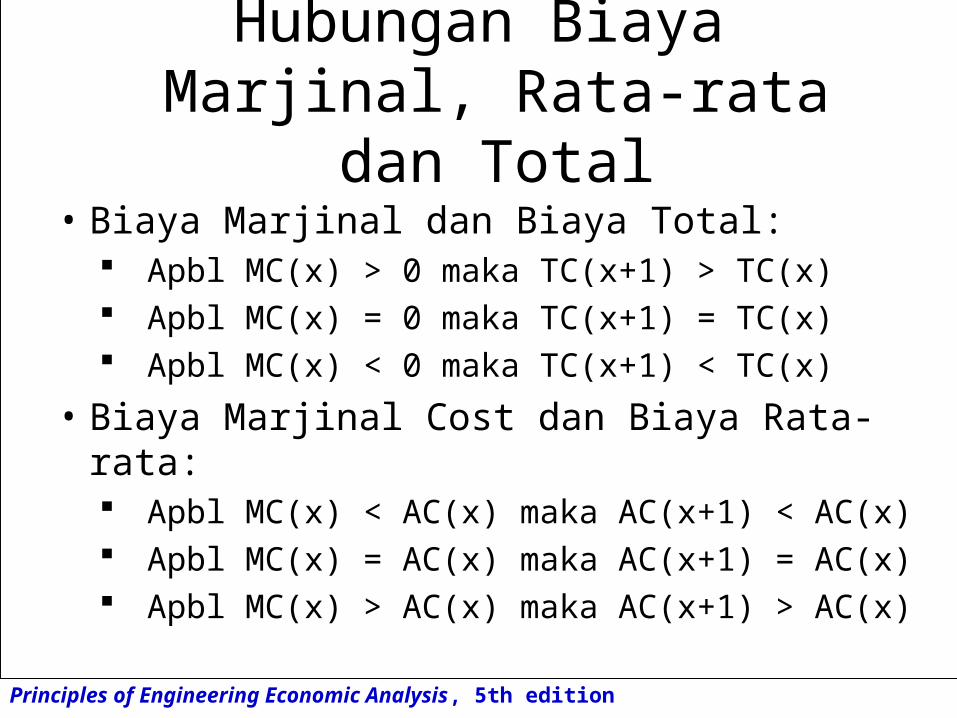

Hubungan BiayaMarjinal, Rata-rata dan Total

• Biaya Marjinal dan Biaya Total: Apbl MC(x) > 0 maka TC(x+1) > TC(x) Apbl MC(x) = 0 maka TC(x+1) = TC(x) Apbl MC(x) < 0 maka TC(x+1) < TC(x)

• Biaya Marjinal Cost dan Biaya Rata-rata: Apbl MC(x) < AC(x) maka AC(x+1) < AC(x) Apbl MC(x) = AC(x) maka AC(x+1) = AC(x) Apbl MC(x) > AC(x) maka AC(x+1) > AC(x)

Principles of Engineering Economic Analysis, 5th edition

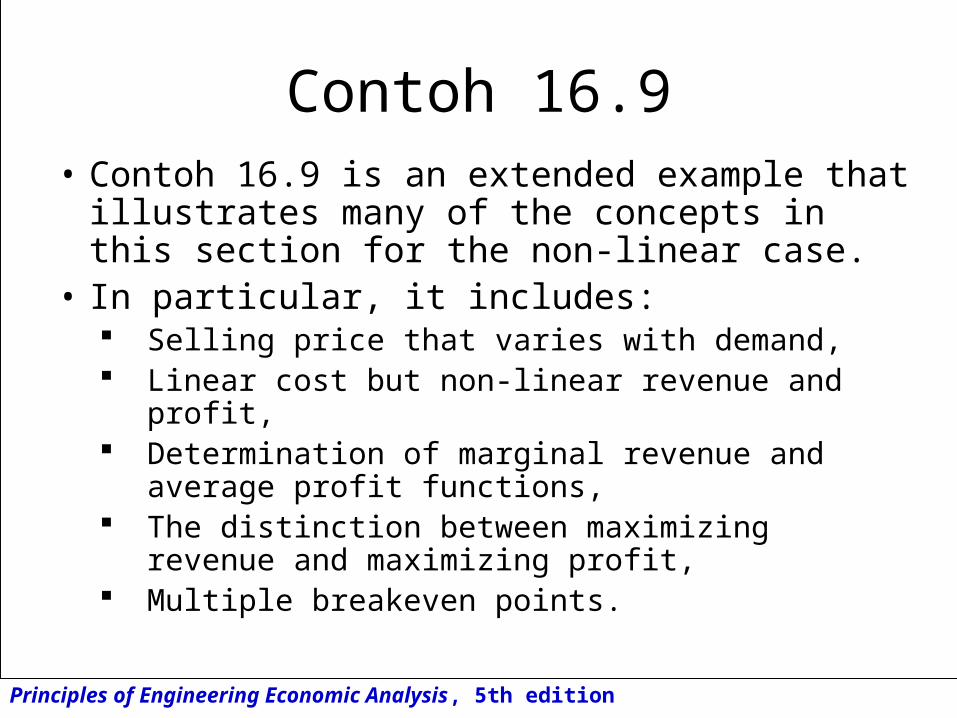

Contoh 16.9• Contoh 16.9 is an extended example that

illustrates many of the concepts in this section for the non-linear case.

• In particular, it includes: Selling price that varies with demand, Linear cost but non-linear revenue and profit, Determination of marginal revenue and average

profit functions, The distinction between maximizing revenue and

maximizing profit, Multiple breakeven points.

Principles of Engineering Economic Analysis, 5th edition

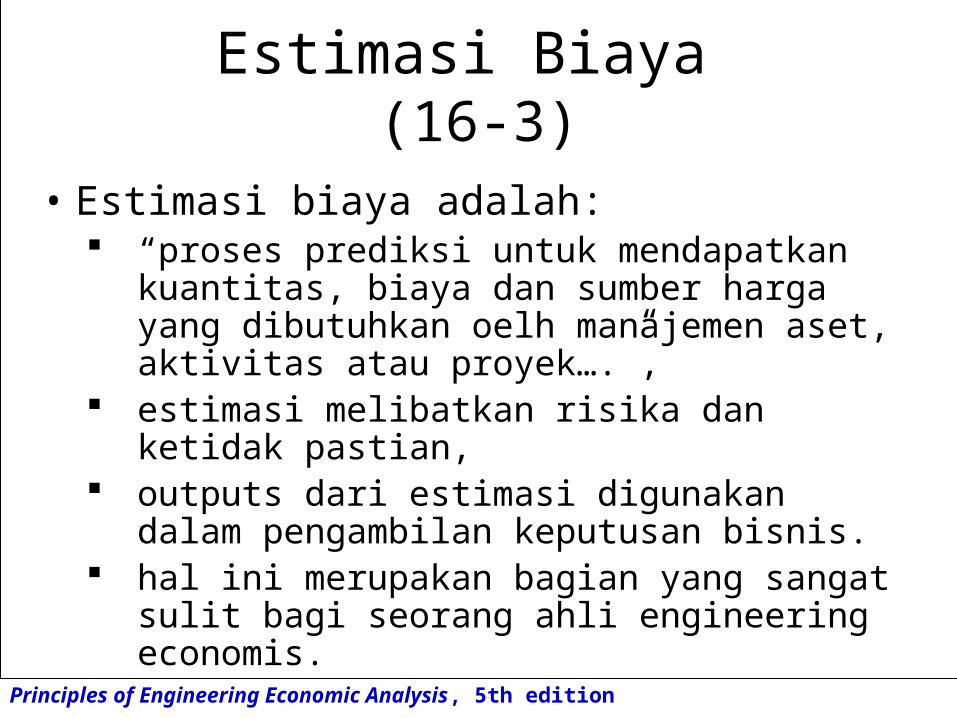

Estimasi Biaya (16-3)

• Estimasi biaya adalah: “proses prediksi untuk mendapatkan

kuantitas, biaya dan sumber harga yang dibutuhkan oelh manajemen aset, aktivitas atau proyek….”,

estimasi melibatkan risika dan ketidak pastian,

outputs dari estimasi digunakan dalam pengambilan keputusan bisnis.

hal ini merupakan bagian yang sangat sulit bagi seorang ahli engineering economis.

Principles of Engineering Economic Analysis, 5th edition

Biaya dari Estimasi• Biaya dalam melakukan estimasi akan

meningkat sehubungan dengan lebih banyaknya informasi rinci yg dicari.

• Perlu dipertimbangkan trade-off dari nilai informasi dengan biaya untuk mendapatkan informasi tersebut.

• Trade-off ini seringkali sulit dievaluasi secara tepat.

Principles of Engineering Economic Analysis, 5th edition

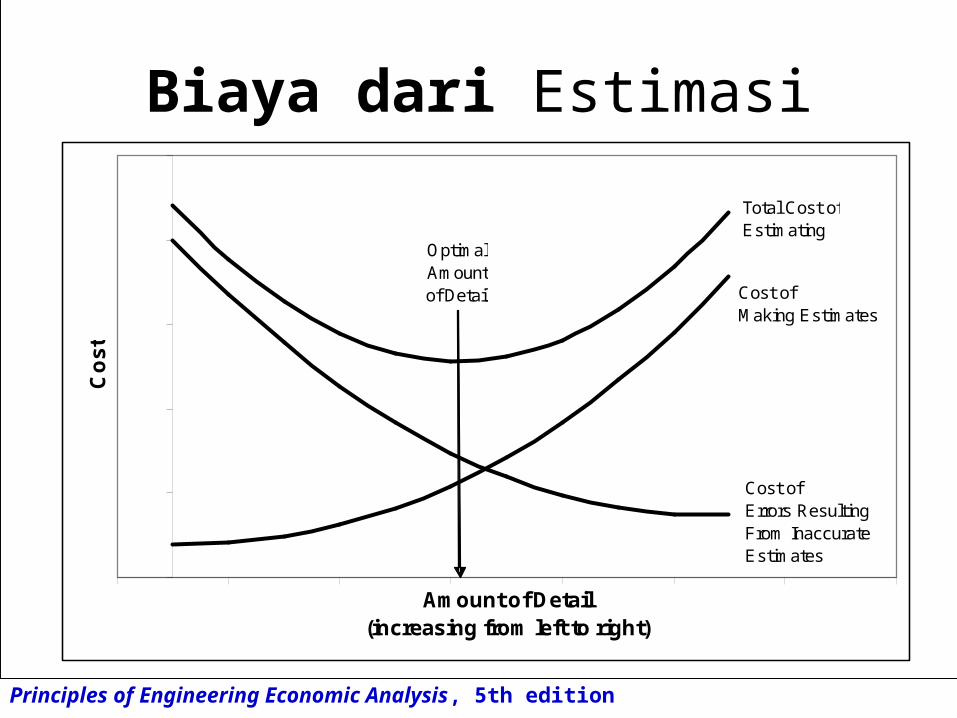

Biaya dari Estimasi

Amount of Detail(increasing from left to right)

Co

st

Cost ofErrors ResultingFrom InaccurateEstimates

Cost ofMaking Estimates

Total Cost ofEstimating

OptimalAmountof Detail

Principles of Engineering Economic Analysis, 5th edition

Empat Kelas Estimasi• Order of Magnitude Estimates

Estimasi kasar berdasarkan pengalaman dan judgment

Tidak diperlukan rincian Berguna dalam pengajuan konsep

• Estimasi Awal Sub-element kunci dipertimbangkan untuk

menambah rincian pada estimate kasar Berguna untuk studi kelayakan

Principles of Engineering Economic Analysis, 5th edition

Empat Kelas Estimasi (Lanjutan)

• Estimasi semi-rinci Semua elemen utama diperhitungkan Berguna dalam rangka pembuatan bujet dan

otorisasi sumber

• Estimasi rinci Semua sub-element diperhitungkan Berguna dalam pelaksanaan dan

pengendalian, penentuan harga dan bidding kontrak

Principles of Engineering Economic Analysis, 5th edition

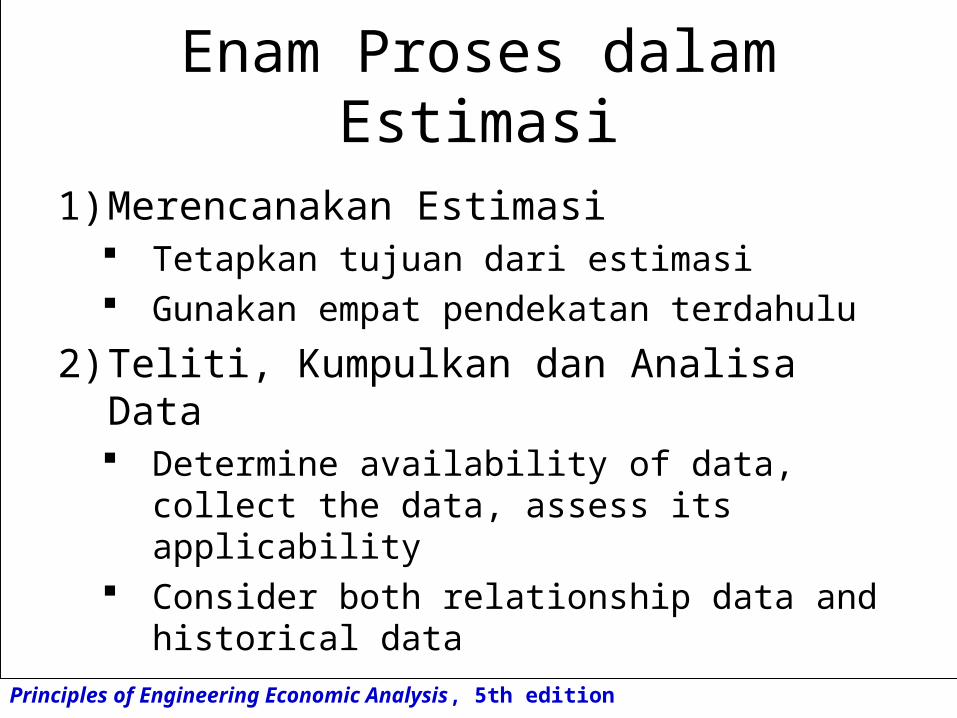

Enam Proses dalam Estimasi

1) Merencanakan Estimasi Tetapkan tujuan dari estimasi Gunakan empat pendekatan terdahulu

2) Teliti, Kumpulkan dan Analisa Data Determine availability of data, collect the

data, assess its applicability Consider both relationship data and

historical data

Principles of Engineering Economic Analysis, 5th edition

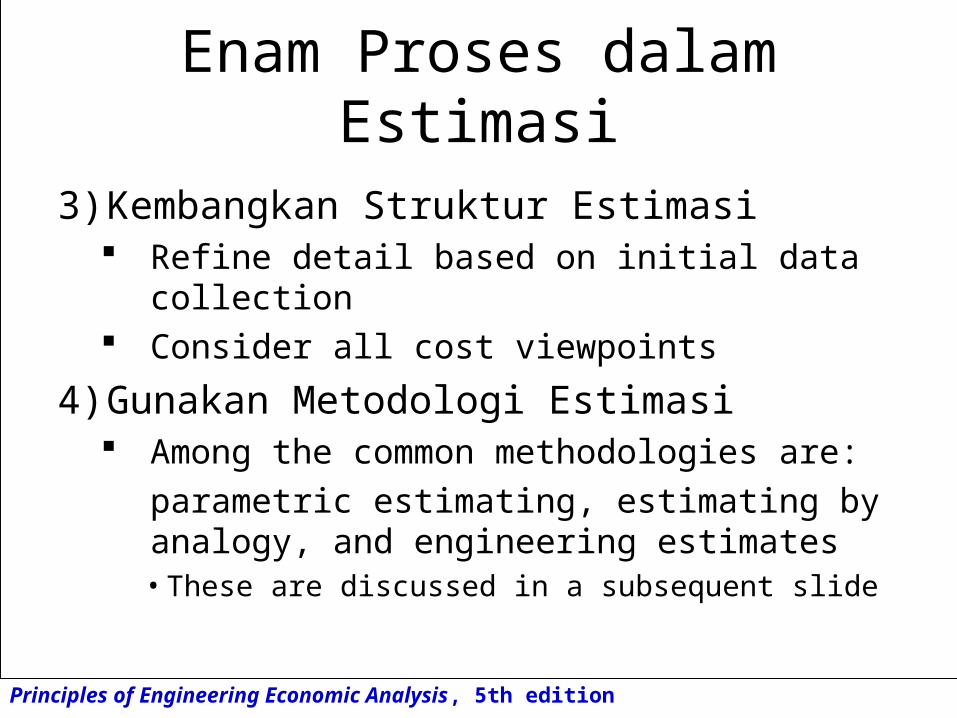

Enam Proses dalam Estimasi

3) Kembangkan Struktur Estimasi Refine detail based on initial data collection Consider all cost viewpoints

4) Gunakan Metodologi Estimasi Among the common methodologies are:

parametric estimating, estimating by analogy, and engineering estimates• These are discussed in a subsequent slide

Principles of Engineering Economic Analysis, 5th edition

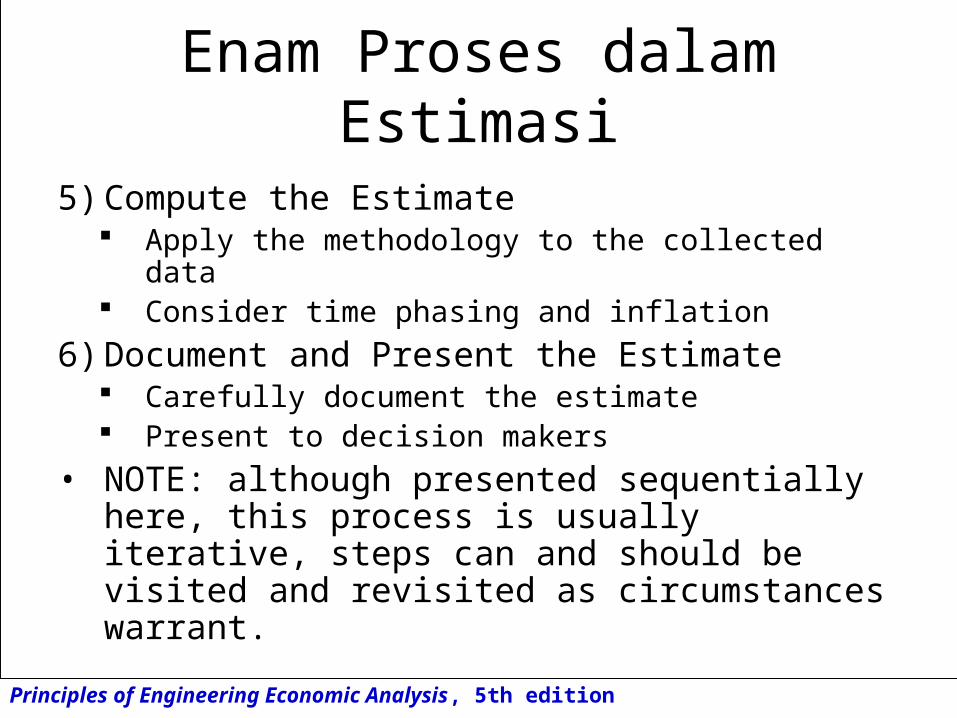

Enam Proses dalam Estimasi

5) Compute the Estimate Apply the methodology to the collected data Consider time phasing and inflation

6) Document and Present the Estimate Carefully document the estimate Present to decision makers

• NOTE: although presented sequentially here, this process is usually iterative, steps can and should be visited and revisited as circumstances warrant.

Principles of Engineering Economic Analysis, 5th edition

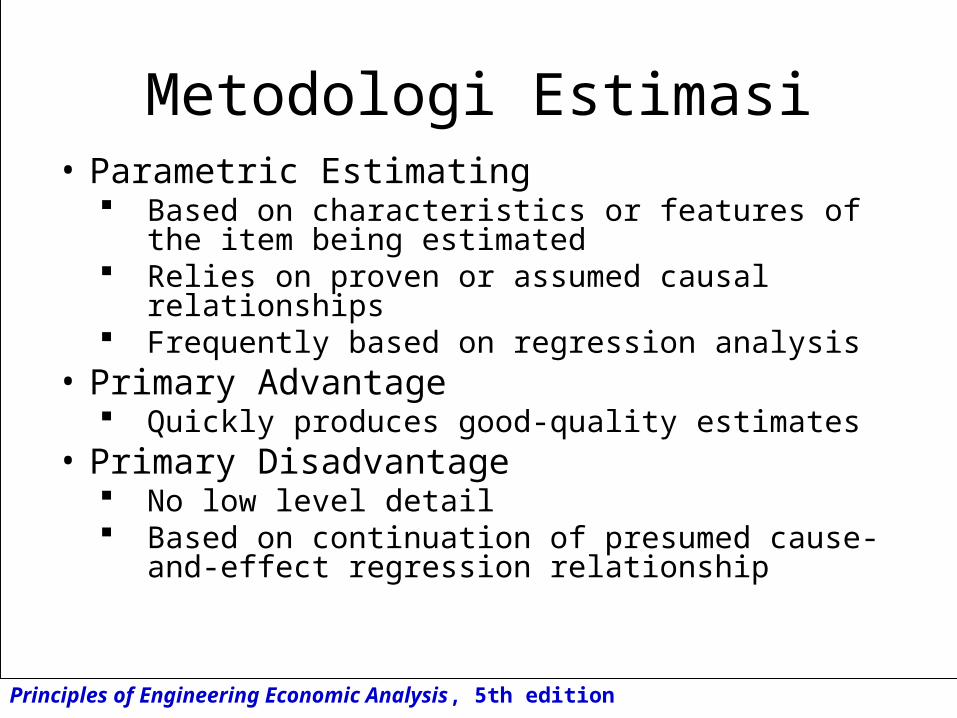

Metodologi Estimasi• Parametric Estimating

Based on characteristics or features of the item being estimated

Relies on proven or assumed causal relationships

Frequently based on regression analysis• Primary Advantage

Quickly produces good-quality estimates• Primary Disadvantage

No low level detail Based on continuation of presumed cause-and-

effect regression relationship

Principles of Engineering Economic Analysis, 5th edition

Metodologi Estimasi (lanjutan)

• Estimating by Analogy Based on the premise that no new project is

totally new Relies on the idea that many cost elements can

be reasonably estimated from a predecessor

• Primary Advantage If a good analogy is found, low level estimates

can be developed quickly

• Primary Disadvantage Dependent upon identification of an appropriate

analogy

Principles of Engineering Economic Analysis, 5th edition

Metodologi Estimasi (lanjutan)

• Engineering Estimating Bottom-up estimating that relies on low-level

engineering analysis and calculations that build to a total

• Primary Advantage Level of detail considered results in highly

credible estimates

• Primary Disadvantage Time and information requirements are high

Principles of Engineering Economic Analysis, 5th edition

Sumber Data

• Pada umumnya sumber data didapat dari internal ataupun eksternal perusahaan.

• Sumber Internal dapat berupa catatan akutansi dan cacatan produksi.

• Sumber Eksternal termasuk dari manufaktur peralatan, asosiasi perdagangan, buku referensi dan pihak pemerintah.

Principles of Engineering Economic Analysis, 5th edition

Prinsip-prinsip Akutansi(16.4-16.5)

Prinsio Akutansi Umum • Balance Sheet• Income Statement• Analisa Rasio

Prinsip Cost Accounting/Akutansi Biaya• Metoda Alokasi Biaya Tradisional• Pembebaanan Biaya berdasarkan Aktivitas• Biaya Standar• Economic Value Added

Principles of Engineering Economic Analysis, 5th edition

Accounting Overview• Akutansi merupakan bahasa bisnis

Ahli Engineering economi harus mengerti bahasa ini agar dapat melakukan cara pengumpulan yg benar, melakukan interpretasi data dan mengkomunikasikan hasilnya pada manejer.

• Aktivitas tg berhubungan dengan data finansial organiasasi adalah: Pencatatan Klasifikasi Summarizing Interpretasi

Principles of Engineering Economic Analysis, 5th edition

Accounting Overview(lanjutan)

• Data Akutansi disimpulkan dalam dua laporan finansial. Balance Sheet merupakan pernyataan yg

menggambarkan kondisi perusahaan pada satu titik waktu.

Income Statement menyimpulkan penerimaan dan pengeluaran perusahaan selama perioda waktu tertentu.

Balance Income BalanceSheet Statement Sheet

Principles of Engineering Economic Analysis, 5th edition

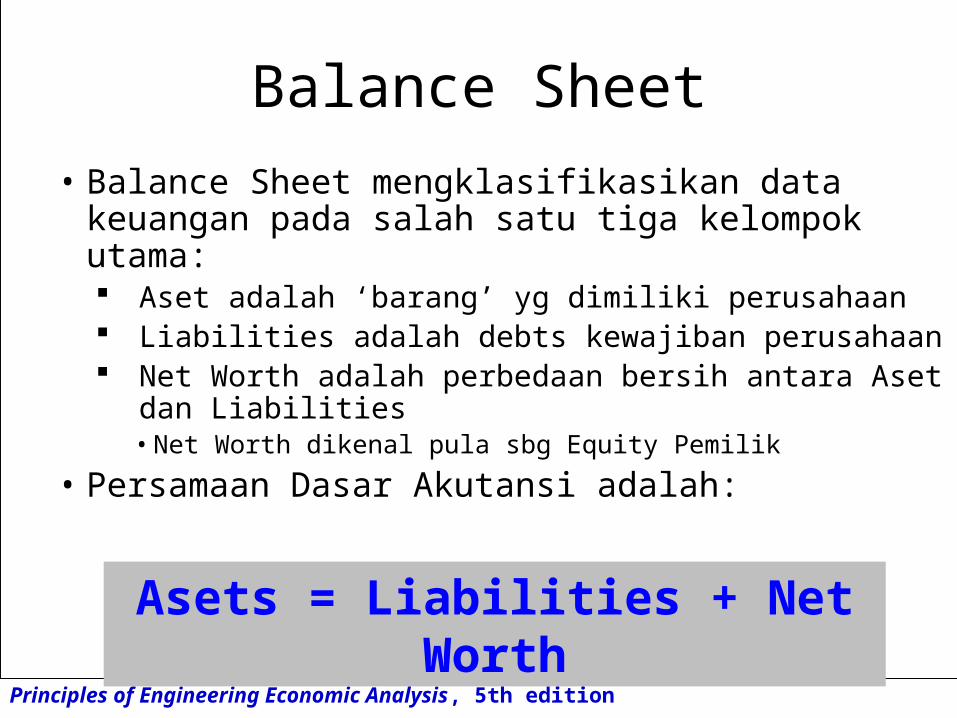

Balance Sheet

• Balance Sheet mengklasifikasikan data keuangan pada salah satu tiga kelompok utama: Aset adalah ‘barang’ yg dimiliki perusahaan Liabilities adalah debts kewajiban perusahaan Net Worth adalah perbedaan bersih antara Aset

dan Liabilities• Net Worth dikenal pula sbg Equity Pemilik

• Persamaan Dasar Akutansi adalah:

Asets = Liabilities + Net Worth

Principles of Engineering Economic Analysis, 5th edition

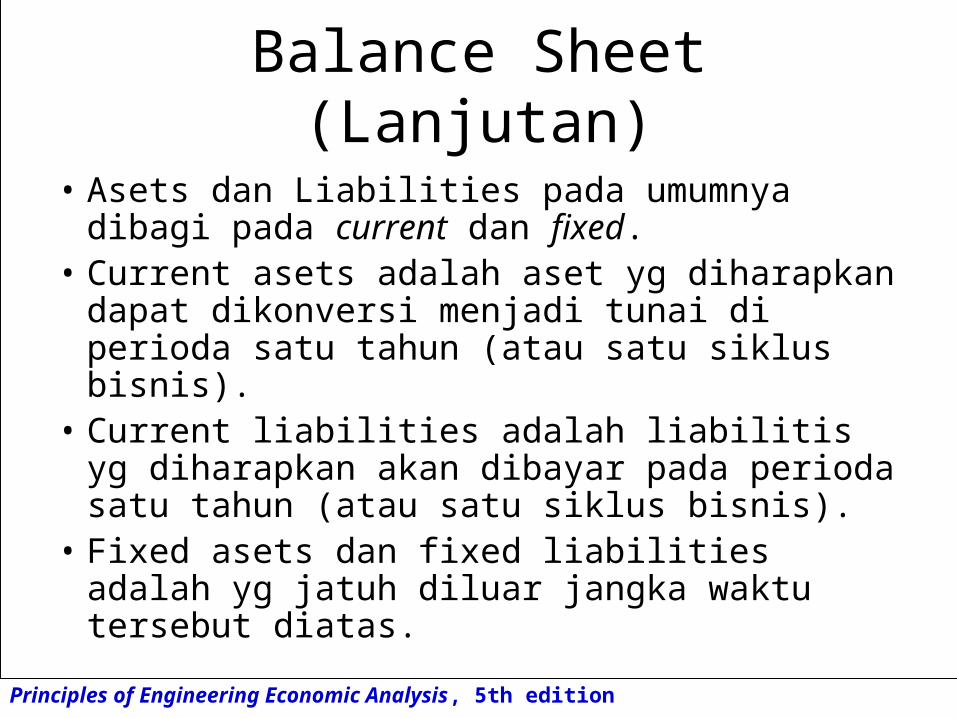

Balance Sheet(Lanjutan)

• Asets dan Liabilities pada umumnya dibagi pada current dan fixed.

• Current asets adalah aset yg diharapkan dapat dikonversi menjadi tunai di perioda satu tahun (atau satu siklus bisnis).

• Current liabilities adalah liabilitis yg diharapkan akan dibayar pada perioda satu tahun (atau satu siklus bisnis).

• Fixed asets dan fixed liabilities adalah yg jatuh diluar jangka waktu tersebut diatas.

Principles of Engineering Economic Analysis, 5th edition

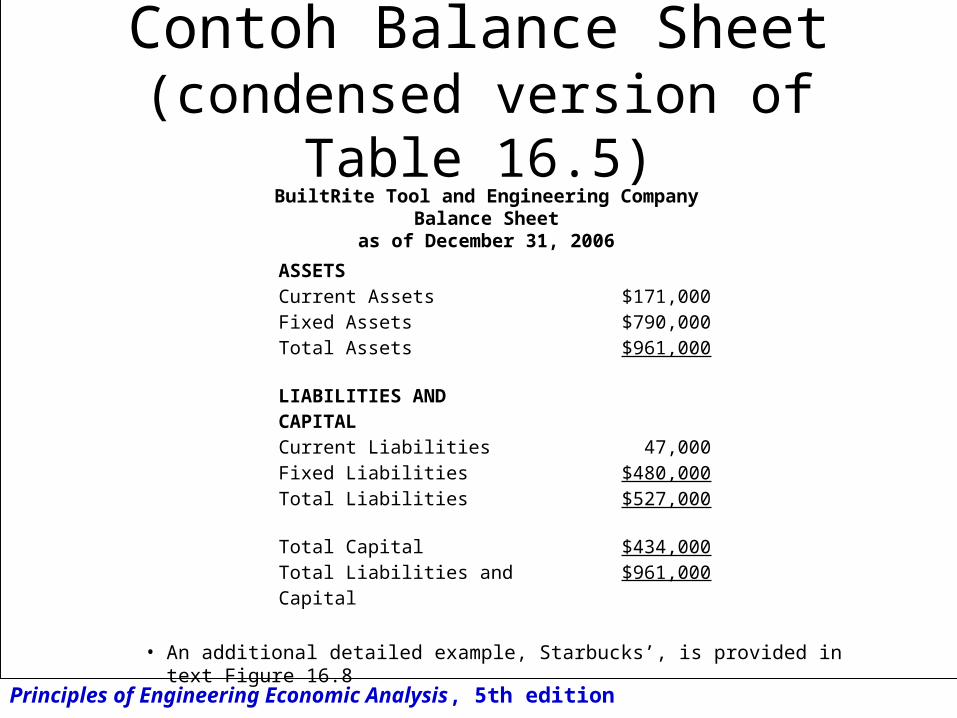

Contoh Balance Sheet(condensed version of Table 16.5)

• An additional detailed example, Starbucks’, is provided in text Figure 16.8

BuiltRite Tool and Engineering CompanyBalance Sheet

as of December 31, 2006

ASSETSCurrent Assets $171,000Fixed Assets $790,000Total Assets $961,000

LIABILITIES AND CAPITALCurrent Liabilities 47,000Fixed Liabilities $480,000Total Liabilities $527,000

Total Capital $434,000Total Liabilities and Capital $961,000

Principles of Engineering Economic Analysis, 5th edition

Income Statement

• Income Statement merupakan kumpulan dari (1) revenu yg diterima, (2) expenses yang terjadi, dan (3) profit atau loss hasil opeasi selama perioda akutansi.

• Income Statement seringkali disebut sebagai Profit and Loss Statement, P&L, atau Statement of Earnings.

• Net Profit (atau Net Loss) yang dikemukakan pada Income Statement disebut sebagai Net Income atau Net Earnings.

Principles of Engineering Economic Analysis, 5th edition

Income Statement(Lanjutan)

• Income Statement dimulai dengan Revenues.

• Selanjutnya, kurangi biaya langsung yg menghasilkan revenues. Biaya langsung ini dikenal sebagai Cost of Goods. Hasil pengurangannya dikenal sebagai Gross Income

atau Gross Profit.

• Kemudian, kurangi pengeluaran lainnya. Hasilnya adalah total “bottom line” dikenal sebagai

Net Income atau Net Profit.

Principles of Engineering Economic Analysis, 5th edition

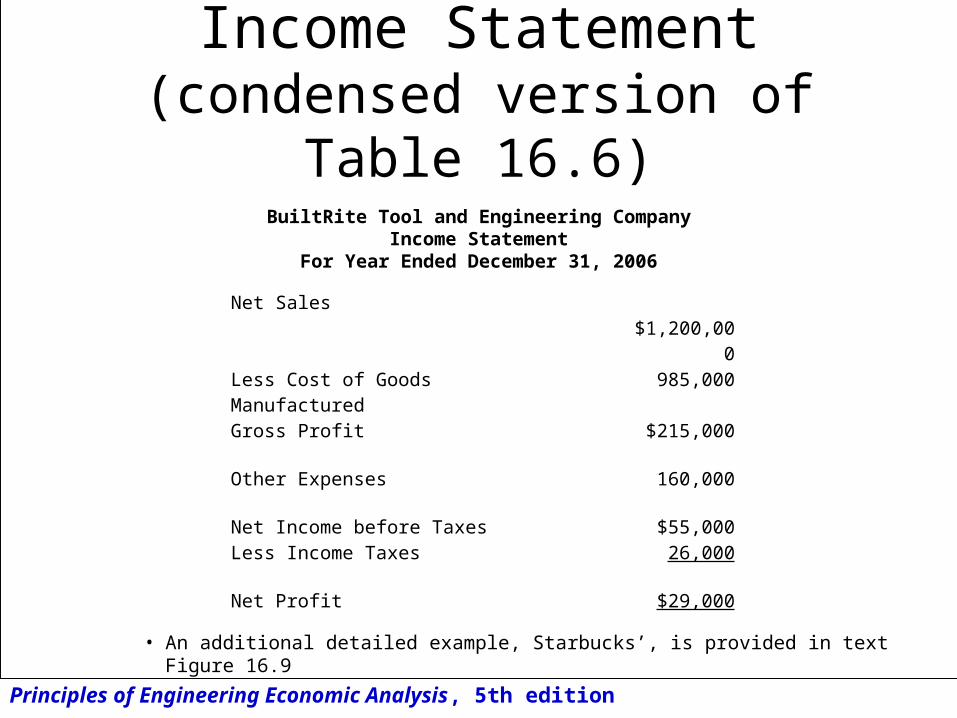

Income Statement(condensed version of Table 16.6)

• An additional detailed example, Starbucks’, is provided in text Figure 16.9

BuiltRite Tool and Engineering CompanyIncome Statement

For Year Ended December 31, 2006

Net Sales $1,200,000Less Cost of Goods Manufactured 985,000Gross Profit $215,000

Other Expenses 160,000

Net Income before Taxes $55,000Less Income Taxes 26,000

Net Profit $29,000

Principles of Engineering Economic Analysis, 5th edition

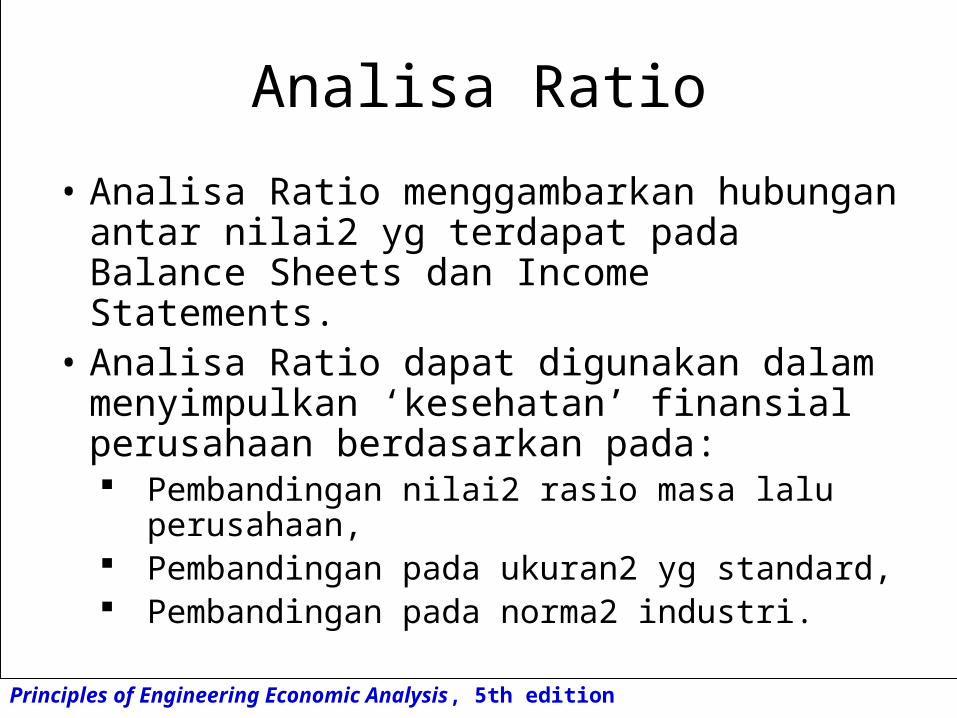

Analisa Ratio

• Analisa Ratio menggambarkan hubungan antar nilai2 yg terdapat pada Balance Sheets dan Income Statements.

• Analisa Ratio dapat digunakan dalam menyimpulkan ‘kesehatan’ finansial perusahaan berdasarkan pada: Pembandingan nilai2 rasio masa lalu

perusahaan, Pembandingan pada ukuran2 yg standard, Pembandingan pada norma2 industri.

Principles of Engineering Economic Analysis, 5th edition

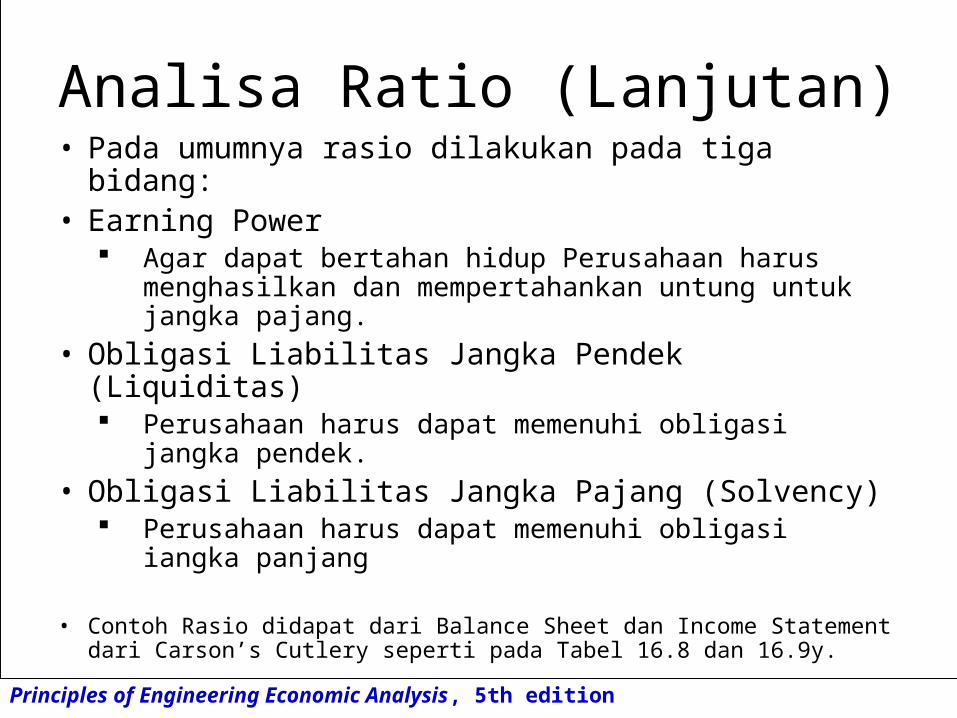

Analisa Ratio (Lanjutan)• Pada umumnya rasio dilakukan pada tiga bidang:• Earning Power

Agar dapat bertahan hidup Perusahaan harus menghasilkan dan mempertahankan untung untuk jangka pajang.

• Obligasi Liabilitas Jangka Pendek (Liquiditas) Perusahaan harus dapat memenuhi obligasi jangka

pendek.

• Obligasi Liabilitas Jangka Pajang (Solvency) Perusahaan harus dapat memenuhi obligasi iangka

panjang

• Contoh Rasio didapat dari Balance Sheet dan Income Statement dari Carson’s Cutlery seperti pada Tabel 16.8 dan 16.9y.

Principles of Engineering Economic Analysis, 5th edition

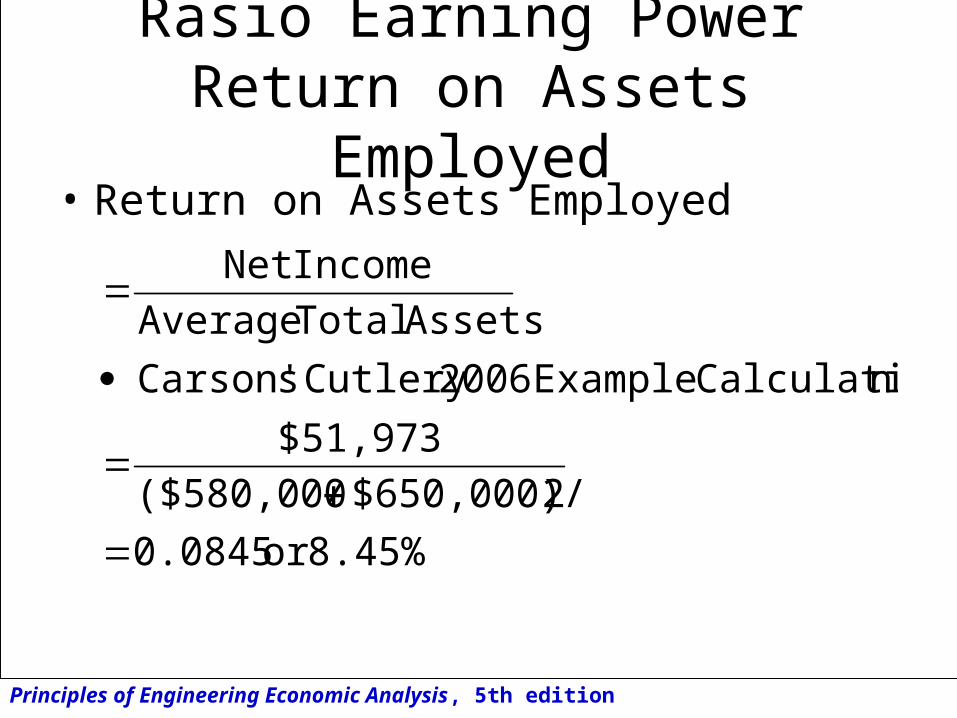

Rasio Earning PowerReturn on Assets Employed

• Return on Assets Employed

8.45% or 0.0845

2$650,000)/($580,000

$51,973

nCalculatio Example 2006Cutlery sCarson'

AssetsTotal Average

Income Net

Principles of Engineering Economic Analysis, 5th edition

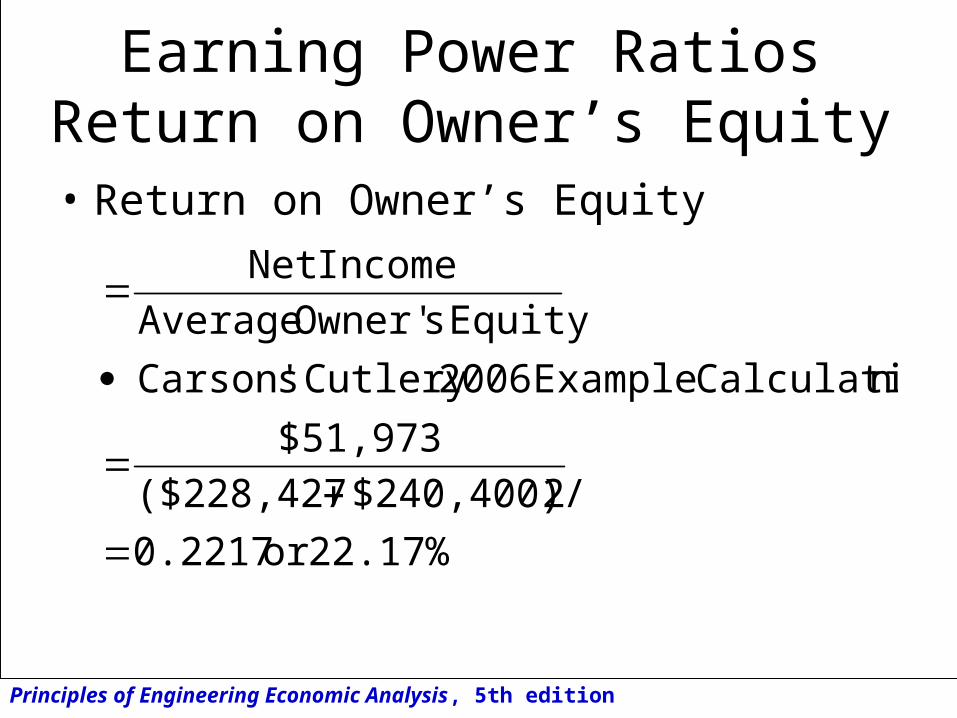

Earning Power RatiosReturn on Owner’s Equity

• Return on Owner’s Equity

22.17% or 0.2217

2$240,400)/($228,427

$51,973

nCalculatio Example 2006Cutlery sCarson'

Equity sOwner' Average

Income Net

Principles of Engineering Economic Analysis, 5th edition

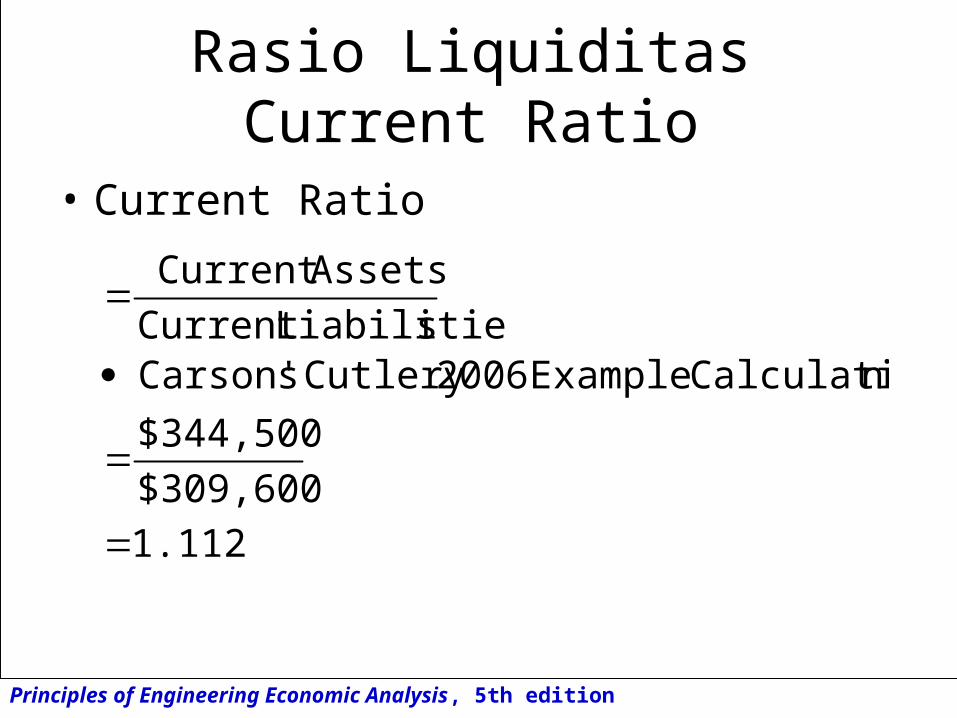

Rasio LiquiditasCurrent Ratio

• Current Ratio

1.112

$309,600

$344,500

nCalculatio Example 2006Cutlery sCarson' sLiabilitie Current

AssetsCurrent

Principles of Engineering Economic Analysis, 5th edition

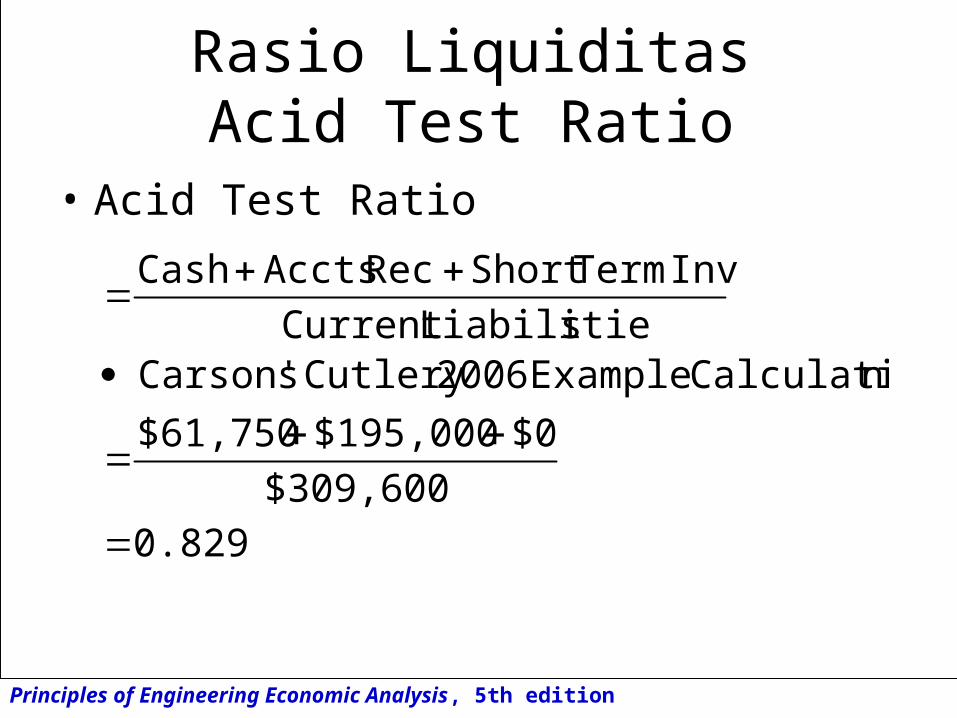

Rasio LiquiditasAcid Test Ratio

• Acid Test Ratio

0.829

$309,600

$0$195,000$61,750

nCalculatio Example 2006Cutlery sCarson' sLiabilitie Current

Inv Term ShortRec AcctsCash

Principles of Engineering Economic Analysis, 5th edition

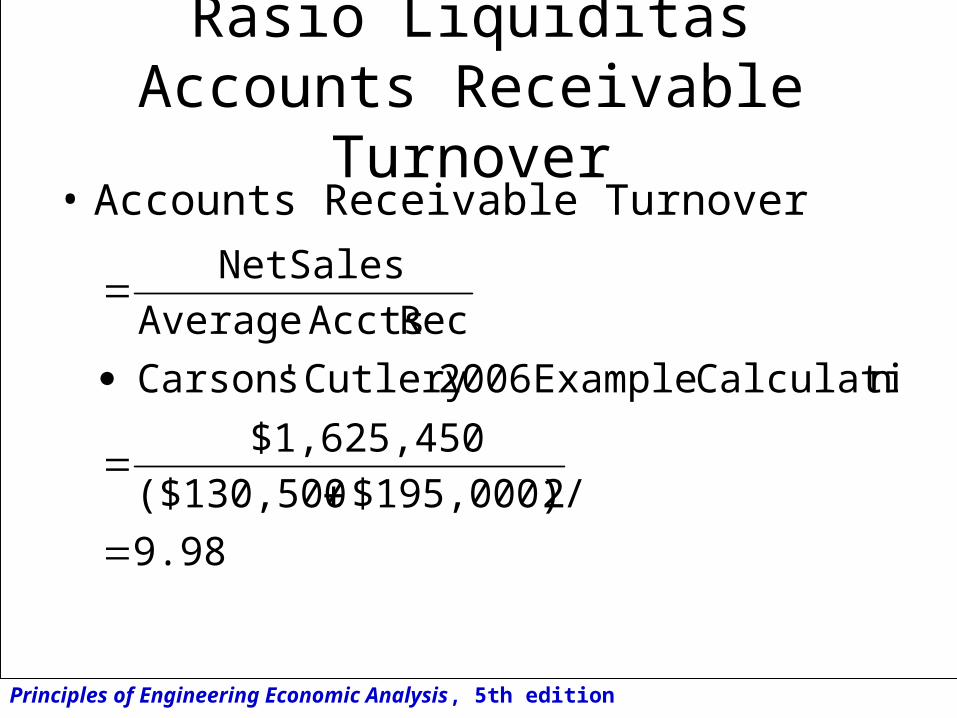

Rasio LiquiditasAccounts Receivable Turnover

• Accounts Receivable Turnover

9.98

2$195,000)/($130,500

$1,625,450

nCalculatio Example 2006Cutlery sCarson'

Rec AcctsAverage

Sales Net

Principles of Engineering Economic Analysis, 5th edition

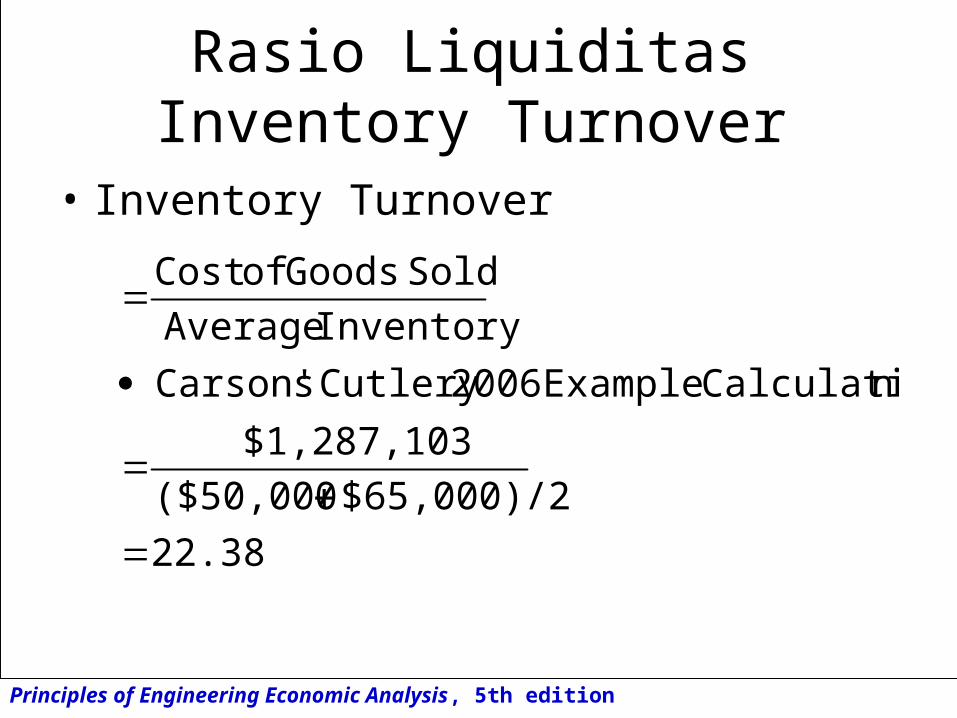

Rasio LiquiditasInventory Turnover

• Inventory Turnover

22.38

$65,000)/2($50,000

$1,287,103

nCalculatio Example 2006Cutlery sCarson'

Inventory Average

Sold Goods of Cost

Principles of Engineering Economic Analysis, 5th edition

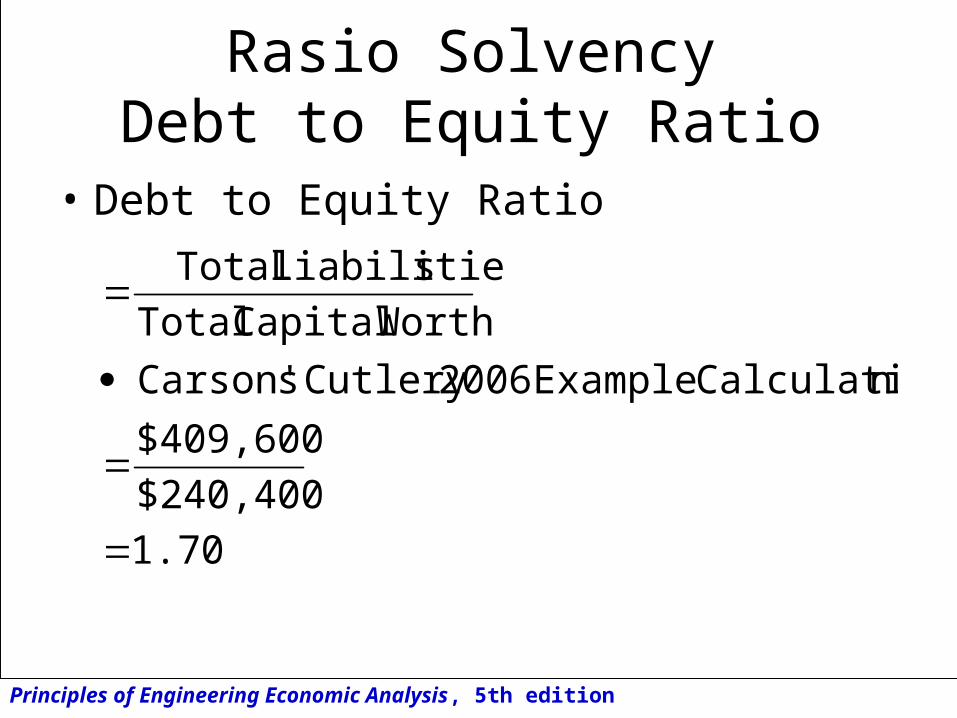

Rasio SolvencyDebt to Equity Ratio

• Debt to Equity Ratio

1.70

$240,400

$409,600

nCalculatio Example 2006Cutlery sCarson'

WorthCapital Total

sLiabilitie Total

Principles of Engineering Economic Analysis, 5th edition

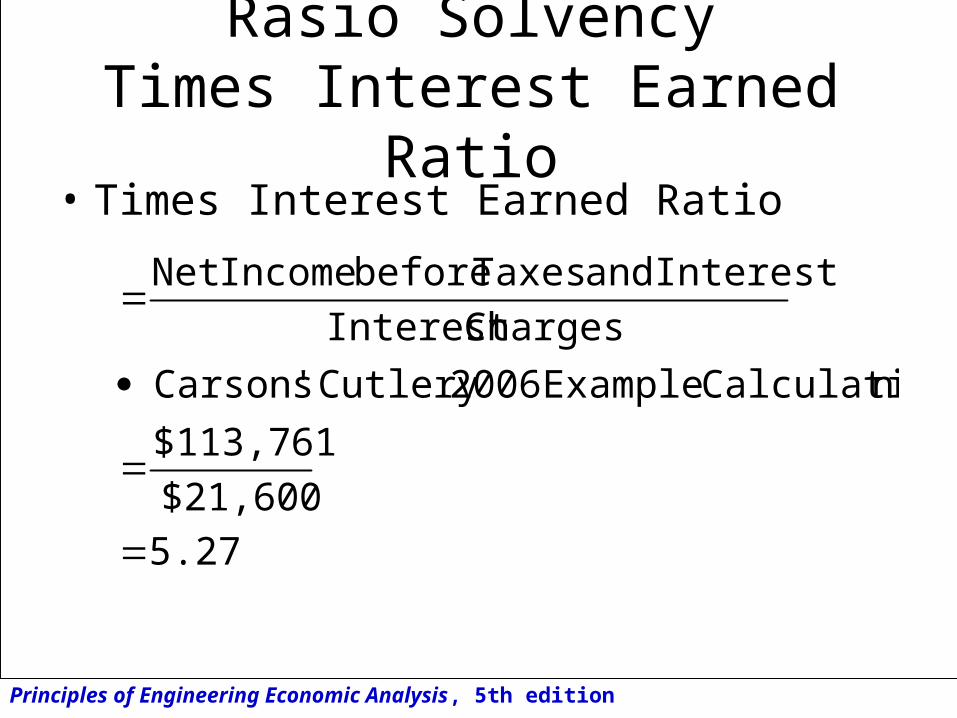

Rasio SolvencyTimes Interest Earned Ratio

• Times Interest Earned Ratio

5.27

$21,600

$113,761

nCalculatio Example 2006Cutlery sCarson'

Charges Interest

Interest and Taxes before Income Net

Principles of Engineering Economic Analysis, 5th edition

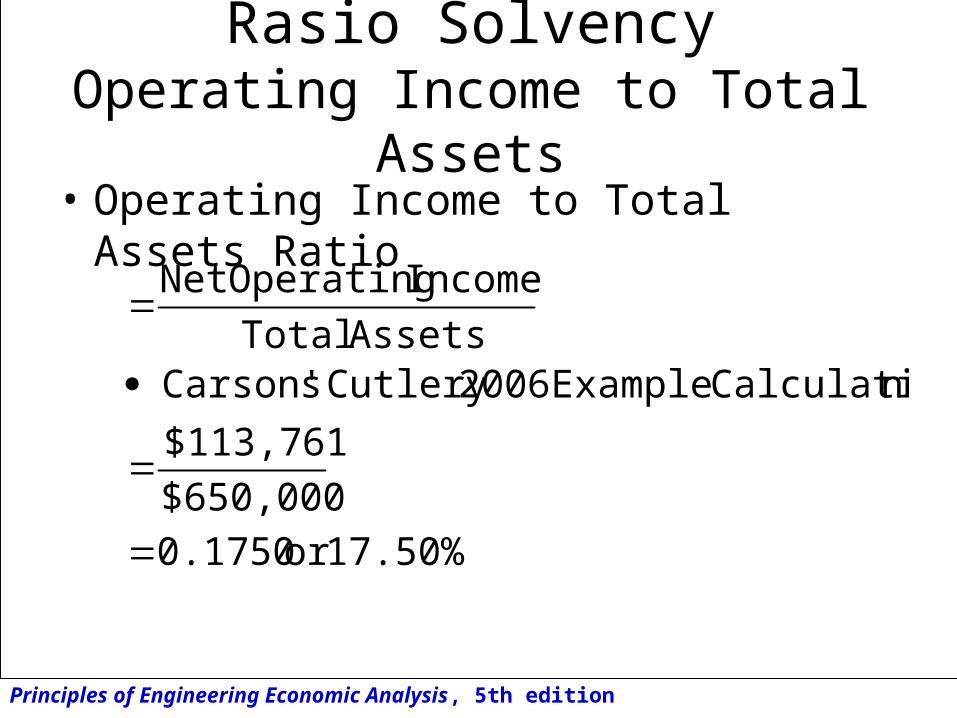

Rasio SolvencyOperating Income to Total Assets

• Operating Income to Total Assets Ratio

17.50% or 0.1750

$650,000

$113,761

nCalculatio Example 2006Cutlery sCarson' AssetsTotal

Income Operating Net

Principles of Engineering Economic Analysis, 5th edition

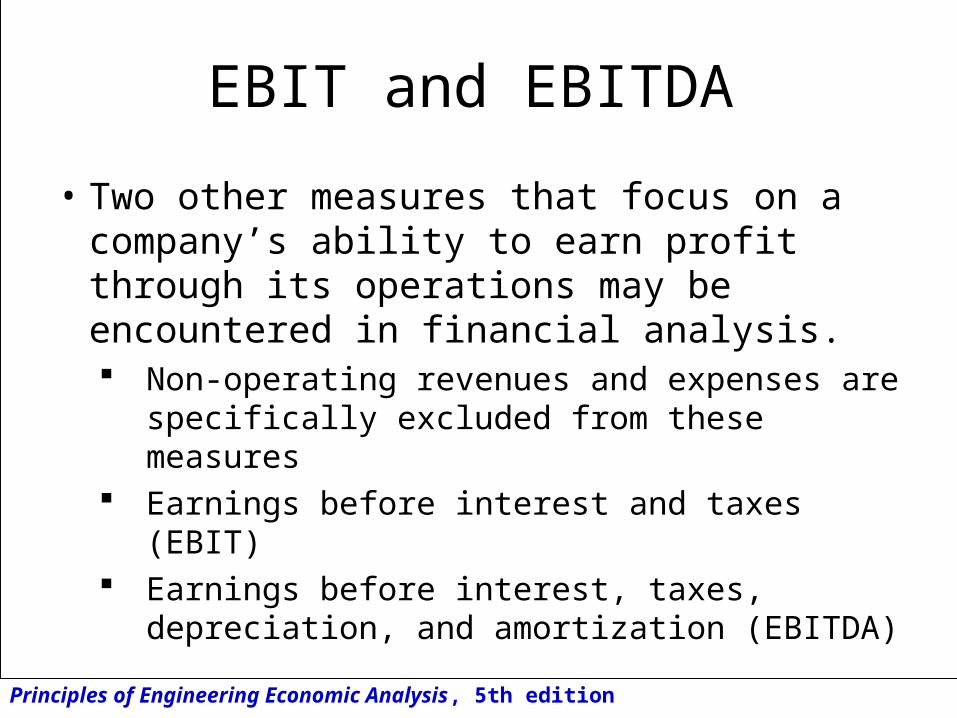

EBIT and EBITDA

• Two other measures that focus on a company’s ability to earn profit through its operations may be encountered in financial analysis. Non-operating revenues and expenses are

specifically excluded from these measures Earnings before interest and taxes (EBIT) Earnings before interest, taxes, depreciation,

and amortization (EBITDA)

Principles of Engineering Economic Analysis, 5th edition

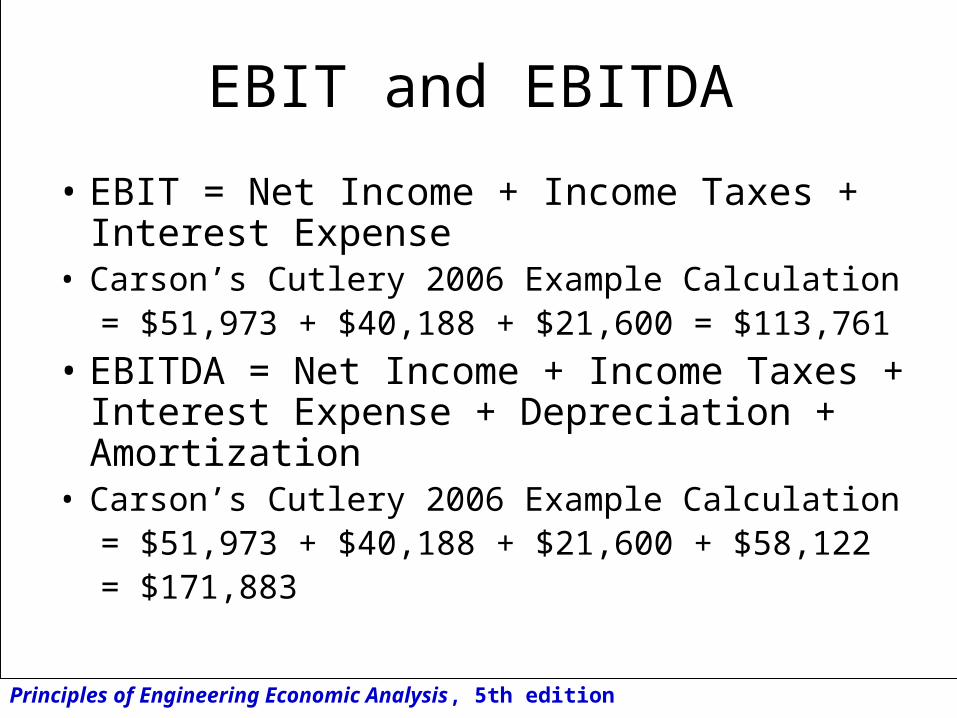

EBIT and EBITDA

• EBIT = Net Income + Income Taxes + Interest Expense

• Carson’s Cutlery 2006 Example Calculation= $51,973 + $40,188 + $21,600 = $113,761

• EBITDA = Net Income + Income Taxes + Interest Expense + Depreciation + Amortization

• Carson’s Cutlery 2006 Example Calculation= $51,973 + $40,188 + $21,600 + $58,122= $171,883

Principles of Engineering Economic Analysis, 5th edition

Prinsip Cost Accounting(16.5)

• Cost Accounting fokus pada pencarian (atau prediksi) biaya dalam memproduksi suatu produk atau pekerjaan.

• Material dan Buruh Langsung adalah bagian dari produk/pekerjaan yang biasanya tersedia. Material Langsung biasanya didapat dari

purchase order dan/atau bills of material. Buruh Langsung biasanya didapat dari sistim

pelaporan tenaga kerja dan/atau dokumentasi perencanaan proses.

Principles of Engineering Economic Analysis, 5th edition

Alokasi Overhead

• Pengeluaran Overhead pada umumnya tidak didapatkan secara langsung dan dibebankan pada produk/pekerjaan.

• Pembebanan overhead total biasanya diakumulasikan selama perioda waktu tertentu dan kemuadian dialokasikan pada produk/pekerjaan selam perioda waktu tersebut.

Principles of Engineering Economic Analysis, 5th edition

Metoda Traditional dalam Alokasi Overhead

• Traditional methods typically allocate overhead one of three ways:

• Allocation based on direct labor hours Direct labor hours is the simplest and most

common method.• Allocation based on direct labor dollars

Direct labor dollars is useful if labor rates vary across different classes of labor used on different products/jobs.

• Allocation based on prime dollars Prime dollars is useful if the cost of material is

significantly different across products/jobs.

Principles of Engineering Economic Analysis, 5th edition

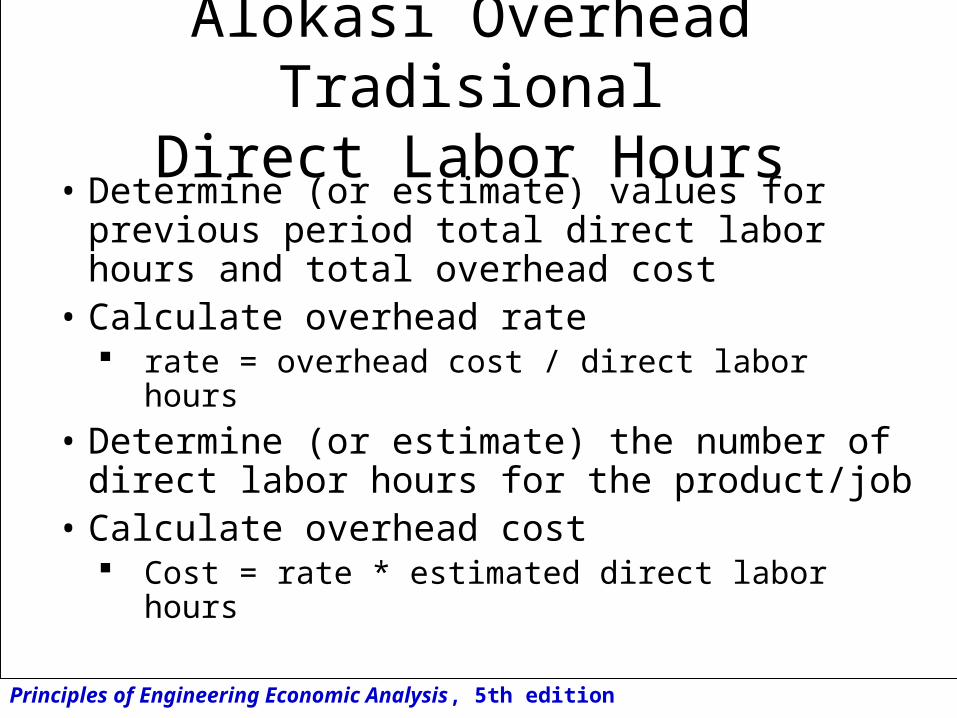

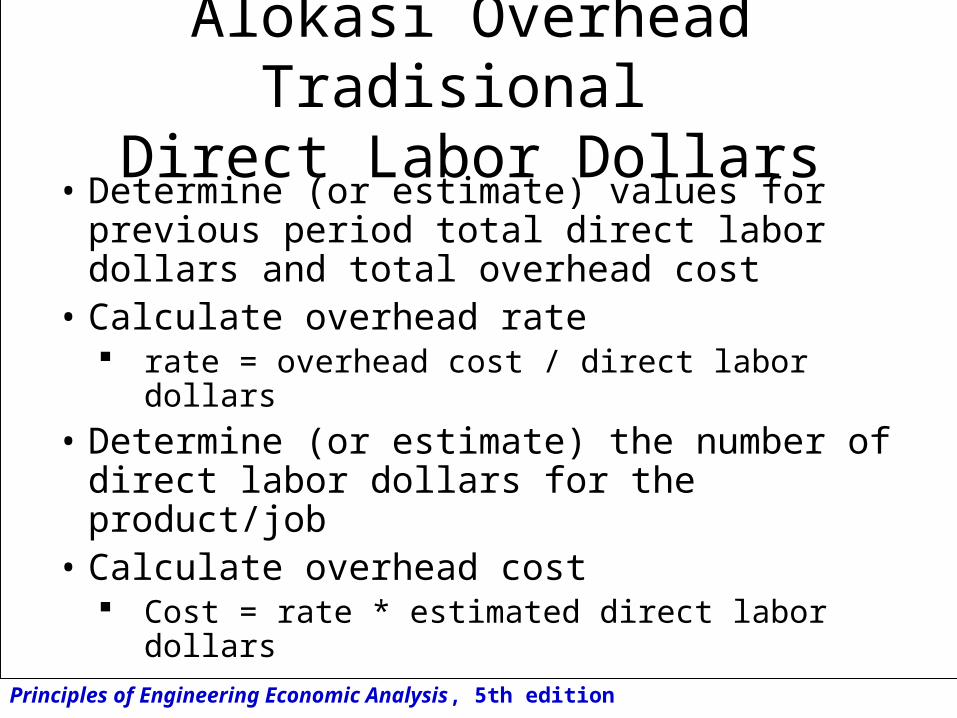

Alokasi Overhead TradisionalDirect Labor Hours

• Determine (or estimate) values for previous period total direct labor hours and total overhead cost

• Calculate overhead rate rate = overhead cost / direct labor hours

• Determine (or estimate) the number of direct labor hours for the product/job

• Calculate overhead cost Cost = rate * estimated direct labor hours

Principles of Engineering Economic Analysis, 5th edition

Alokasi Overhead Tradisional Direct Labor Dollars

• Determine (or estimate) values for previous period total direct labor dollars and total overhead cost

• Calculate overhead rate rate = overhead cost / direct labor dollars

• Determine (or estimate) the number of direct labor dollars for the product/job

• Calculate overhead cost Cost = rate * estimated direct labor dollars

Principles of Engineering Economic Analysis, 5th edition

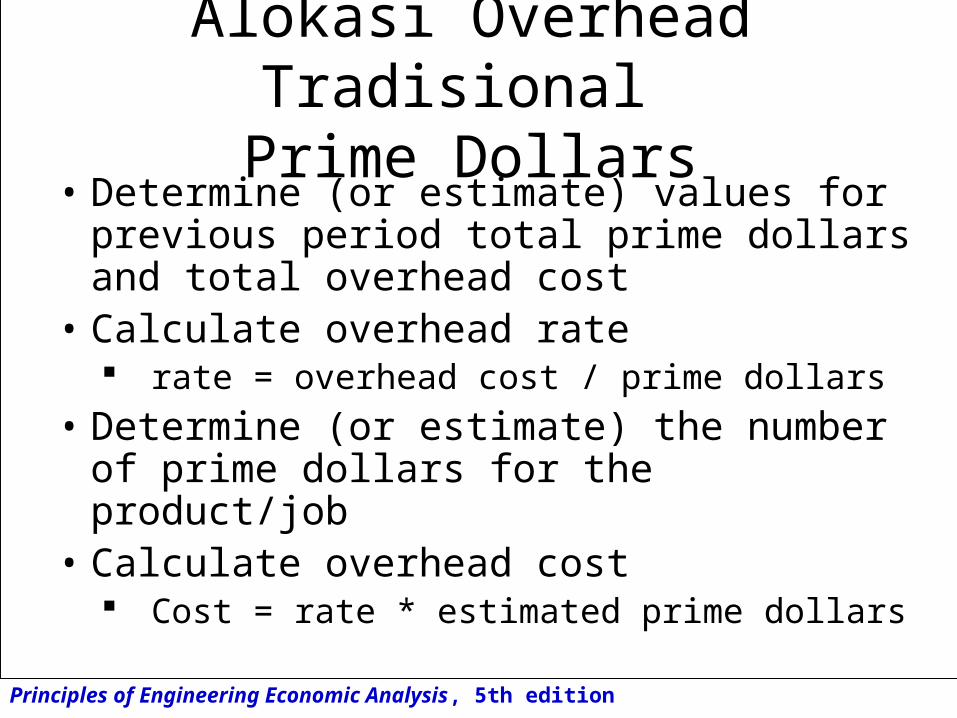

Alokasi Overhead Tradisional Prime Dollars

• Determine (or estimate) values for previous period total prime dollars and total overhead cost

• Calculate overhead rate rate = overhead cost / prime dollars

• Determine (or estimate) the number of prime dollars for the product/job

• Calculate overhead cost Cost = rate * estimated prime dollars

Principles of Engineering Economic Analysis, 5th edition

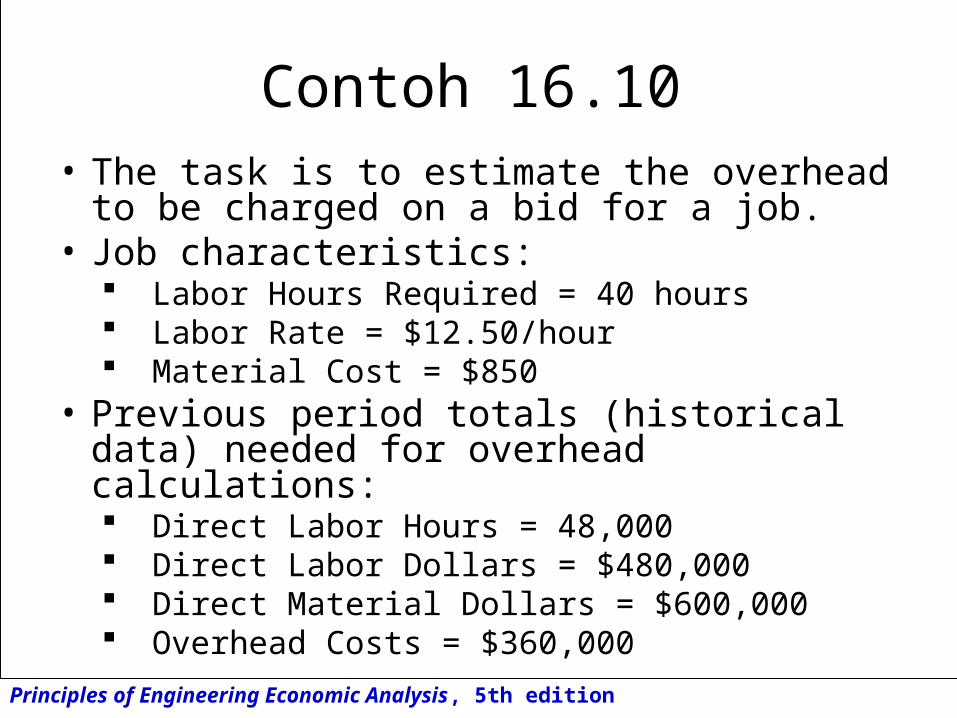

Contoh 16.10• The task is to estimate the overhead to be

charged on a bid for a job.• Job characteristics:

Labor Hours Required = 40 hours Labor Rate = $12.50/hour Material Cost = $850

• Previous period totals (historical data) needed for overhead calculations: Direct Labor Hours = 48,000 Direct Labor Dollars = $480,000 Direct Material Dollars = $600,000 Overhead Costs = $360,000

Principles of Engineering Economic Analysis, 5th edition

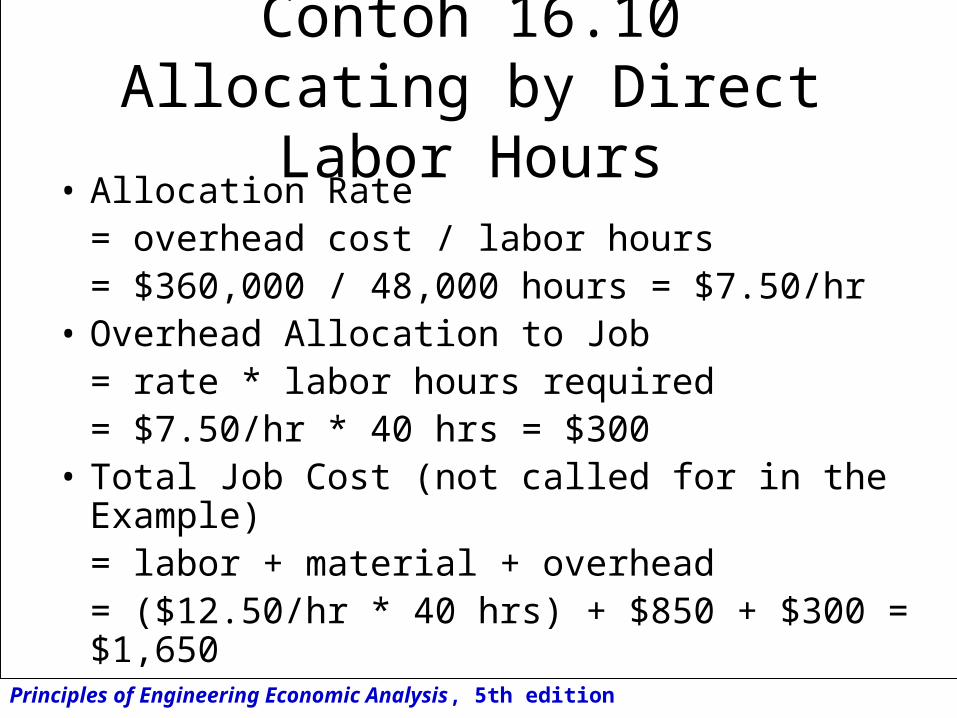

Contoh 16.10Allocating by Direct Labor Hours• Allocation Rate

= overhead cost / labor hours= $360,000 / 48,000 hours = $7.50/hr

• Overhead Allocation to Job= rate * labor hours required= $7.50/hr * 40 hrs = $300

• Total Job Cost (not called for in the Example)= labor + material + overhead= ($12.50/hr * 40 hrs) + $850 + $300 = $1,650

Principles of Engineering Economic Analysis, 5th edition

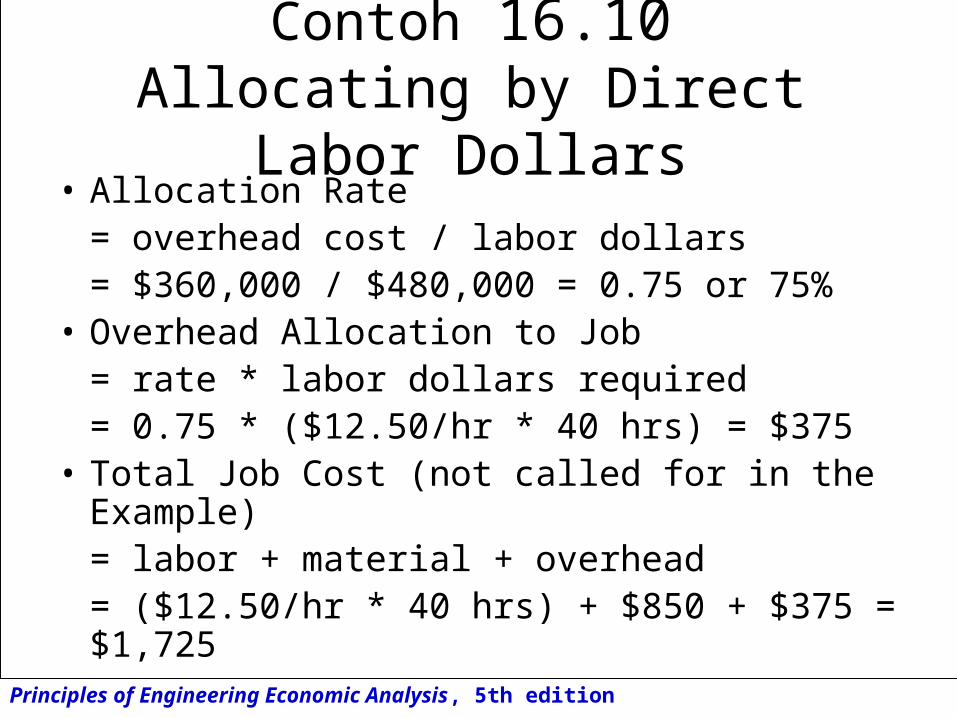

Contoh 16.10Allocating by Direct Labor Dollars• Allocation Rate

= overhead cost / labor dollars= $360,000 / $480,000 = 0.75 or 75%

• Overhead Allocation to Job= rate * labor dollars required= 0.75 * ($12.50/hr * 40 hrs) = $375

• Total Job Cost (not called for in the Example)= labor + material + overhead= ($12.50/hr * 40 hrs) + $850 + $375 = $1,725

Principles of Engineering Economic Analysis, 5th edition

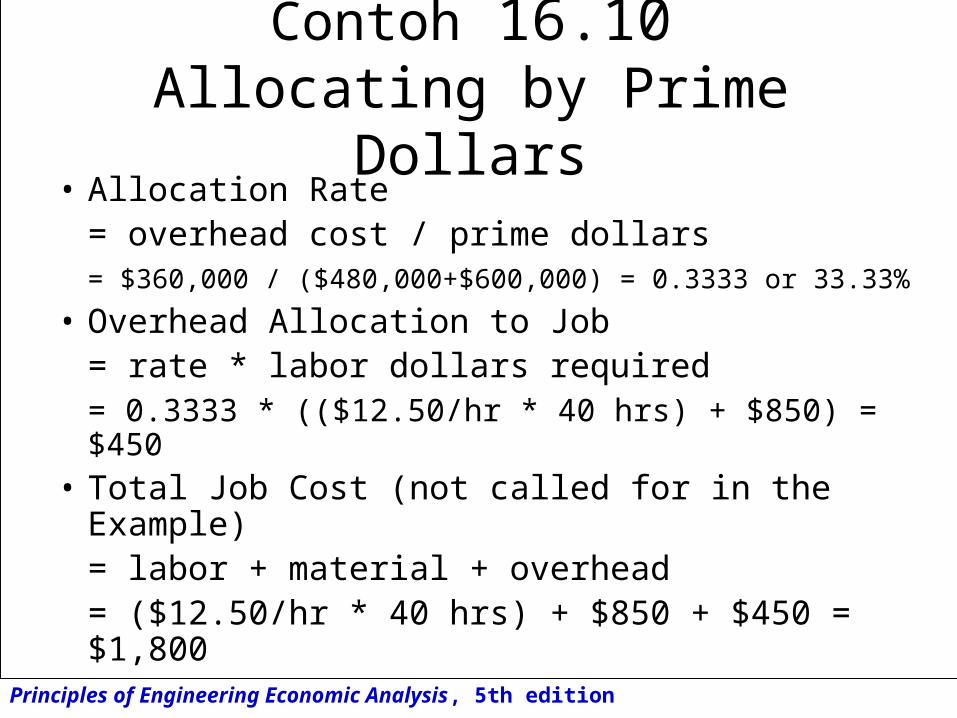

Contoh 16.10Allocating by Prime Dollars

• Allocation Rate= overhead cost / prime dollars= $360,000 / ($480,000+$600,000) = 0.3333 or 33.33%

• Overhead Allocation to Job= rate * labor dollars required= 0.3333 * (($12.50/hr * 40 hrs) + $850) = $450

• Total Job Cost (not called for in the Example)= labor + material + overhead= ($12.50/hr * 40 hrs) + $850 + $450 = $1,800

Principles of Engineering Economic Analysis, 5th edition

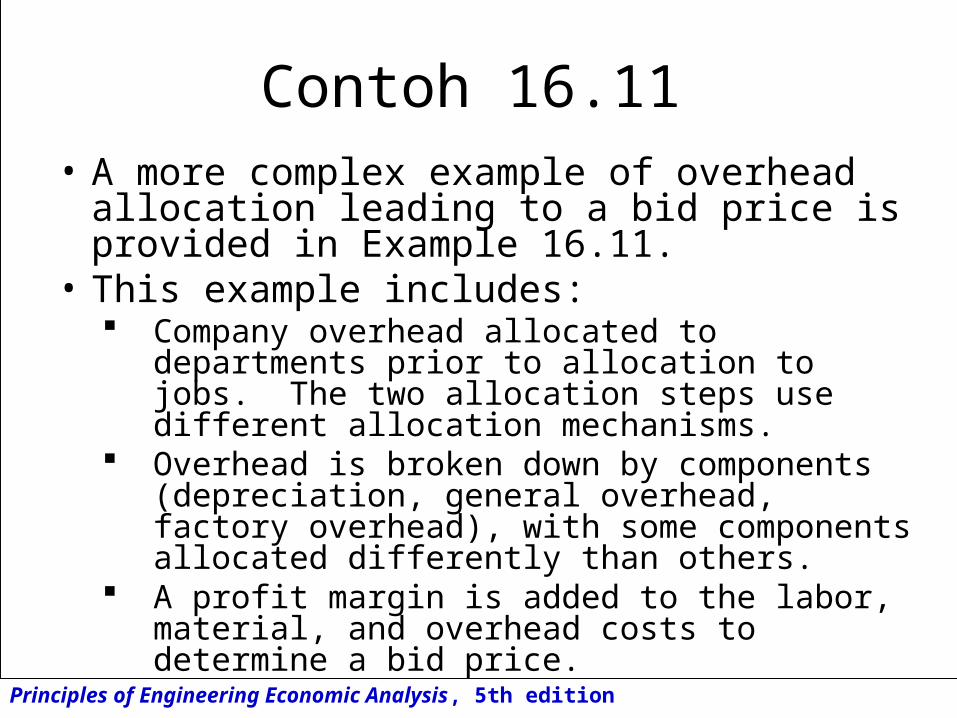

Contoh 16.11• A more complex example of overhead

allocation leading to a bid price is provided in Example 16.11.

• This example includes: Company overhead allocated to departments

prior to allocation to jobs. The two allocation steps use different allocation mechanisms.

Overhead is broken down by components (depreciation, general overhead, factory overhead), with some components allocated differently than others.

A profit margin is added to the labor, material, and overhead costs to determine a bid price.

Principles of Engineering Economic Analysis, 5th edition

Pembebanan Biaya berdasarkan Activitas

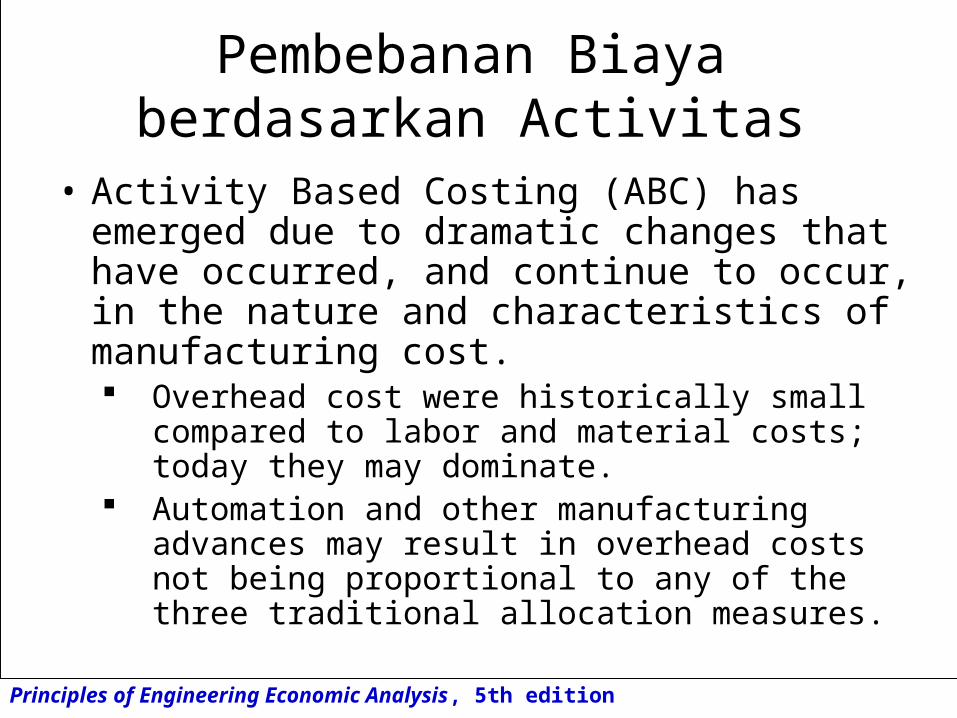

• Activity Based Costing (ABC) has emerged due to dramatic changes that have occurred, and continue to occur, in the nature and characteristics of manufacturing cost. Overhead cost were historically small compared

to labor and material costs; today they may dominate.

Automation and other manufacturing advances may result in overhead costs not being proportional to any of the three traditional allocation measures.

Principles of Engineering Economic Analysis, 5th edition

Pembebanan Biaya berdasarkan Activitas

• Activity Based Costing seeks to associate overhead costs (as well as labor and material costs) with the activities that generate them.

• Costs and cost rates are identified with the specific activities that drive them rather than with one of the traditional measures.

• Costs are then allocated to products/jobs based on the activities required to produce them.

Principles of Engineering Economic Analysis, 5th edition

Pembebanan Biaya berdasarkan Activitas

• Many companies find that ABC driven costing provides a much more accurate picture of true costs than traditional methods.

• Frequently, insights generated from ABC have lead to impressive process improvements and cost reductions by eliminating activities that add cost but not

value, by focusing improvement efforts on activities that

add value.

Principles of Engineering Economic Analysis, 5th edition

Standard Costs

• Another major purpose of cost accounting is to measure production efficiency and to help evaluate production performance.

• Establishing cost standards can facilitate these goals.

• Cost standards involve: Determination of standard rates (expected rates)

for material, labor, overhead. Application of the standard rates to the consumed

quantities of labor and material.• Variance from thee standards provides a

measure of performance.

Principles of Engineering Economic Analysis, 5th edition

Standard Costs(continued)

• Variation from cost standards can be caused by price variance, use variance, or both.

• Use Variance Quantities in excess of (or less than) plan are

consumed

• Price Variance Rates in excess of (or less than) standards are

experienced

• Understanding the source of cost variation can lead directly to eliminating it (or cementing it).

Principles of Engineering Economic Analysis, 5th edition

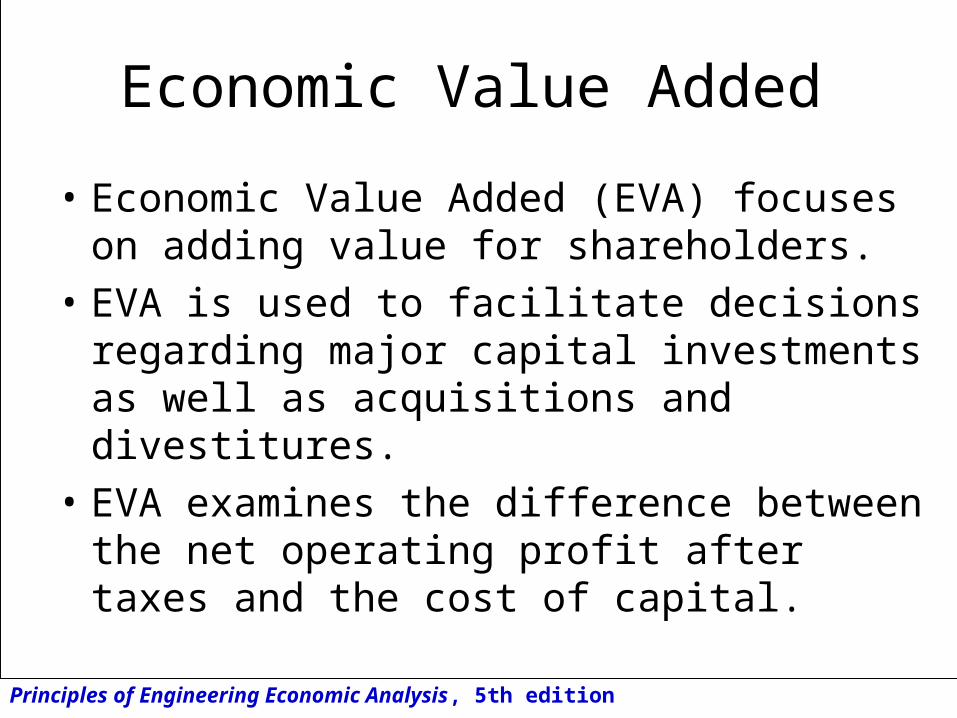

Economic Value Added

• Economic Value Added (EVA) focuses on adding value for shareholders.

• EVA is used to facilitate decisions regarding major capital investments as well as acquisitions and divestitures.

• EVA examines the difference between the net operating profit after taxes and the cost of capital.

Principles of Engineering Economic Analysis, 5th edition

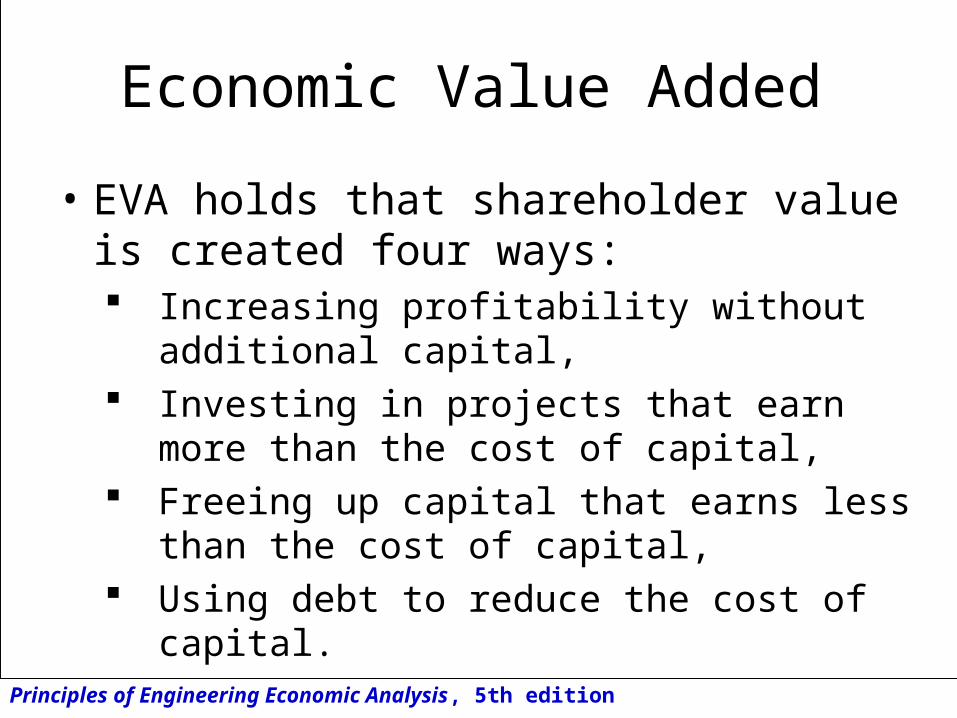

Economic Value Added

• EVA holds that shareholder value is created four ways: Increasing profitability without additional

capital, Investing in projects that earn more than the

cost of capital, Freeing up capital that earns less than the

cost of capital, Using debt to reduce the cost of capital.

Principles of Engineering Economic Analysis, 5th edition

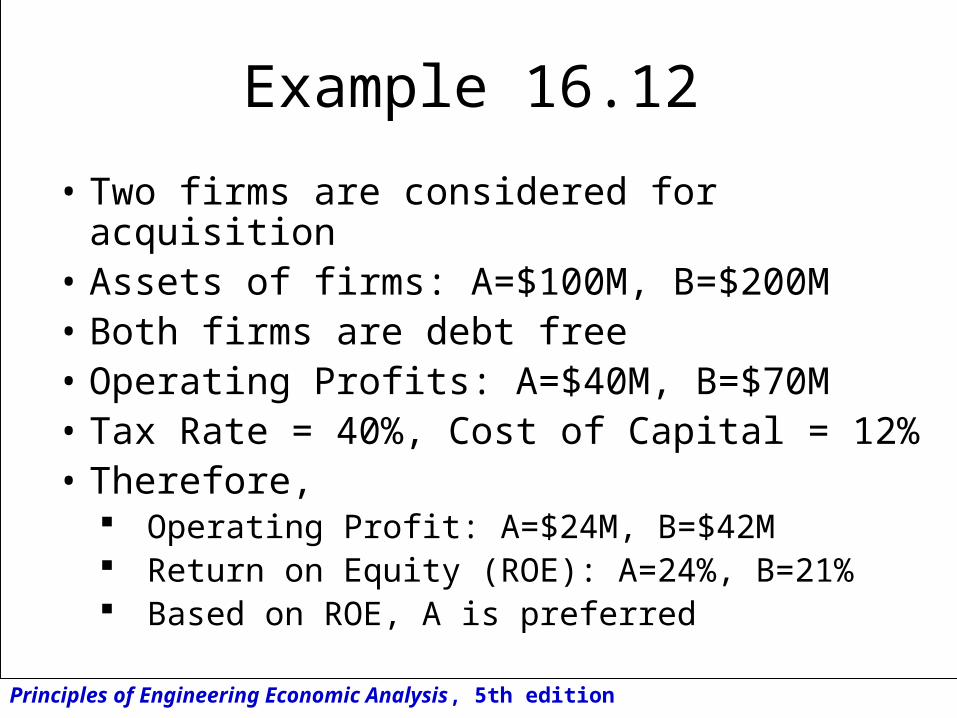

Example 16.12

• Two firms are considered for acquisition• Assets of firms: A=$100M, B=$200M• Both firms are debt free• Operating Profits: A=$40M, B=$70M• Tax Rate = 40%, Cost of Capital = 12%• Therefore,

Operating Profit: A=$24M, B=$42M Return on Equity (ROE): A=24%, B=21% Based on ROE, A is preferred

Principles of Engineering Economic Analysis, 5th edition

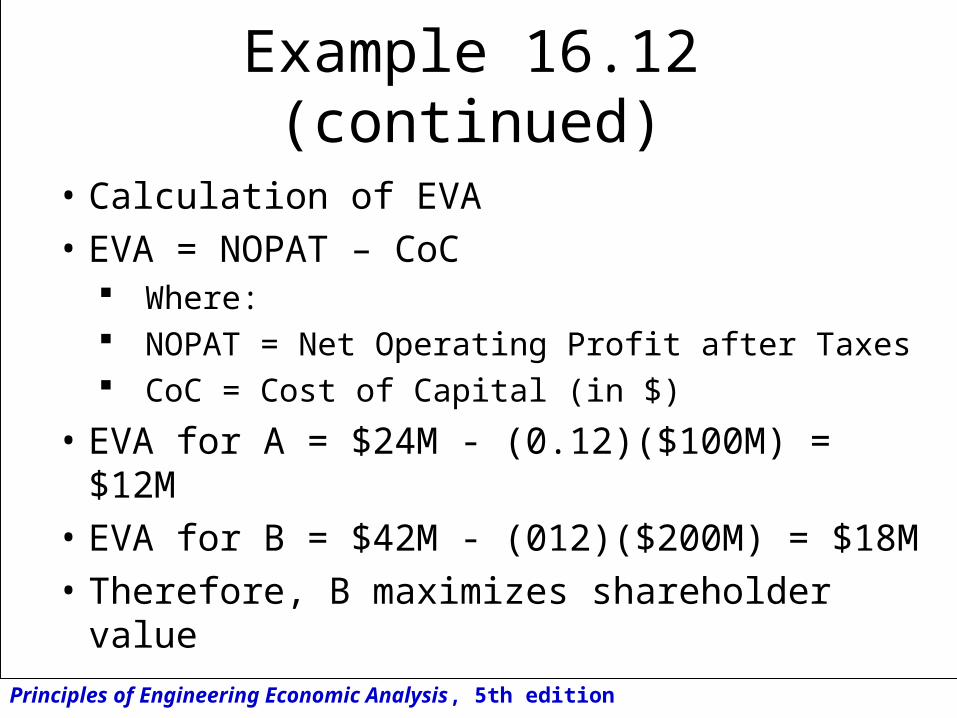

Example 16.12(continued)

• Calculation of EVA

• EVA = NOPAT – CoC Where: NOPAT = Net Operating Profit after Taxes CoC = Cost of Capital (in $)

• EVA for A = $24M - (0.12)($100M) = $12M

• EVA for B = $42M - (012)($200M) = $18M

• Therefore, B maximizes shareholder value

Principles of Engineering Economic Analysis, 5th edition

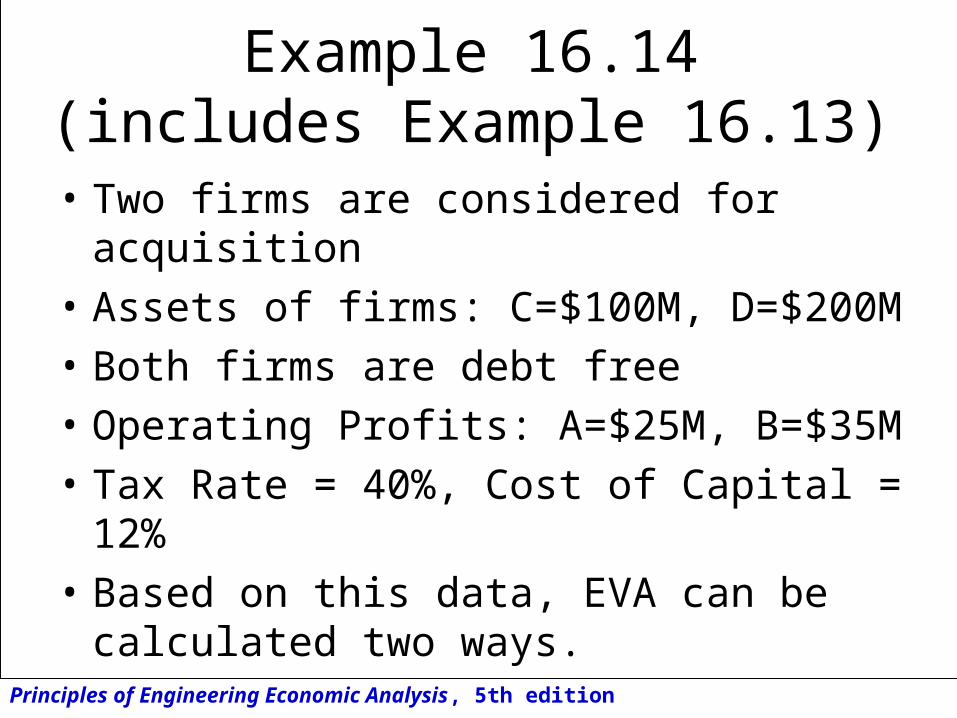

Example 16.14(includes Example 16.13)

• Two firms are considered for acquisition

• Assets of firms: C=$100M, D=$200M

• Both firms are debt free

• Operating Profits: A=$25M, B=$35M

• Tax Rate = 40%, Cost of Capital = 12%

• Based on this data, EVA can be calculated two ways.

Principles of Engineering Economic Analysis, 5th edition

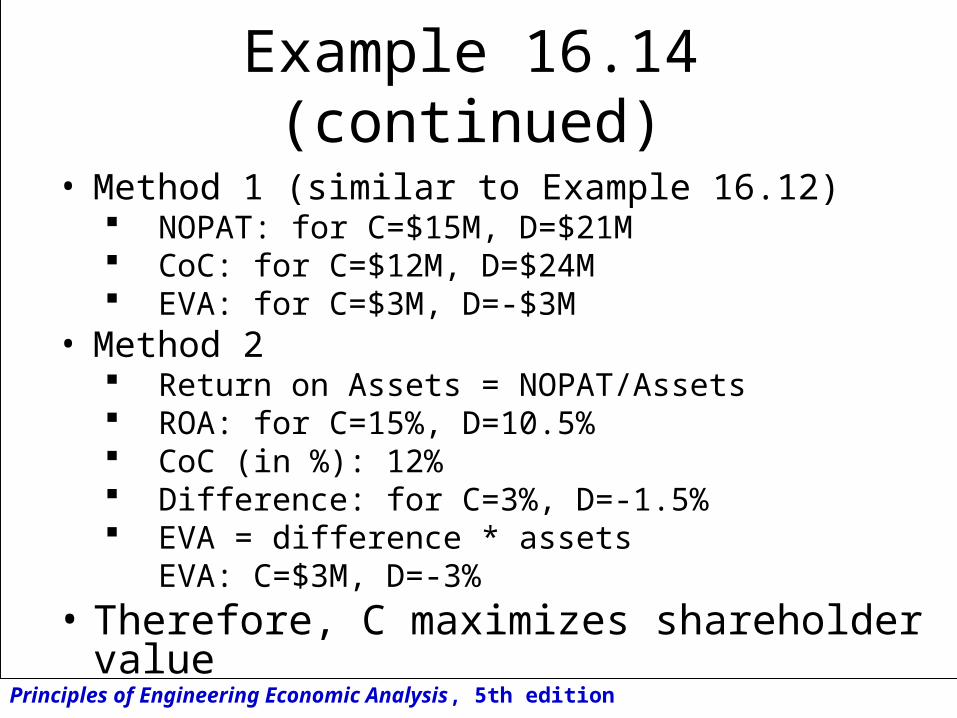

Example 16.14(continued)

• Method 1 (similar to Example 16.12) NOPAT: for C=$15M, D=$21M CoC: for C=$12M, D=$24M EVA: for C=$3M, D=-$3M

• Method 2 Return on Assets = NOPAT/Assets ROA: for C=15%, D=10.5% CoC (in %): 12% Difference: for C=3%, D=-1.5% EVA = difference * assets

EVA: C=$3M, D=-3%

• Therefore, C maximizes shareholder value

Principles of Engineering Economic Analysis, 5th edition

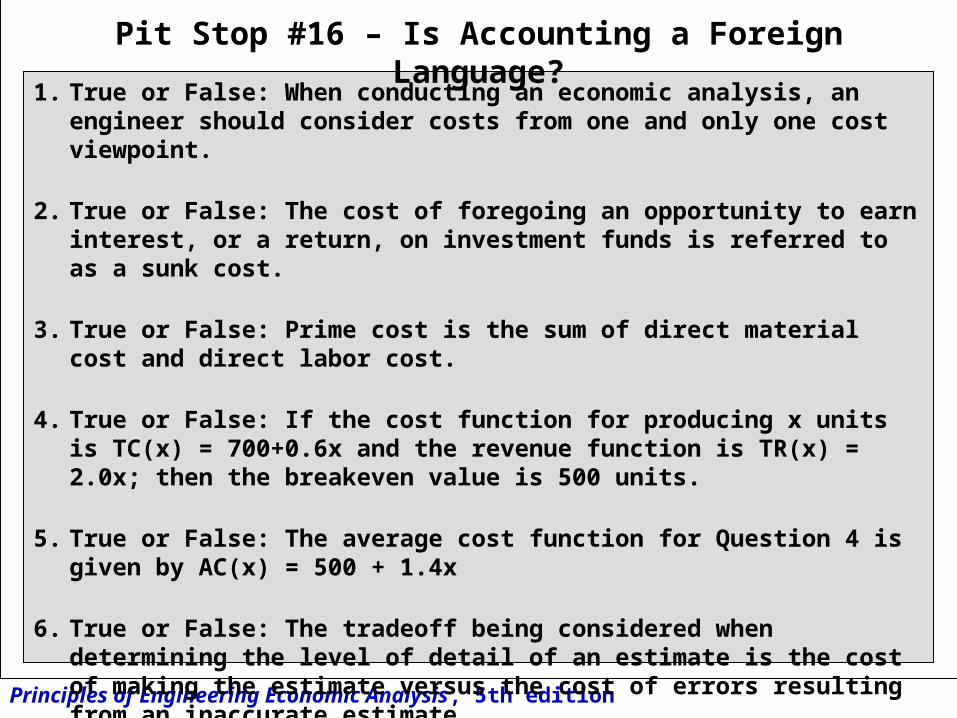

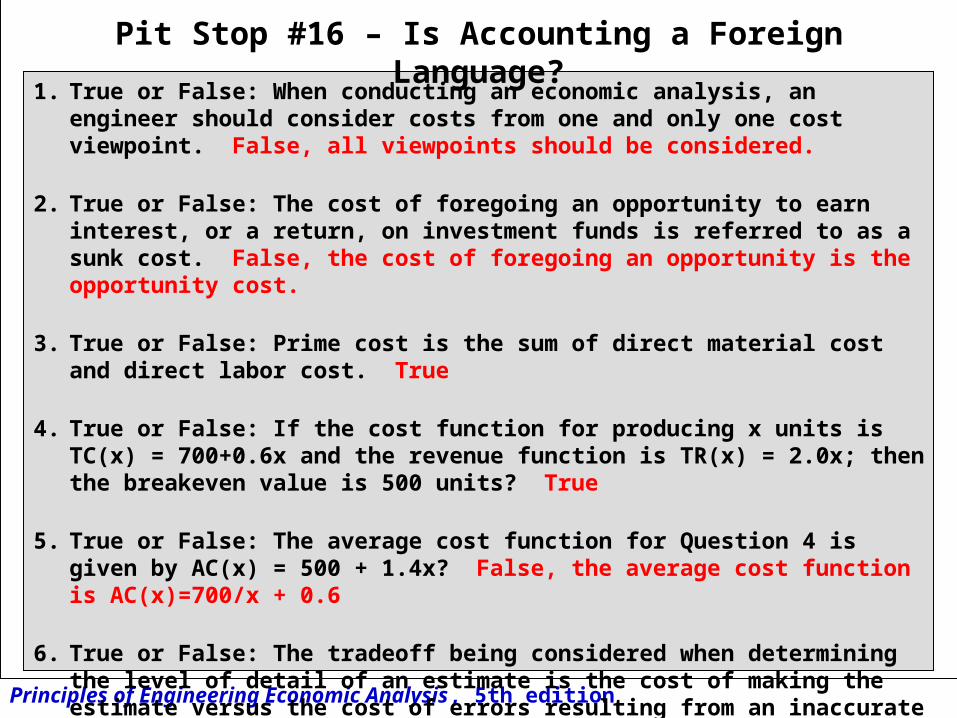

1. True or False: When conducting an economic analysis, an engineer should consider costs from one and only one cost viewpoint.

2. True or False: The cost of foregoing an opportunity to earn interest, or a return, on investment funds is referred to as a sunk cost.

3. True or False: Prime cost is the sum of direct material cost and direct labor cost.

4. True or False: If the cost function for producing x units is TC(x) = 700+0.6x and the revenue function is TR(x) = 2.0x; then the breakeven value is 500 units.

5. True or False: The average cost function for Question 4 is given by AC(x) = 500 + 1.4x

6. True or False: The tradeoff being considered when determining the level of detail of an estimate is the cost of making the estimate versus the cost of errors resulting from an inaccurate estimate

Pit Stop #16 – Is Accounting a Foreign Language?

Principles of Engineering Economic Analysis, 5th edition

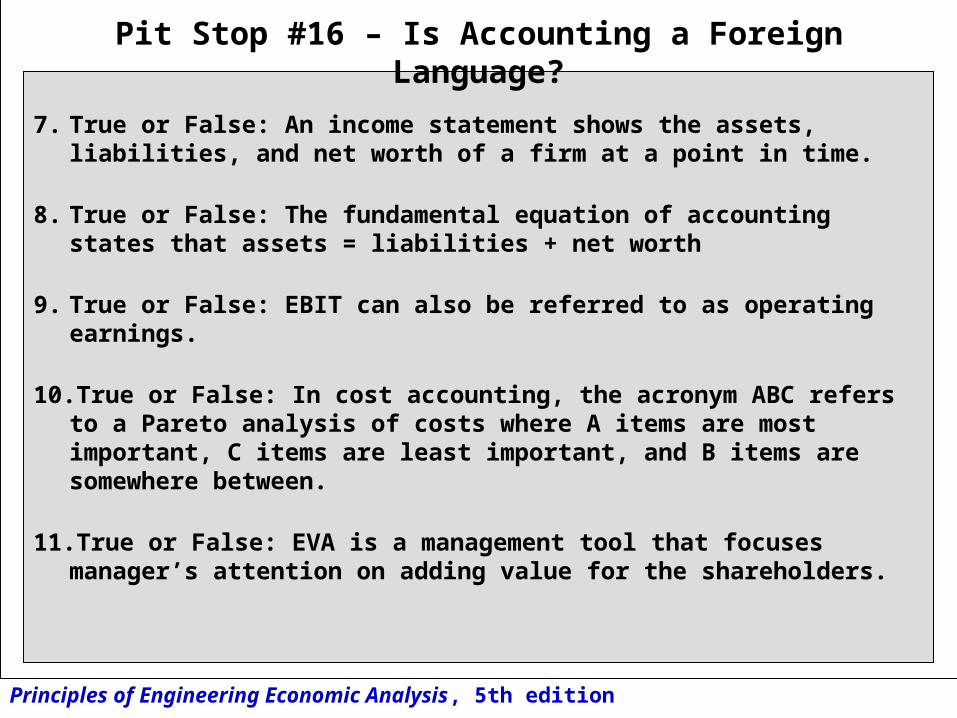

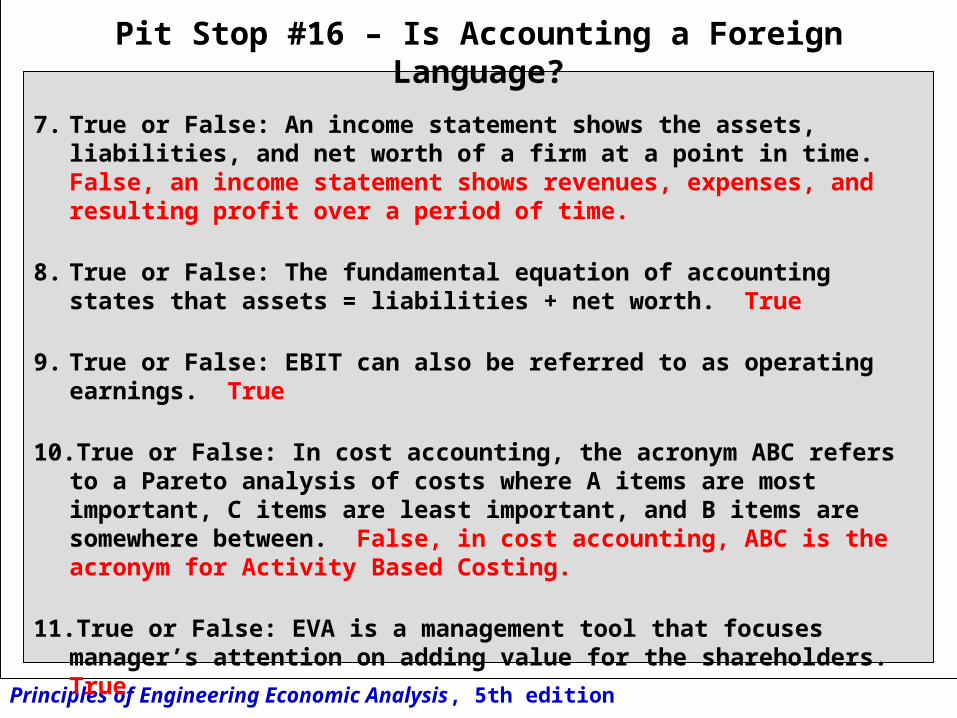

7. True or False: An income statement shows the assets, liabilities, and net worth of a firm at a point in time.

8. True or False: The fundamental equation of accounting states that assets = liabilities + net worth

9. True or False: EBIT can also be referred to as operating earnings.

10.True or False: In cost accounting, the acronym ABC refers to a Pareto analysis of costs where A items are most important, C items are least important, and B items are somewhere between.

11.True or False: EVA is a management tool that focuses manager’s attention on adding value for the shareholders.

Pit Stop #16 – Is Accounting a Foreign Language?

Principles of Engineering Economic Analysis, 5th edition

1. True or False: When conducting an economic analysis, an engineer should consider costs from one and only one cost viewpoint. False, all viewpoints should be considered.

2. True or False: The cost of foregoing an opportunity to earn interest, or a return, on investment funds is referred to as a sunk cost. False, the cost of foregoing an opportunity is the opportunity cost.

3. True or False: Prime cost is the sum of direct material cost and direct labor cost. True

4. True or False: If the cost function for producing x units is TC(x) = 700+0.6x and the revenue function is TR(x) = 2.0x; then the breakeven value is 500 units? True

5. True or False: The average cost function for Question 4 is given by AC(x) = 500 + 1.4x? False, the average cost function is AC(x)=700/x + 0.6

6. True or False: The tradeoff being considered when determining the level of detail of an estimate is the cost of making the estimate versus the cost of errors resulting from an inaccurate estimate. True

Pit Stop #16 – Is Accounting a Foreign Language?

Principles of Engineering Economic Analysis, 5th edition

7. True or False: An income statement shows the assets, liabilities, and net worth of a firm at a point in time. False, an income statement shows revenues, expenses, and resulting profit over a period of time.

8. True or False: The fundamental equation of accounting states that assets = liabilities + net worth. True

9. True or False: EBIT can also be referred to as operating earnings. True

10.True or False: In cost accounting, the acronym ABC refers to a Pareto analysis of costs where A items are most important, C items are least important, and B items are somewhere between. False, in cost accounting, ABC is the acronym for Activity Based Costing.

11.True or False: EVA is a management tool that focuses manager’s attention on adding value for the shareholders. True

Pit Stop #16 – Is Accounting a Foreign Language?