penghentian aktiva tetap

DESCRIPTION

weldaTRANSCRIPT

Pengertian Aktiva Tetap

Aktiva tetap adalah aktiva (kekayaan) yang dimiliki perusahaan yang diperoleh dalam

bentuk siap pakai atau dibangun terlebih dahulu, sifatnya permanen dan digunakan dalam

kegiatan normal perusahaan untuk jangka panjang serta mempunyai nilai cukup material.

Aktiva tetap mempunyai karakteristik sebagai berikut:

1. Digunakan dalm kegiatan normal perusahaan, artinya tetap dimiliki untuk digunakan

dalam operasi perusahaan bukan untuk dijual kembali (barang dagangan), atau

investasi.

2. Masa manfaatnya lebih dari satu tahun atau satu siklus operasi normal perusahaan,

dan nilai manfaatnya dapat diukur.

3. Mempunyai nilai yang cukup material, artinya nilai/harga aktiva tersebut cukup

tinggi. Misalnya: tanah, bangunan, mesin-mesin, inventaris, peralatan, kendaraan.

Sedang aktiva yang nilainya relatif kecil, walaupun dapat digunakan dalam jangka

panjang, tidak digolongkan sebagai aktiva tetap. Misalnya: pulpen, kalkulator,

gunting.

4. Memiliki wujud fisik.

Berdasarkan sifatnya, aktiva tetap dibagi atas:

aktiva tetap berwujud (tangible fixed assets), dan

aktiva tetap tak berwujud (intangible fixed assets).

Aktiva tetap 1

Aktiva tetap berwujud seringkali disebut saja aktiva tetap, yaitu aktiva tetap yang

mempunyai bentuk fisik, dalam hal ini terdapat tiga jenis aktiva tetap berwujud, yaitu

1. Aktiva yang merupakan sumber penyusutan (depresiasi), seperti gedung, peralatan,

inventaris/equipment, kendaraan.

2. Aktiva yang merupakan sumberdeplesi, seperti tambang mineral/sumber-sumber

alam (mineral deposits).

3. Aktiva yang tidak mengalami penyusutan atau deplesi, seperti tanah untuk tempat

bangunan perusahaan.

Aktiva Tidak Berwujud ( Intangible Asset ) Yaitu aktiva yang tidak memilki wujud fisik,

tetapi mempunyai nilai/manfaat bagi perusahaan yang dinyatakan dalam bentuk jaminan

tertentu, seperti hak paten, goodwill, hak cipta, hak monopoli, merek dagang, biaya riset dan

pengembangan, dan biaya pendirian perusahaan.

Harga Perolehan Harta TetapHarga perolehan harta tetap adalah harga yang akan dipakai sebagai dasar pelaporan

harta tetap dalam neraca perusahaan dan akan dijadikan dasar perhitungan penyusutan harta

Aktiva tetap 2

tetap yang bersangkutan. Nilai ini terdiri dari harga beli harta yang bersangkutan ditambah

dengan biaya-biaya yang dikeluarkan dan diperhitungkan samapi harta tetap yang

bersangkutan dapat dipergunakan atau dimanfaatkan. Biaya-biaya yang dimaksud adalah :

Biaya persiapan tempat

Biaya pengiriman awal

Biaya pemasangan

Biaya konsultan

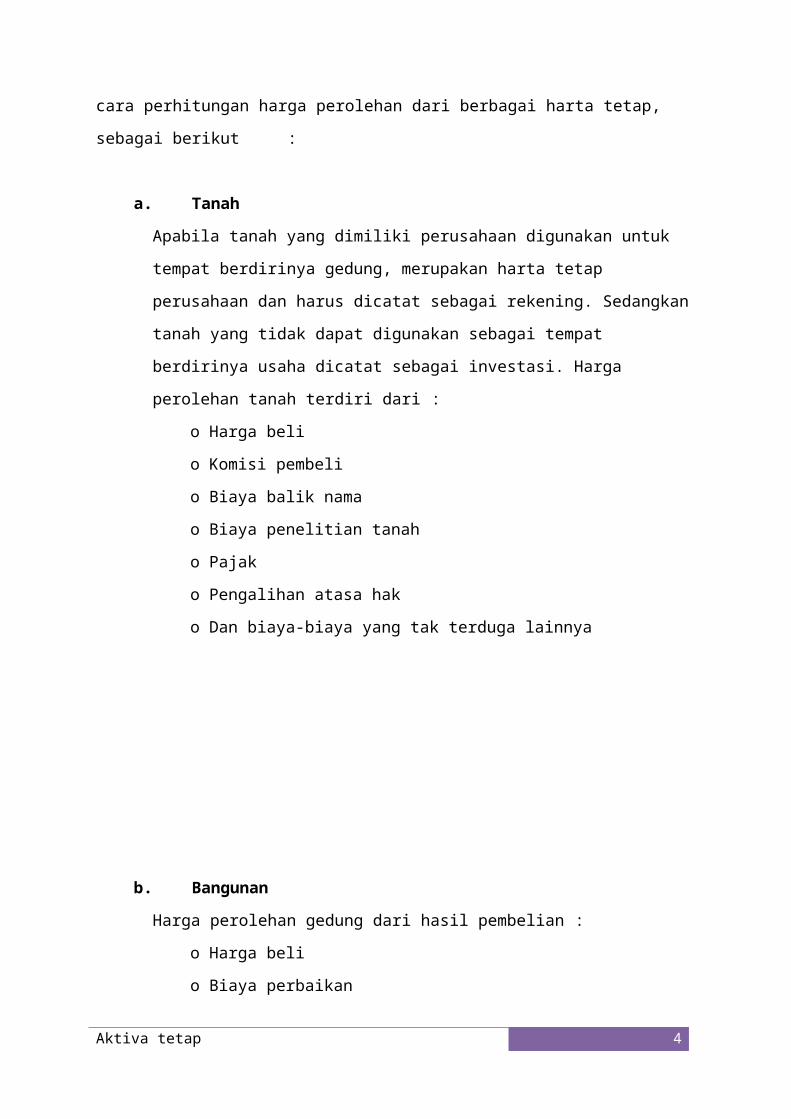

Dalam penghitungan harga tetap memiliki masalah-masalah yang berbeda, maka harga

perolehan akan berbeda. Dibawah ini adalah cara perhitungan harga perolehan dari berbagai

harta tetap, sebagai berikut :

a. Tanah

Apabila tanah yang dimiliki perusahaan digunakan untuk tempat berdirinya gedung,

merupakan harta tetap perusahaan dan harus dicatat sebagai rekening. Sedangkan

tanah yang tidak dapat digunakan sebagai tempat berdirinya usaha dicatat sebagai

investasi. Harga perolehan tanah terdiri dari :

o Harga beli

o Komisi pembeli

o Biaya balik nama

o Biaya penelitian tanah

o Pajak

o Pengalihan atasa hak

o Dan biaya-biaya yang tak terduga lainnya

b. Bangunan

Harga perolehan gedung dari hasil pembelian :

Aktiva tetap 3

o Harga beli

o Biaya perbaikan

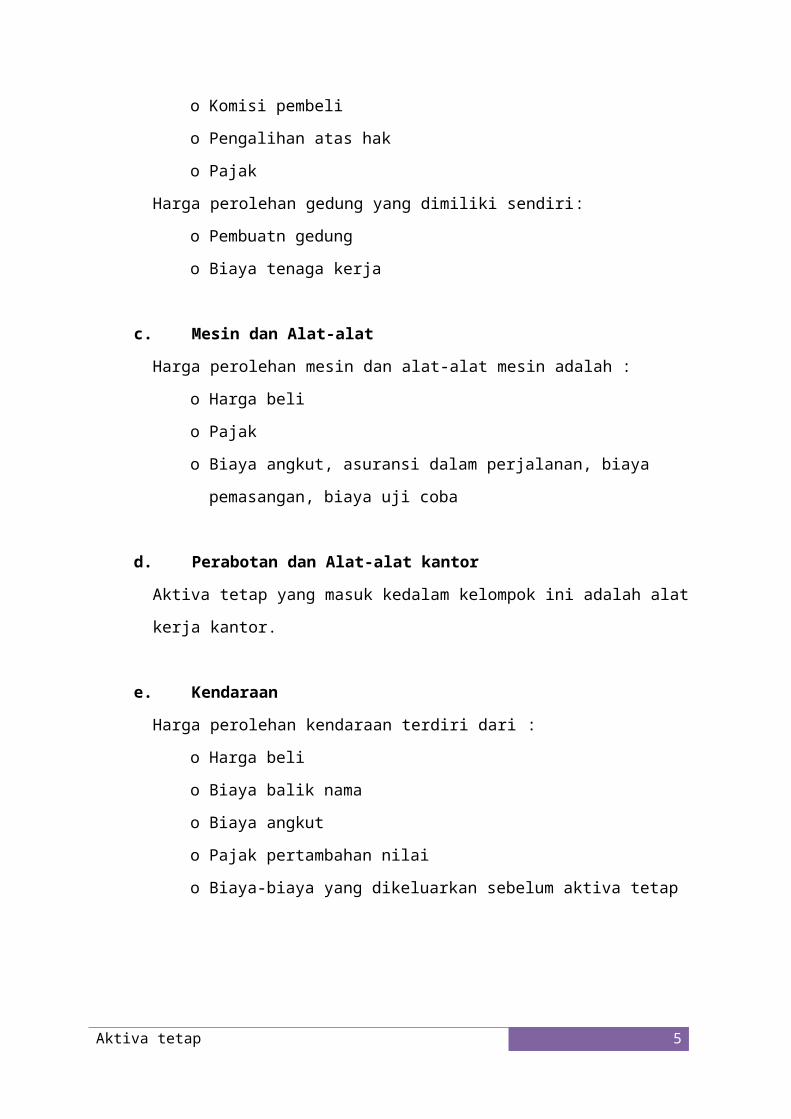

o Komisi pembeli

o Pengalihan atas hak

o Pajak

Harga perolehan gedung yang dimiliki sendiri :

o Pembuatn gedung

o Biaya tenaga kerja

c. Mesin dan Alat-alat

Harga perolehan mesin dan alat-alat mesin adalah :

o Harga beli

o Pajak

o Biaya angkut, asuransi dalam perjalanan, biaya pemasangan, biaya uji coba

d. Perabotan dan Alat-alat kantor

Aktiva tetap yang masuk kedalam kelompok ini adalah alat kerja kantor.

e. Kendaraan

Harga perolehan kendaraan terdiri dari :

o Harga beli

o Biaya balik nama

o Biaya angkut

o Pajak pertambahan nilai

o Biaya-biaya yang dikeluarkan sebelum aktiva tetap

Penyusutan Harta Tetap

Aktiva tetap 4

Besar kecilnya niali penyusutan ditentukan oleh :

1. Harga perolehan ( Cost )

Uang atau biaya yang diperhitungkan terhadap harta tetap yang bersangkutan

sampai harta tetap tersebut dapat digunakan atau dimanfaatkan.

2. Nilai sisa atau nilai residu ( Residual or Salvage Value )

Nilai residu tidak mesti ada, nilai residu hanya nilai taksiran realisasi

penjualan aktiva tetap setelah habis manfaatnya.

3. Perkiraan umur ekonomis ( Usefull Live )

Perkiraan seberapa lama sebuah harta tetap dapat dimanfaatkan.

4. Metode perhitungan yang digunakan

Dalam menghitung nilai penyusutan dalam harta tetap, metode yang

digunakan sangat mempengaruhi nilainya. Namun dalam perhitungan

penyusutan harta haruslah konsisten.

Metode Perhitungan Penyusutan

A. Penyusutan yang didasari oleh factor waktu pemakaian

Aktiva tetap 5

1. Metode Garis Lurus ( Straight Line

Method )

Istilah lain dari metode garis lurus adalah straigt line method, di dalam metode ini

beban penyusutan aktiva tetap pertahunnya akan sama sampai akhir umur ekonomis aktiva

tetap tersebut.

Rumusnya:

Penyusutan = Harga perole h an−Nilai Residu

umur ekonomis /manfaat

Dapat juga dicari dengan cara lain:

Menghitung tarif penyusutan tiap tahun

Tarif penyusutan = 100 %

umur ekonomis /manfaat

Menghitung beban penyusutan tiap tahun

Beban penyusutan = tarif penyusutan x (harga perolehan – nilai residu)

Menghitung nilai buku aktiva tetap

Harga buku aktiva tetap = harga perolehan – akumulasi penyusutan

Examples of working out when the engine / vehicle used at the beginning of the year

In January 2010, Selecta Electronic Stores buy a machine with price Rp165.000.000 type x,

Before to normal operation, incurred the following costs:

Transportation costs Rp1.500.000

Aktiva tetap 6

Installation costs Rp2.350.000

The cost of trial and servic Rp1.750.000

The machine began operation on January 6, 2012 with the estimated economic life of 10 years and a

residual value Rp2.600.000

Requested:

a. Calculate the cost of the machine

b. Make a chart of depreciation to the straight line method

Completion:

b. Depreciation tables

Year Acquisition Price

Depreciation Expense

Accumulated

Depreciatio

Book Value

Aktiva tetap 7

a. Acquisition price of the machine is:

~The purchase price Rp165.000.000

~ Freight Rp1.500.000

~ The cost of installing Rp2.350.000

~ Cost experiments and servic Rp1.750.000

The amount of additional costs Rp 5.600.000

Machine acquisition cost Rp170.600.000

Depreciation of the year =

(170.600 .000−2.600.000)10

= Rp 16.800.000,-

n2012 Rp 170,600,000 Rp 16,800,000 Rp 16,800,000 Rp 153,800,000

2013 Rp 170,600,000 Rp 16,800,000 Rp 33,600,000 Rp 137,000,000

2014 Rp 170,600,000 Rp 16,800,000 Rp 50,400,000 Rp 120,200,000

2015 Rp 170,600,000 Rp 16,800,000 Rp 67,200,000 Rp 103,400,000

2016 Rp 170,600,000 Rp 16,800,000 Rp 84,000,000 Rp 86,600,000

2017 Rp 170,600,000 Rp 16,800,000 Rp 100,800,000 Rp 69,800,000

2018 Rp 170,600,000 Rp 16,800,000 Rp 117,600,000 Rp 53,000,000

2019 Rp 170,600,000 Rp 16,800,000 Rp 134,400,000 Rp 36,200,000

2020 Rp 170,600,000 Rp 16,800,000 Rp 151,200,000 Rp 19,400,000

2021 Rp 170,600,000 Rp 16,800,000 Rp 168,000,000 Rp 2,600,000

Jumlah Rp 168,000,000

Tabel 1.1

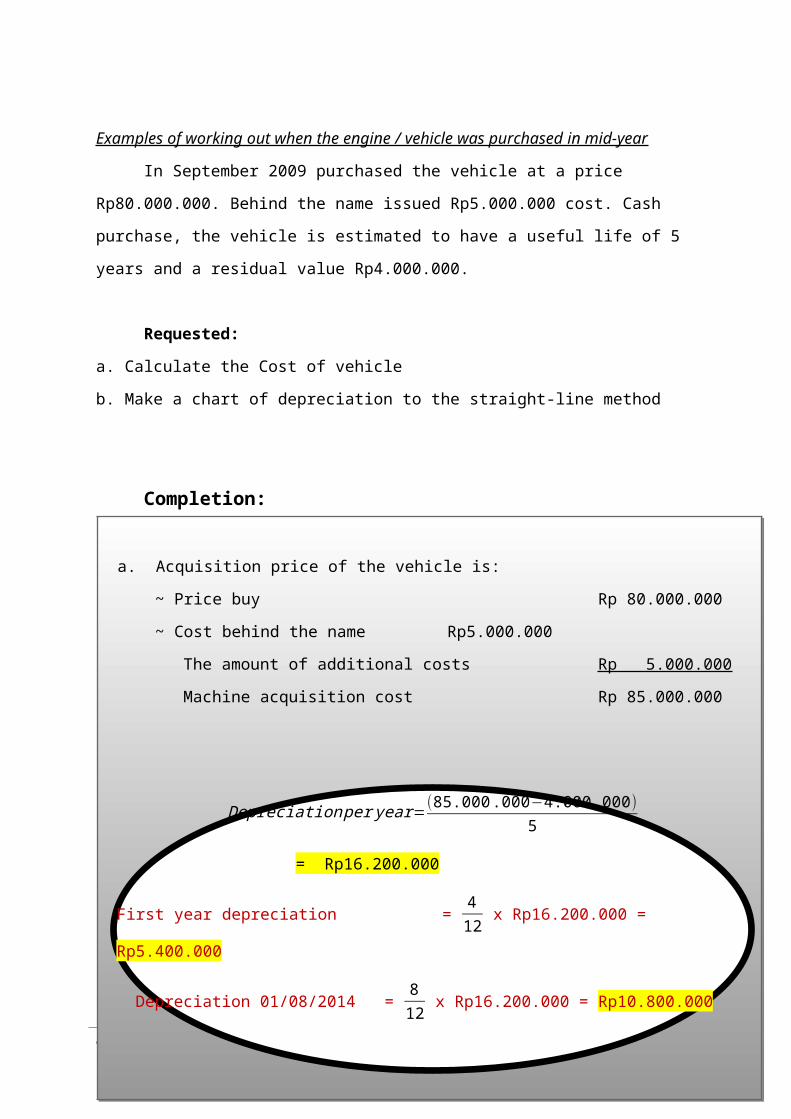

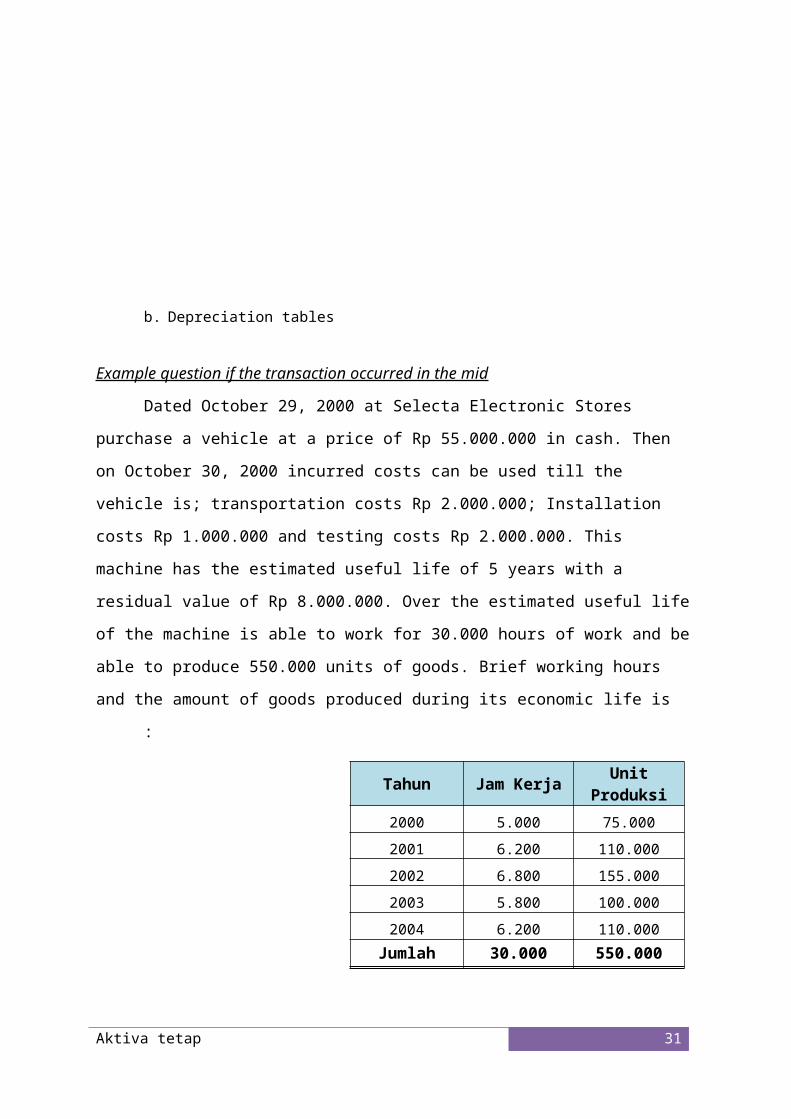

Examples of working out when the engine / vehicle was purchased in mid-year

In September 2009 purchased the vehicle at a price Rp80.000.000. Behind the name

issued Rp5.000.000 cost. Cash purchase, the vehicle is estimated to have a useful life of 5

years and a residual value Rp4.000.000.

Aktiva tetap 8

Requested:

a. Calculate the Cost of vehicle

b. Make a chart of depreciation to the straight-line method

Completion:

b. Depreciation tables

YearAcquisition

PriceDepreciation

ExpenseAccumulated Depreciation

Book Value

2009 Rp 85,000,000 Rp 5,400,000 Rp 5,400,000 Rp 79,600,000

Aktiva tetap 9

a. Acquisition price of the vehicle is:

~ Price buy Rp 80.000.000

~ Cost behind the name Rp5.000.000

The amount of additional costs Rp 5.000.000

Machine acquisition cost Rp 85.000.000

Depreciation per year=(85.000 .000−4.000 .000)

5

= Rp16.200.000

First year depreciation = 4

12 x Rp16.200.000 = Rp5.400.000

Depreciation 01/08/2014 = 8

12 x Rp16.200.000 = Rp10.800.000

2010 Rp 85,000,000 Rp 16,200,000 Rp 21,600,000 Rp 63,400,000

2011 Rp 85,000,000 Rp 16,200,000 Rp 37,800,000 Rp 47,200,000

2012 Rp 85,000,000 Rp 16,200,000 Rp 54,000,000 Rp 31,000,000

2013 Rp 85,000,000 Rp 16,200,000 Rp 70,200,000 Rp 14,800,000

01/09/2014 Rp 85,000,000 Rp 10,800,000 Rp 81,000,000 Rp 4,000,000

Jumlah Rp 81.000.000

Tabel 1.2

Note: In the first year and last year made such a

because, purchases made by mid-year

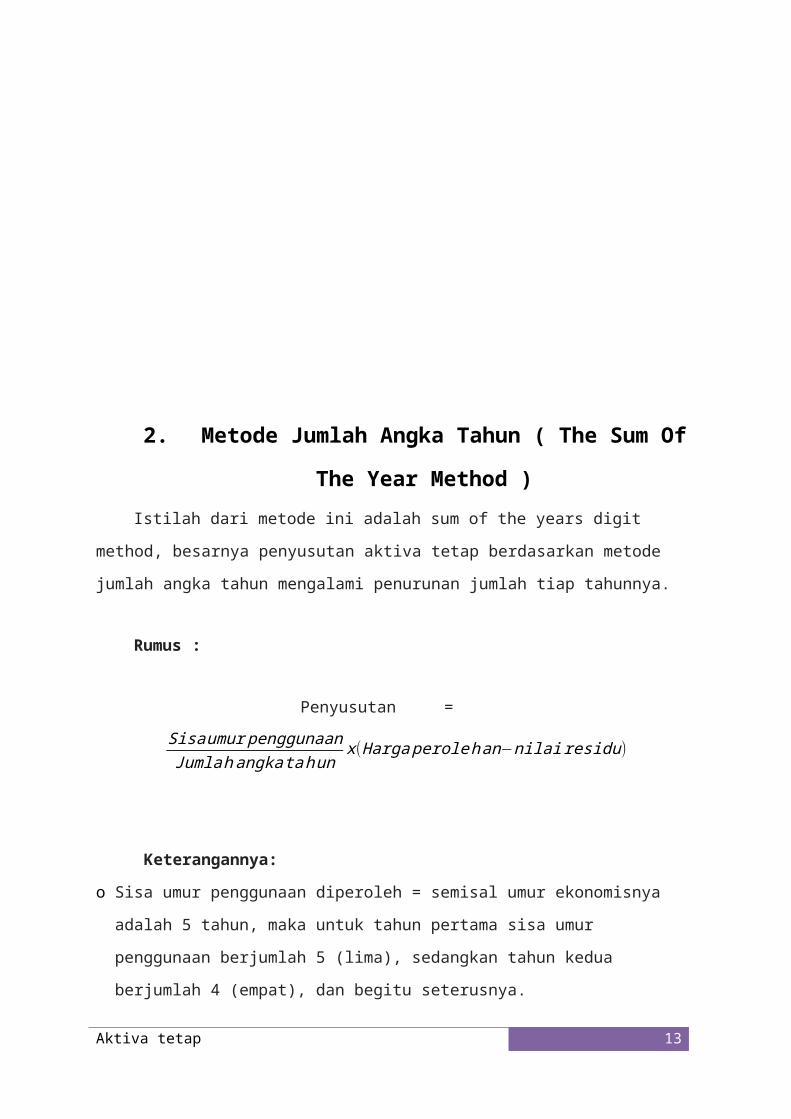

2. Metode Jumlah Angka Tahun ( The Sum

Of The Year Method )

Istilah dari metode ini adalah sum of the years digit method, besarnya penyusutan

aktiva tetap berdasarkan metode jumlah angka tahun mengalami penurunan jumlah tiap

tahunnya.

Aktiva tetap 10

Rumus :

Penyusutan = Sisa umur penggunaanJumlah angka tahun

x (Harga perolehan−nilai residu)

Keterangannya:

o Sisa umur penggunaan diperoleh = semisal umur ekonomisnya adalah 5 tahun, maka untuk

tahun pertama sisa umur penggunaan berjumlah 5 (lima), sedangkan tahun kedua

berjumlah 4 (empat), dan begitu seterusnya.

o Jumlah angka tahun diperoleh = semisal umur ekonomisnya adalah 5 tahun, maka

perhitungan jumlah angka tahunnya 1+2+3+4+5=15

o Harga buku aktiva = harga perolehan dikurangi nilai residu

Elektronic Selecta shop is a shop selling goods Electonic. Purchase machines made by

this shop in 2011 :

On January 3, 2012 Shop Selecta Elektronic buy 1 piece engine coolant at a price of

Rp10,000,000 incurred costs amounting to Rp100,000 freight engine. The purchases

made in cash. This machine has the estimated useful life of 5 years and a residual

value of Rp1.500.000.

Aktiva tetap 11

On July 31, 2012 Shop Selecta Elektronic buy 3 pieces with harga @ Rp 15.500.000

refrigeration, transport costs incurred sebesar @ Rp 250.000 machine. The purchases

made in cash. This machine has the estimated useful life of 5 years and the value

residu @Rp3.500.00.

Requested:

a. Calculate depreciation of the year

b. Make a chart of depreciation by Sum Of The Year Method

Completion:

Aktiva tetap 12

a. Date 3 January 2012

Acquisition price of the machine is:

~ Purchase price Rp 10.000.000

~ Freight cost Rp 100.000

The amount of additional costs Rp 100.000

Machine acquisition cost Rp 10.100.000

Unknow :

• Cost of machine Rp10.100.00

b. Depreciation tables

Year

Acquisition Price

Depreciation Expense

Accumulated Depreciation

Book Value

2012 Rp 10,100,000 Rp 2,866,667 Rp 2,866,667 Rp 7,233,333

2013 Rp 10,100,000 Rp 2,293,333 Rp 5,160,000 Rp 4,940,000

2014 Rp 10,100,000 Rp 1,720,000 Rp 6,880,000 Rp 3,220,000

Aktiva tetap 13

a. Date 3 January 2012

Acquisition price of the machine is:

~ Purchase price Rp 10.000.000

~ Freight cost Rp 100.000

The amount of additional costs Rp 100.000

Machine acquisition cost Rp 10.100.000

Unknow :

• Cost of machine Rp10.100.00

2015 Rp 10,100,000 Rp 1,146,667 Rp 8,026,667 Rp 2,073,333

2016 Rp 10,100,000 Rp 573,333 Rp 8,600,000 Rp 1,500,000

Jumlah Rp

8,600,000

Tabel 2.1

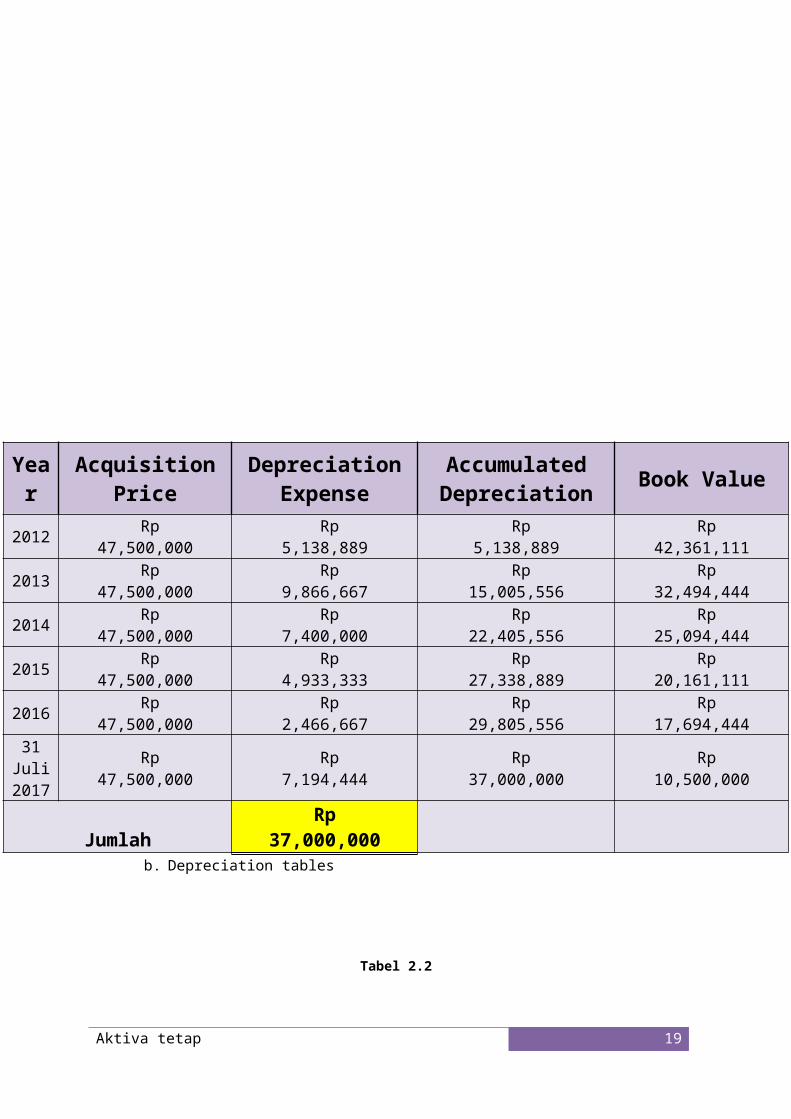

Completion:

Aktiva tetap 14

a. Dated July 31, 2012

Acquisition price of the machine is:

~ Price Buy 3 x @Rp 15.500.000 Rp

46.500.000

~ Load haul purchase 3 x @ Rp 250.000 Rp 750,000

The amount of additional costs Rp

750.000

Machine acquisition cost Rp

47.250.000

Unknow :

Cost of machine Rp 47.500.000

Residual value of 3 x @ Rp 3.500.000 = Rp 10.500.000

Year

Acquisition Price

Depreciation Expense

Accumulated Depreciation

Book Value

2012 Rp 47,500,000 Rp 5,138,889 Rp 5,138,889 Rp 42,361,111

2013 Rp 47,500,000 Rp 9,866,667 Rp 15,005,556 Rp 32,494,444

2014 Rp 47,500,000 Rp 7,400,000 Rp 22,405,556 Rp 25,094,444

2015 Rp 47,500,000 Rp 4,933,333 Rp 27,338,889 Rp 20,161,111

2016 Rp 47,500,000 Rp 2,466,667 Rp 29,805,556 Rp 17,694,444

31 Juli 2017

Rp 47,500,000 Rp 7,194,444 Rp 37,000,000 Rp 10,500,000

Aktiva tetap 15

a. Dated July 31, 2012

Acquisition price of the machine is:

~ Price Buy 3 x @Rp 15.500.000 Rp

46.500.000

~ Load haul purchase 3 x @ Rp 250.000 Rp 750,000

The amount of additional costs Rp

750.000

Machine acquisition cost Rp

47.250.000

Unknow :

Cost of machine Rp 47.500.000

Residual value of 3 x @ Rp 3.500.000 = Rp 10.500.000

JumlahRp

37,000,000 b. Depreciation tables

Tabel 2.2

3. Metode Slado menurun dengan

persentase dua kali garis lurus

( Double declining balance )

Istilah lain dari metode ini adalah Double Declining Balance Methode. Di dalam metode ini, penyusutan aktiva tetap dapat ditentukan melalui persentase tertentu yang dicari dari harga buku pada tahun bersangkutan. Untuk menghitung persentase penyusutan dapat diperoleh dengan mengalikan persentase penyusutan yang diperoleh dengan metode garis lurus dikalikan angka 2. Jadi, besarnya persentase penyusutan 2 kali dari persentase atau tarif penyusutan metode garis lurus.

Rumus :

Penysutan = [ 2 x (100% : umur ekonomis )] x harga buku aktiva tetap

Aktiva tetap 16

Example about when the transaction occurred at the beginning of the year

Electronic Selecta shop on January 1, 2010 to buy a machine with a price of Rp

13.500.000, in cash. Then on January 3, 2010 incurred costs until the machine can be used

are: transportation costs Rp 2,500,000 and Rp 1.500.000 Costs trials. This machine has the

estimated useful life of 5 years with a residual value of Rp 4.000.000

Requested :

a. Calculate depreciation of the year

b. Make a chart of depreciation using the Double declining balance method

Completion:

Aktiva tetap 17

a. Purchase price of the machine is:~ Purchase price Rp 13.500.000~ Transportation costs Rp 2.500.000~ Trial costs Rp 1.500.000

The amount of additional costs Rp 4.000.000Machine acquisition cost Rp 17.500.000

Unknow :

Cost of machine Rp 17.500.000

Residual value of Rp 4.000.000

Economic value 5 years

Percentage of depreciation = 2 x15

x100 %

= 2 x 20%= 40%

b. Depreciation tables

Year

Acquisition Price

Depreciation Expense

Accumulated

Depreciation

Book Value

2010 Rp 17,500,000 Rp 7,000,000 Rp 7,000,000 Rp 10,500,000

2011 Rp 17,500,000 Rp 4,200,000 Rp 11,200,000 Rp 6,300,000

2012 Rp 17,500,000 Rp 2,520,000 Rp 13,720,000 Rp 3,780,000

2013 Rp 17,500,000 Rp 1,512,000 Rp 15,232,000 Rp 2,268,000

2014 Rp 17,500,000 Rp 907,200 Rp 16,139,200 Rp 1,360,800

Aktiva tetap 18

a. Purchase price of the machine is:~ Purchase price Rp 13.500.000~ Transportation costs Rp 2.500.000~ Trial costs Rp 1.500.000

The amount of additional costs Rp 4.000.000Machine acquisition cost Rp 17.500.000

Unknow :

Cost of machine Rp 17.500.000

Residual value of Rp 4.000.000

Economic value 5 years

Percentage of depreciation = 2 x15

x100 %

= 2 x 20%= 40%

Jumlah Rp 16,139,200

Tabel 3.1

Example question if the transaction occurred in the mid

Vehicles purchased in January at a price of Rp 65,000,000, issued under the name of

cost of Rp 1,000,000. Cash purchase and began operation on 6 September 2010. This vehicle

possessed estimated useful life of 5 years and a residual value of Rp 7,000,000

Requested :

a. Calculate depreciation of the year

b. Make a chart of depreciation using the Double declining balance method

Completion :

Aktiva tetap 19

a. Purchase price of the machine is:~ Purchase price Rp 65.000.000~ Cost under the name Rp 1.000.000

The amount of additional costs Rp 1.000.000Machine acquisition cost Rp 66.000.000

Unknow :

Cost of machine Rp 66.000.000

Residual value of Rp 7.000.000

Economic value 5 years

b. Depreciation tables

Year Acquisition Price

Depreciation Expense

Accumulated

Depreciation

Book Value

2010 Rp 66,000,000 Rp 6,600,000 Rp 6,600,000 Rp 59,400,000

2011 Rp 66,000,000 Rp 23,760,000 Rp 30,360,000 Rp 35,640,000

2012 Rp 66,000,000 Rp 14,256,000 Rp 44,616,000 Rp 21,384,000

2013 Rp 66,000,000 Rp 8,553,600 Rp 53,169,600 Rp 12,830,400

2014 Rp 66,000,000 Rp 5,132,160 Rp 58,301,760 Rp 7,698,240

Sep 2015 Rp 66,000,000 Rp 3,849,120 Rp 62,150,880 Rp 3,849,120

Jumlah Rp 62,150,880

Aktiva tetap 20

a. Purchase price of the machine is:~ Purchase price Rp 65.000.000~ Cost under the name Rp 1.000.000

The amount of additional costs Rp 1.000.000Machine acquisition cost Rp 66.000.000

Unknow :

Cost of machine Rp 66.000.000

Residual value of Rp 7.000.000

Economic value 5 years

Tabel 3.2

B. Berdasarkan faktor penggunaannya

4. Metode Unit Produksi ( Method of

Production Unit )

Istilah lainnya adalah Method of production unit. Di dalam metode ini penetapan beban

penyusutan aktiva tetap didasarkan pada jumlah satuan produk yang dihasilkan pada periode

yang bersangkutan.

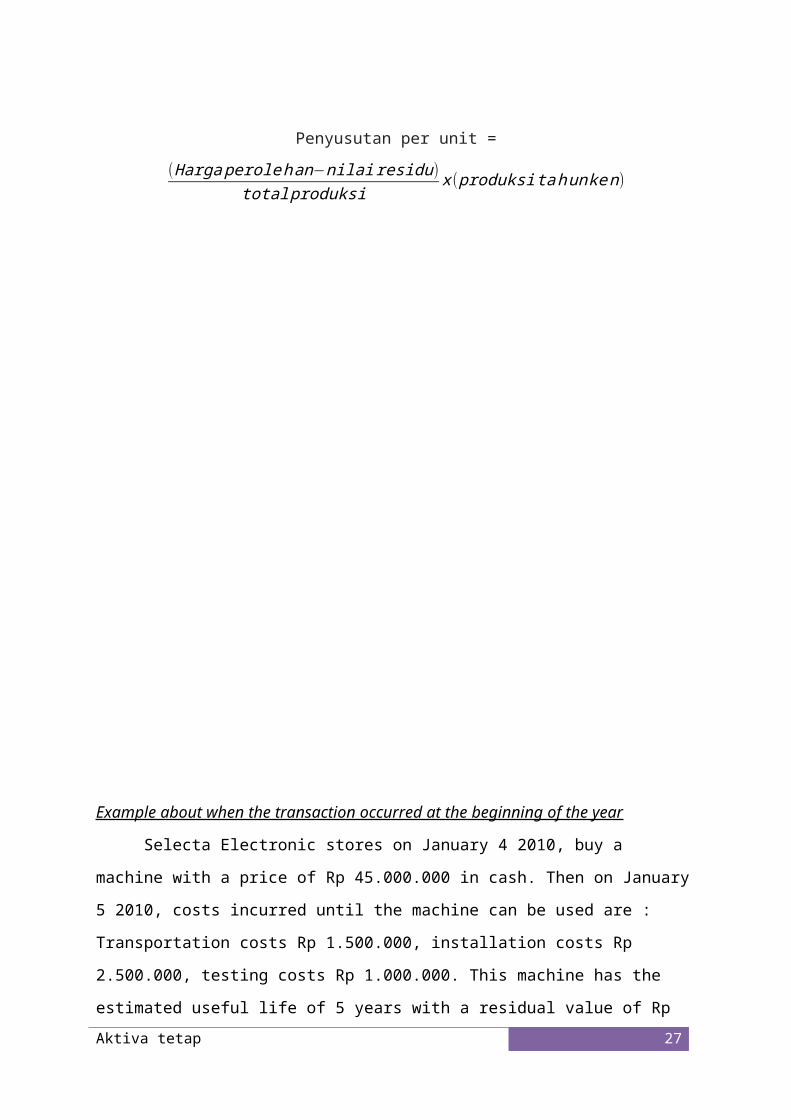

Rumus:

Penyusutan per tahun = unit produksi ta h un ke−n

total produksix (h arga peroleh an−residu)

Penyusutan per unit = (Harga peroleh an−nilai residu)

total produksix ( produksi ta hun ke n)

Aktiva tetap 21

Example about when the transaction occurred at the beginning of the year

Selecta Electronic stores on January 4 2010, buy a machine with a price of Rp

45.000.000 in cash. Then on January 5 2010, costs incurred until the machine can be used are

:

Transportation costs Rp 1.500.000, installation costs Rp 2.500.000, testing costs Rp

1.000.000. This machine has the estimated useful life of 5 years with a residual value of Rp

4.000.000. During msa benefit of this machine is estimated to work for 24.000 hours of work

and be able to produce 400.000 units of goods. Summary of hours and the amount of goods

that will be produced during its economic life is :

Aktiva tetap 22

Tahun Jam KerjaUnit

Produksi2010 4.500 75.0002011 5.200 80.0002012 6.000 90.0002013 4.300 85.0002014 4.000 70.000

Jumlah 24.000 400.000

Requested :

a. Calculate depreciation of the year

b. Make a chart of depreciation using the Method of Production Unit

Completion :

Aktiva tetap 23

a. Purchase price of the machine is:~ Purchase price Rp 45.000.000~ Transportation costs Rp 1.500.000~ Installation costs Rp 2.500.000~ Testing costs Rp 1.000.000

The amount of additional costs Rp 5.000.000Machine acquisition cost Rp 50.000.000

Unknow :

Cost of machine Rp 50.000.000

Residual value of Rp 4.000.000

Economic value 5 years

Tahun Jam KerjaUnit

Produksi2010 4.500 75.0002011 5.200 80.0002012 6.000 90.0002013 4.300 85.0002014 4.000 70.000

Jumlah 24.000 400.000

Machine depreciation of year :

a. Year depreciation 2010= = Rp 8.625.000

b. Depreciation tables

Year

Acquisition Price

Depreciation Expense

Accumulated Depreciation Book Value

2010 Rp 50,000,000 Rp 8,625,000 Rp 8,625,000 Rp 41,375,000

2011 Rp 50,000,000 Rp 9,200,000 Rp 17,825,000 Rp 32,175,000

2012 Rp 50,000,000 Rp 10,350,000 Rp 28,175,000 Rp 21,825,000

2013 Rp 50,000,000 Rp 9,775,000 Rp 37,950,000 Rp 12,050,000

2014 Rp 50,000,000 Rp 8,050,000 Rp 46,000,000 Rp 4,000,000

Jumlah Rp

46,000,000

Tabel 4.1

Aktiva tetap 24

a. Purchase price of the machine is:~ Purchase price Rp 45.000.000~ Transportation costs Rp 1.500.000~ Installation costs Rp 2.500.000~ Testing costs Rp 1.000.000

The amount of additional costs Rp 5.000.000Machine acquisition cost Rp 50.000.000

Unknow :

Cost of machine Rp 50.000.000

Residual value of Rp 4.000.000

Economic value 5 years

Tahun Jam KerjaUnit

Produksi2010 4.500 75.0002011 5.200 80.0002012 6.000 90.0002013 4.300 85.0002014 4.000 70.000

Jumlah 24.000 400.000

Machine depreciation of year :

a. Year depreciation 2010= = Rp 8.625.000

b. Depreciation tables

Example question if the transaction occurred in the mid

Dated October 29, 2000 at Selecta Electronic Stores purchase a vehicle at a price of

Rp 55.000.000 in cash. Then on October 30, 2000 incurred costs can be used till the vehicle

is; transportation costs Rp 2.000.000; Installation costs Rp 1.000.000 and testing costs Rp

2.000.000. This machine has the estimated useful life of 5 years with a residual value of Rp

8.000.000. Over the estimated useful life of the machine is able to work for 30.000 hours of

work and be able to produce 550.000 units of goods. Brief working hours and the amount of

goods produced during its economic life is :

Requested :

a. Calculate depreciation of the year

Aktiva tetap 25

Tahun Jam KerjaUnit

Produksi

2000 5.000 75.000

2001 6.200 110.000

2002 6.800 155.000

2003 5.800 100.000

2004 6.200 110.000

Jumlah 30.000 550.000

b. Make a chart of depreciation using the Method of Production Unit

Completion :

Aktiva tetap 26

a. Purchase price of the machine is:~ Purchase price Rp 55.000.000~ Transportation costs Rp 2.000.000~ Installation costs Rp 1.000.000~ Testing costs Rp 2.000.000

The amount of additional costs Rp 5.000.000Machine acquisition cost Rp 60.000.000

Unknow :

Cost of machine Rp 60.000.000

Residual value of Rp 8.000.000

Economic value 5 years

Tahun Jam KerjaUnit

Produksi2000 5.000 75.000

2001 6.200 110.000

2002 6.800 155.000

2003 5.800 100.000

2004 6.200 110.000Jumlah 30.000 550.000

Machine depreciation of year :

a. Year depreciation 2010 =75.000550.00

x (60.000 .000−8.000.000) = Rp 7.090.909

=2

12x7.090 .909 = Rp 1.181.818

b. Depreciation tables

Year Acquisition Price

Depreciation Expense

Accumulated Depreciation

Book Value

2010 Rp 60,000,000 Rp 1,181,818 Rp 1,181,818 Rp 58,818,182

2011 Rp 60,000,000 Rp 10,400,000 Rp 11,581,818 Rp 48,418,182

2012 Rp 60,000,000 Rp 14,654,546 Rp 26,236,364 Rp 33,763,636

2013 Rp 60,000,000 Rp 9,454,545 Rp 35,690,909 Rp 24,309,091

2014 Rp 60,000,000 Rp 10,400,000 Rp 46,090,909 Rp 13,909,091

Oct 2015 Rp 60,000,000 Rp 5,909,091 Rp 52,000,000 Rp 8,000,000

Jumlah Rp

52,000,000

Tabel 4.2

Aktiva tetap 27

a. Purchase price of the machine is:~ Purchase price Rp 55.000.000~ Transportation costs Rp 2.000.000~ Installation costs Rp 1.000.000~ Testing costs Rp 2.000.000

The amount of additional costs Rp 5.000.000Machine acquisition cost Rp 60.000.000

Unknow :

Cost of machine Rp 60.000.000

Residual value of Rp 8.000.000

Economic value 5 years

Tahun Jam KerjaUnit

Produksi2000 5.000 75.000

2001 6.200 110.000

2002 6.800 155.000

2003 5.800 100.000

2004 6.200 110.000Jumlah 30.000 550.000

Machine depreciation of year :

a. Year depreciation 2010 =75.000550.00

x (60.000 .000−8.000.000) = Rp 7.090.909

=2

12x7.090 .909 = Rp 1.181.818

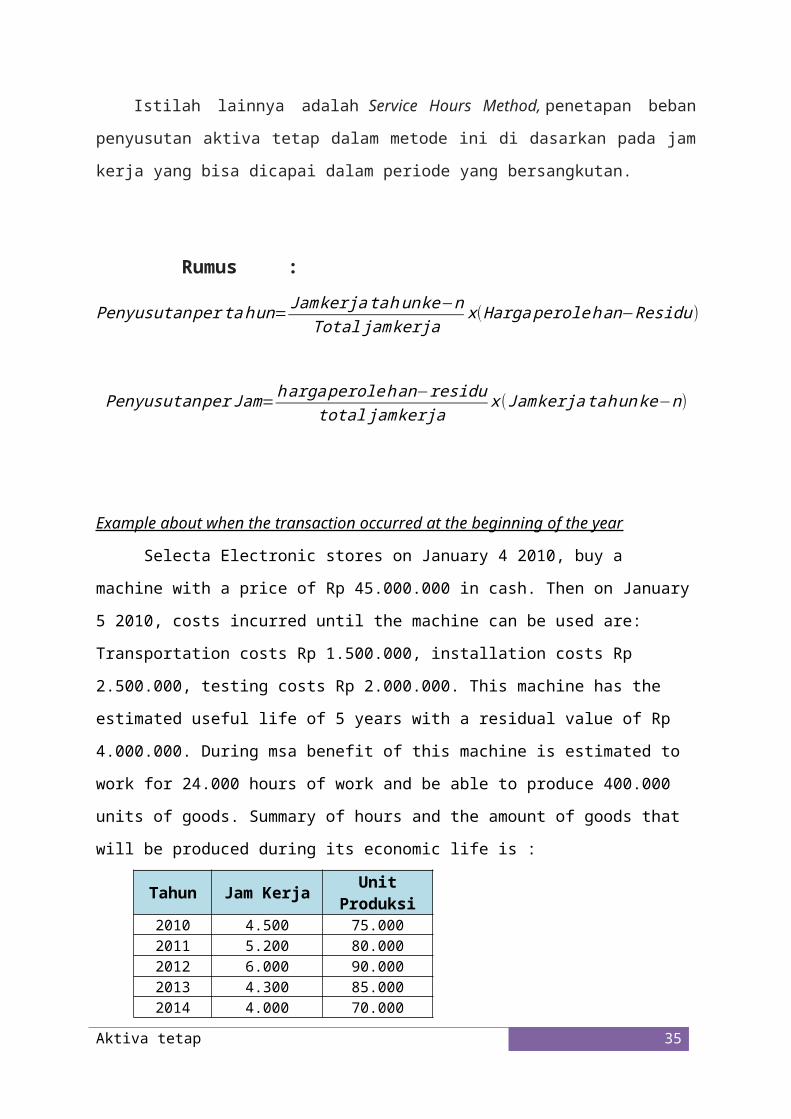

5. Metode Jam Kerja ( Methods of Working

Hours )

Istilah lainnya adalah Service Hours Method, penetapan beban penyusutan aktiva tetap

dalam metode ini di dasarkan pada jam kerja yang bisa dicapai dalam periode yang

bersangkutan.

Rumus :

Penyusutan per tah un= Jam kerjata h un ke−nTotal jam kerja

x (Harga peroleh an−Residu)

Penyusutan per Jam=h arga perolehan−residutotal jam kerja

x (Jam kerja tah un ke−n)

Example about when the transaction occurred at the beginning of the year

Selecta Electronic stores on January 4 2010, buy a machine with a price of Rp

45.000.000 in cash. Then on January 5 2010, costs incurred until the machine can be used

are: Transportation costs Rp 1.500.000, installation costs Rp 2.500.000, testing costs Rp

2.000.000. This machine has the estimated useful life of 5 years with a residual value of Rp

4.000.000. During msa benefit of this machine is estimated to work for 24.000 hours of work

and be able to produce 400.000 units of goods. Summary of hours and the amount of goods

that will be produced during its economic life is :

Tahun Jam KerjaUnit

Produksi2010 4.500 75.000

Aktiva tetap 28

2011 5.200 80.0002012 6.000 90.0002013 4.300 85.0002014 4.000 70.000

Jumlah 24.000 400.000

Requested :

a. Calculate depreciation of the year

b. Make a chart of depreciation using the Method of working hours

Completion :

Aktiva tetap 29

a. Purchase price of the machine is:~ Purchase price Rp 45.000.000~ Transportation costs Rp 1.500.000~ Installation costs Rp 2.500.000~ Testing costs Rp 1.000.000

The amount of additional costs Rp 5.000.000Machine acquisition cost Rp 50.000.000

Unknow :

Cost of machine Rp 50.000.000

Residual value of Rp 4.000.000

Economic value 5 years

Tahun Jam KerjaUnit

Produksi2010 4.500 75.0002011 5.200 80.0002012 6.000 90.0002013 4.300 85.0002014 4.000 70.000

Jumlah 24.000 400.000

Machine depreciation of year :

a. Year depreciation 2010=4.500

24.000x (50.000 .000−4.000 .000) = Rp 8.625.000

b. Year depreciation 2011=5.200

24.000x 46.000 .000 = Rp 9.966.667

c. Year depreciation 2012=6.000

24.000x 46.000 .000 = Rp 11.500.000

d. Year depreciation 2013=4.300

24.000x 46.000 .000 = Rp 8.241.667

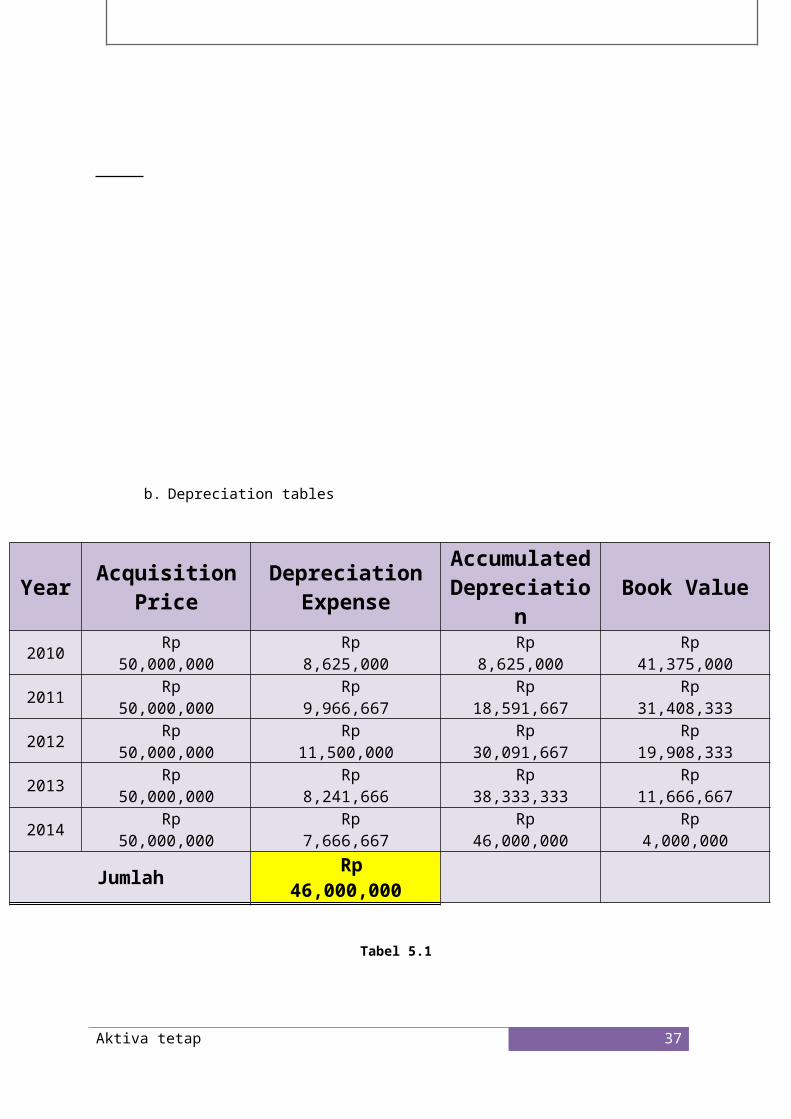

b. Depreciation tables

Year Acquisition Price

Depreciation Expense

Accumulated

Depreciation

Book Value

2010 Rp 50,000,000 Rp 8,625,000 Rp 8,625,000 Rp 41,375,000

2011 Rp 50,000,000 Rp 9,966,667 Rp 18,591,667 Rp 31,408,333

2012 Rp 50,000,000 Rp 11,500,000 Rp 30,091,667 Rp 19,908,333

2013 Rp 50,000,000 Rp 8,241,666 Rp 38,333,333 Rp 11,666,667

2014 Rp 50,000,000 Rp 7,666,667 Rp 46,000,000 Rp 4,000,000

Jumlah Rp

46,000,000

Tabel 5.1

Aktiva tetap 30

a. Purchase price of the machine is:~ Purchase price Rp 45.000.000~ Transportation costs Rp 1.500.000~ Installation costs Rp 2.500.000~ Testing costs Rp 1.000.000

The amount of additional costs Rp 5.000.000Machine acquisition cost Rp 50.000.000

Unknow :

Cost of machine Rp 50.000.000

Residual value of Rp 4.000.000

Economic value 5 years

Tahun Jam KerjaUnit

Produksi2010 4.500 75.0002011 5.200 80.0002012 6.000 90.0002013 4.300 85.0002014 4.000 70.000

Jumlah 24.000 400.000

Machine depreciation of year :

a. Year depreciation 2010=4.500

24.000x (50.000 .000−4.000 .000) = Rp 8.625.000

b. Year depreciation 2011=5.200

24.000x 46.000 .000 = Rp 9.966.667

c. Year depreciation 2012=6.000

24.000x 46.000 .000 = Rp 11.500.000

d. Year depreciation 2013=4.300

24.000x 46.000 .000 = Rp 8.241.667

Example question if the transaction occurred in the mid

Dated October 29, 2000 at Selecta Electronic Stores purchase a vehicle at a price of

Rp 55.000.000 in cash. Then on October 30, 2000 incurred costs can be used till the vehicle

is; transportation costs Rp 2.000.000; Installation costs Rp 1.000.000 and Rp 2.000.000 cost

trials. This machine has the estimated useful life of 5 years with a residual value of Rp

8.000.000. Over the estimated useful life of the machine is able to work for 30.000 hours of

work and be able to produce 550.000 units of goods. Brief working hours and the amount of

goods produced during its economic life is :

Tahun Jam KerjaUnit

Produksi

2000 5.000 75.000

2001 6.200 110.000

2002 6.800 155.000

2003 5.800 100.000

2004 6.200 110.000

Jumlah 30.000 550.000

Requested :

a. Calculate depreciation of the year

b. Make a chart of depreciation using the Method of working hours

Aktiva tetap 31

Completion :

Aktiva tetap 32

a. Purchase price of the machine is:~ Purchase price Rp 55.000.000~ Transportation costs Rp 2.000.000~ Installation costs Rp 1.000.000~ Testing costs Rp 2.000.000

The amount of additional costs Rp 5.000.000Machine acquisition cost Rp 60.000.000

Unknow :

Cost of machine Rp 60.000.000

Residual value of Rp 8.000.000

Economic value 5 years

Tahun Jam KerjaUnit

Produksi2000 5.000 75.000

2001 6.200 110.000

2002 6.800 155.000

2003 5.800 100.000

2004 6.200 110.000Jumlah 30.000 550.000

Machine depreciation of year :

a. Year depreciation 2010 =5.00030.00

x (60.000 .000−8.000.000) = Rp 8.666.667

=2

12x8.666 .667 = Rp 1.444.445

b. Year depreciation 2011 =6.200

30.000x52.000 .000 = Rp 10.746.667

c. Year depreciation 2012 =6.800

30.000x52.000 .000 = Rp 11.786.667

d. Year depreciation 2013 =5.800

30.000x52.000 .000 = Rp 10.053.333

b. Depreciation tables

Year Acquisition Price

Depreciation Expense

Accumulated

Depreciation

Book Value

2010 Rp 60,000,000 Rp 1,444,445 Rp 1,444,445 Rp 58,555,555

2011 Rp 60,000,000 Rp 10,746,666 Rp 12,191,111 Rp 47,808,889

2012 Rp 60,000,000 Rp 11,786,666 Rp 23,977,777 Rp 36,022,223

2013 Rp 60,000,000 Rp 10,053,333 Rp 34,031,110 Rp 25,968,890

2014 Rp 60,000,000 Rp 10,746,667 Rp 44,777,777 Rp 15,222,223

Oct 2015 Rp 60,000,000 Rp 7,222,223 Rp 52,000,000 Rp 8,000,000

Jumlah Rp

52,000,000

Tabel 5.2

Aktiva tetap 33

a. Purchase price of the machine is:~ Purchase price Rp 55.000.000~ Transportation costs Rp 2.000.000~ Installation costs Rp 1.000.000~ Testing costs Rp 2.000.000

The amount of additional costs Rp 5.000.000Machine acquisition cost Rp 60.000.000

Unknow :

Cost of machine Rp 60.000.000

Residual value of Rp 8.000.000

Economic value 5 years

Tahun Jam KerjaUnit

Produksi2000 5.000 75.000

2001 6.200 110.000

2002 6.800 155.000

2003 5.800 100.000

2004 6.200 110.000Jumlah 30.000 550.000

Machine depreciation of year :

a. Year depreciation 2010 =5.00030.00

x (60.000 .000−8.000.000) = Rp 8.666.667

=2

12x8.666 .667 = Rp 1.444.445

b. Year depreciation 2011 =6.200

30.000x52.000 .000 = Rp 10.746.667

c. Year depreciation 2012 =6.800

30.000x52.000 .000 = Rp 11.786.667

d. Year depreciation 2013 =5.800

30.000x52.000 .000 = Rp 10.053.333

Penghentian Pemakaian Aktiva

TetapAktiva tetap yang sudah kurang bermanfaat lagi karena habis umur ekonomisnya atau

tidak layak lagi untuk dipakai terus karena sudah ketinggalan jaman dengan munculnya

mesin-mesin baru yang dapat memproduksi barang yang mutunya lebih baik, lebih

menghemat biaya dan kapasitasnya lebih tinggi, maka aktiva kama tersebut harus dihentikan

pemakaiannya.

Jika suatu aktiva tetap sudah tidak dipakai lagi, untuk menghentikan pemakaian aktiva

tersebut dapat dilakukan dengan cara : dibuang, dijual, atau ditukarkan dengan aktiva yang

baru

1. Dibuang/disingkirkan

Dengan dibuangnya aktiva tetap berarti aktiva tersebut harus dikrluarkan dari

pembukuan, dengan jurnal:

a. Jika sudah habis umur ekonomisnya :

Akumulasi penyusutan mesin X Rp xxx

Mesin X Rp xxx

b. Jika belum habis umur akonomisnya :

Akumulasi penyusutan mesin X Rp xxx

Rugi karena penjualan Rp xxx

Mesin X Rp xxx

Aktiva tetap 34

Example :

A machine with a cost of Rp 80,000,000 heavily damaged and should be discontinued

its use of accumulated depreciation amounted to Rp 75,000,000. The cost for the transfer of

Rp 2,500,000

Requested :

Make the journal termination of fixed assets

Completion :

Acquisition price Rp 80.000.000

Accumulated depreciation ( Rp 75.000.000 )

Loss Rp 5.000.000

Transport costs Rp 2.500.000

Jurnal

Accumulated depreciation Rp 75.000.000

Loss Rp 7.500.000

Machine Rp 82.500.000

Aktiva tetap 35

2. Dijual

Dalam penjualan aktiva tetap memungkinkan timbulnya laba atau rugi

a. Jika timbul laba, dicatat dengan jurnal:

Kas Rp xxx

Akumulasi penyusutan mesin X Rp xxx

Laba penjualan aktiva tetap Rp xxx

Mesi X Rp xxx

b. Jika rugi, dicatat dengan jurnal:

Kas Rp xxx

Akumulasi penyusutan mesin X Rp xxx

Rugi penjualan aktiva tetap Rp xxx

Mesin X Rp xxx

Aktiva tetap 36

Example :

A transport vehicle cost Rp 150.000.000, depreciated Rp 40.000.000. On January 5,

2011 sale date cash at a price of Rp 135.000.000

Requested :

Make the journal termination of fixed assets

Completion :

Sale price Rp 135.000.000

Acquisition price Rp 150.000.000

Accumulation ( Rp 40.000.000 )

Book Value Rp 110.000.000

Gain on sales Rp 25.000.000

Jurnal :Kas Rp 135.000.000

Akumulasi penyusutan Rp 40.000.000

Laba penjualan aktiva tetap Rp 25.000.000

Mesin Rp 150.000.000

3. Ditukar dengan mesin/aktiva tetap yang baru (tukar-tambah)

Dalam pertukaran memungkinkan timbulnya lab atau rugi atas pertukaran.

Aktiva tetap 37

a. Apabila aktiva tetap ditukar dengan aktiva tetap yang sejenis, maka laba atas

pertukaran tidak diakui, sedangkan jika rugi atas pertukaran tersebut harus diakui

(prinsip konservatisme)

b. Apabila aktiva tetap ditukarkan dengan akytiva tetap lain yang tidak sejenis, maka

laba atau rugi atas pertukaran diakui

a) Ditukarsejenis

Example :

Amachinewas purchased inJanuary 2010for Rp144.000.000. Andup toDecember 31,

2012have beendepreciatedRp37.000.000. At thedate ofJanuary 8, 2013exchanged fora

newmachinewith theprice ofRp190.000.000.

Requested :

o Calculate theprofit or lossonthe exchange, iftheexchangeis :

a. Addingcash Rp85.000.000

b. Adding Cash Rp75.000.000

o makejournal

Answer :

Calculating Profit and Loss For exchanges

Purchase price of new machine Rp190.000.000

Buy price of old machine Rp144.000.000

Accumulated Depreciation ( Rp 37.000.000 )

Value of the old machine ( Rp107.000.000 )

Difference between the new value Rp 83.000.000

a. Adding Cash Rp85.000.000

Aktiva tetap 38

Difference betweenthe new value Rp83.000.000

Additionalcash ( Rp85.000.000 )

Loss Rp 2.000.000

Journal :

Machine( new ) Rp190.000.000

Accumulated Depreciation Rp 37.000.000

Loss Rp 2.000.000

Machines( Old ) Rp144.000.000

Cash Rp85.000.000

b. Adding Cash Rp75.000.000

Difference betweenthe new value Rp83.000.000

Additionalcash ( Rp75.000.000 )

Profit Rp 8.000.000

Journal :

Machine(new) Rp182.000.000

Accumulated Depreciation Rp 37.000.000

Machines(Old ) Rp144.000.000

Cash Rp 75.000.000

Aktiva tetap 39

Catatan :

Padapenambahanuangtunaisebesar Rp75.000.000 dinyatakansebagailaba

Namundalamprinsipkoservatismelabatidak di akui, makadariitulaba

Yang diperolehdikurangkanhargamesinbaru

( Rp190.000.000 - Rp8.000.000 = Rp182.000.000 )

b) Ditukartidaksejenis

Example :

A kind of a car with an acquisition cost Rp120.000.000

Rp60.000.000 has been depreciated. At the date of January 5, 2011 exchanged with a vehicle

type B at a price of Rp190.000.000. Keep a journal if the exchange :

a. Adding cash Rp135.000.000

b. Adding cash Rp125.000.000

Answer :

Calculating Profit and Loss For exchanges

Purchase price of new machine Rp190.000.000

Buy price of old machine Rp120.000.000

Accumulated Depreciation ( Rp 60.000.000 )

Value of the old machine ( Rp 60.000.000 )

Difference between the new value Rp130.000.000

a. Adding Cash Rp135.000.000

Aktiva tetap 40

Difference betweenthe new value Rp130.000.000

Additionalcash ( Rp135.000.000 )

Loss Rp 5.000.000

Journal :

Vehicle ( A ) Rp190.000.000

Accumulated Depreciation Rp60.000.000

Loss Rp 5.000.000

Vehicle ( B ) Rp120.000.000

Cash Rp135.000.000

b. Adding Cash Rp125.000.000

Difference betweenthe new value Rp130.000.000

Additionalcash ( Rp125.000.000 )

Profit Rp 5.000.000

Journal :

Vehicle ( A ) Rp190.000.000

Accumulated Depreciation Rp 60.000.000

Vehicle ( B ) Rp120.000.000

Cash Rp125.000.000

Profit Rp 5.000.000

Aktiva tetap 41

Catatan:

Pada pertukaran aktiva tetap tidak sejenis, laba atau pun rugi harus ditulis.

Aktiva tetap 42