jakarta, november 2014 - indocement.co.id · laporan keuangan 2010 rencana strategi investasi...

TRANSCRIPT

Jakarta, November 2014

1

AGENDA

Sekilas Indocement

Kondisi Pasar Semen Domestik Saat ini

Laporan Keuangan 2010

Rencana Strategi Investasi

Tinjauan 2011

General Information about Indocement

Current Domestic Market Condition

Financial Update Q3 2014

Investment Plan Strategy

Outlook 2014

Q & A

2

AGENDA

Sekilas Indocement

Current Domestic Market Condition

Financial Update Q3 2014

Investment Plan Strategy

Outlook 2014

Q & A

General Information about Indocement

3

INDOCEMENT HISTORY 1985

PT Indocement Tunggal Prakarsa (“Indocement”) incorporated

following merger of 6 companies owning 8 cement plants

1989 Public listed of Indocement in the Indonesia Stock Exchange

1991

Acquired the 9th plant in Palimanan

Completed Surabaya cement terminal

Started ready-mix concrete business

1996-1999 Completed the 10th in Palimanan and 11th plants in Citeureup

2001 HeidelbergCement Group became a major shareholder through

its subsidiary Kimmeridge Enterprise Pte. Ltd.

2003 Kimmeridge Enterprise Pte. Ltd. transferred shares in Indocement

to HC Indocement GmbH

2005 Introduced Portland Composite Cement (“PCC”) product to

Indonesian market

2006 HC SE Asia GmbH, was merged into HeidelbergCement AG

which then controlled 65.14% shares of Indocement

2007

Acquisition of 51% stake in PT Gunung Tua Mandiri

Completed modification of the 8th plant which provided an

additional annual capacity of 600,000 tons of cements

2009 Placement of 14.1% Heidelbergcement’s Shares in June 2009

Acquired 12th Plant via merger with PT Indo Kodeco Cement 2000

2010

Additional capacity of 1.5 mt cement mills capacity by August

2010 in Cirebon Factory

2013

On March 25, 2013, the Company has signed the agreement

concerning the equipment supply and engineering with Tianjin Cement Industry Design & Research Institute Co,.Ltd. as part of the construction of a new brownfield project with the capacity of 4.4 mt in Citeureup

Acquisition of PT Tarabatuh Manunggal

4

INDOCEMENT TODAY Leading Indonesian producer of quality & specialty cement products

• 2nd largest cement manufacturer in Indonesia, listed on the Indonesia

Stock Exchange

• Integrated cement operations with a total current production capacity of

20.5mn tons

• Diversified product range including

• PCC, Portland Cement I, II and V, Oil Well Cement, and

• The one and only White Cement producer in Indonesia to date

• One of the world largest cement producer HeidelbergCement Group is

the majority & controlling shareholder – 51%, Salim – 13% and Public –

36%

• As of August 29, 2014 Indocement’s Market capitalization

approximately at IDR 89.2 T (IDR 24,250/share) - one of the largest in

IDX

• As end of 2013, over 7,000 employees (Cement: 4,946 employees;

Ready-Mix & Aggregates: 2,614 Employees)

• Well established “Tiga Roda” brand

5

BOARD OF COMMISSIONERS & BOARD OF DIRECTORS

Board of

Commissioners

Dr. Albert Scheuer

President

Commissioner

Dr. Lorenz Naeger

Commissioner

Daniel Gauthier

Commissioner

Tedy Djuhar

VP Commissioner,

Independent

Commissioner

I Nyoman Tjager

VP Commissioner,

Independent

Commissioner

Dr. Bernd Scheifele

Commissioner

Board of Directors

Kuky Permana

Independent

Director

Franciscus

Welirang

VP Director

Hasan Imer

Director

Ramakanta

Bhattacharjee

Director

Daniel K. Adam

Director

Daniel Fritz

Director

Christian

Kartawijaya

President Director

Benny S.Santoso

Director

M. Jusuf Hamka

Independent

Commissioner

Tju Lie Sukanto

Director

6

INDOCEMENT’S BUSINESS DIVISIONS Cement is the core division comprising over 90% of sales

INDOCEMENT

Cement RMC Others

Citeureup Factory

- 9 plants

Palimanan Factory

- 2 plants

Tarjun Factory - 1

plant

PT Pionirbeton Industri

and PT Indomix

Perkasa* – 40 batching

plants in Jabodetabek,

West Java, and Central

Java – capacity more

than 4.0 mio m3.

PT Dian Abadi Perkasa –

99.9% (Cement Trading)

PT Multi Bangun Galaxy –

99.9% (Terminal-Land

Operation)

PT Pama Indo Mining - 40%

(Mining Services in Tarjun)

PT Bahana Indonor - 100%

(Owns & operates one ship

& one floating terminals)

PT Cibinong Center

Industrial Estate - 50%

(Industrial Estate in

Citeureup)

PT Mineral Industry

Sukabumi

100% (Trass Quarry)

AGGREGATES

PT Mandiri Sentra

Sejahtera – 100%

(Aggregates Business)

PT Tarabatuh

Manunggal – 100%

(Aggregates Business)

7

INDOCEMENT FACTORY AND TERMINAL LOCATIONS

Citeureup Factory

9 plants with

production capacity

of 13.8mt

Tj. Priok Terminal

Palimanan Factory

2 plants with production

capacity of 4.1mt

Surabaya Terminal

Lombok Terminal

Tarjun Factory

1 plant with production

capacity of 2.6mt

One of the largest integrated factory complex in the world at Citeureup

State of the art technology with some of the most efficient kilns in operation today

Total current capacity is 20.5 mt of cement

Cement distribution using train for some locations

Banyuwangi Terminal

Samarinda Terminal

Denpasar

Terminal

8

AGENDA

General Information about Indocement

Current Domestic Market Condition

Financial Update Q3 2014

Investment Plan Strategy

Outlook 2014

Q & A

Current Domestic Market Condition

9

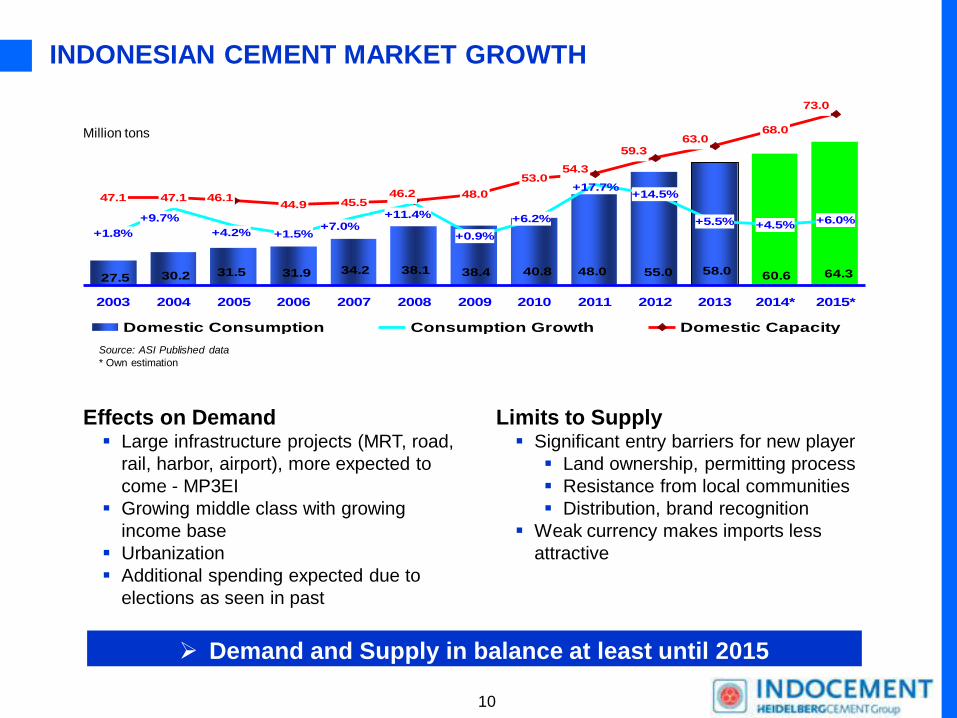

INDONESIAN CEMENT MARKET GROWTH

Source: ASI Published data

* Own estimation

Effects on Demand Large infrastructure projects (MRT, road,

rail, harbor, airport), more expected to

come - MP3EI

Growing middle class with growing

income base

Urbanization

Additional spending expected due to

elections as seen in past

Limits to Supply Significant entry barriers for new player

Land ownership, permitting process

Resistance from local communities

Distribution, brand recognition

Weak currency makes imports less

attractive

Demand and Supply in balance at least until 2015

40.827.5

31.5 31.9 34.2 38.1 38.430.2 64.360.658.055.048.0

+1.8% +1.5% +0.9%

+5.5% +4.5% +6.0%

+4.2%

+11.4%

+17.7%

+6.2%+9.7%+7.0%

+14.5%47.144.9 45.5

68.0

47.1

53.0

48.046.246.1

73.0

63.059.3

54.3

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014* 2015*

Domestic Consumption Consumption Growth Domestic Capacity

Million tons

10

CURRENT TRADING – September 2014 Indocement sales volumes comparison

9.6 mt10.0 mt10.7 mt

12.3 mt 11.8 mt12.8 mt

17.9 mt 18.0 mt

12.9 mt 13.2 mt

0.1 mt

15.4 mt

2.5 mt3.2 mt 3.8 mt

2.3 mt 1.6 mt 1.0 mt 0.6 mt 0.22 mt0.1 mt 0.18 mt

2005 2006 2007 2008 2009 2010 2011 2012 2013 Sep-13 Sep-14

Domestic Export

29.7%30.6% 30.9%

31.7%

30.2%30.9%

31.5%32.0%

30.4% 30.5% 30.2%

Market Share

YTD September 2014, Indocement’s domestic sales volume increase by 2.14% YoY

Export sales volume was decreased by 34% to 120.8 k tons (previous year: 183.1 k tons).

11

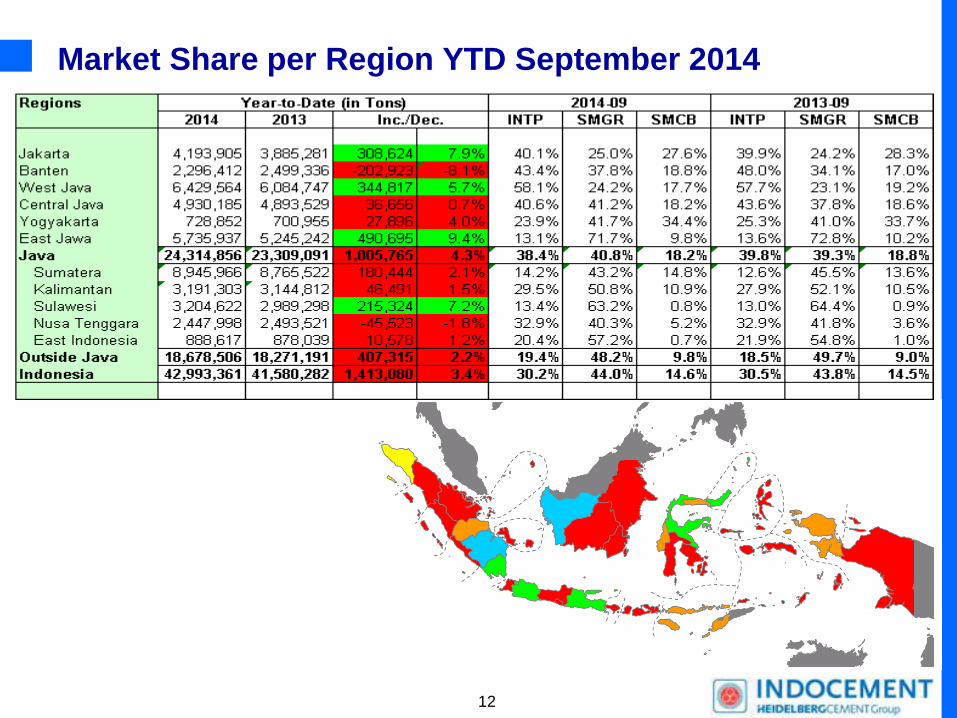

Market Share per Region YTD September 2014

12

AND THERE IS STILL MORE POTENTIAL

Source: Deutsche Bank

Indonesia cement consumption per capita increased by 60% from 143 kg/capita in 2005 to

229 kg/capita in 2013

Reached an all-time high but still one of the lowest cement consumption per capita

compared to its peers

Cement consumption per capita in 2013

Indonesia likely to catch up with its peers in the near future

1,774

1,116

554 493

229 207 210 143

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

CH* SG VN TH ID PH IN

kg/capita

ID

2005

13

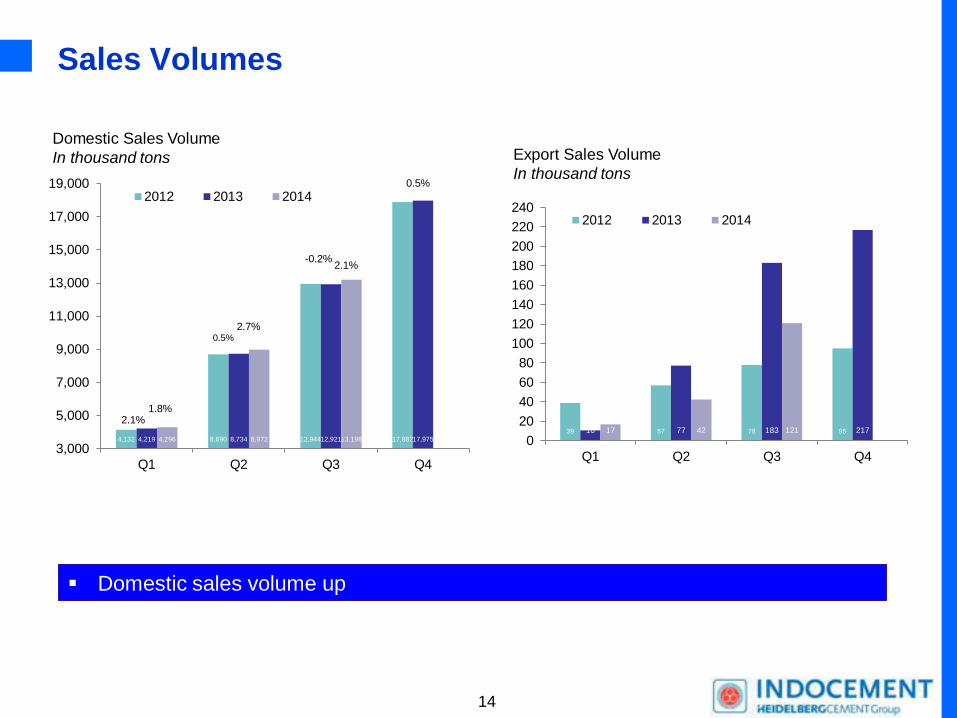

Sales Volumes

4,132 8,690 12,944 17,882 4,219 8,734 12,921 17,975 4,296 8,972 13,198

3,000

5,000

7,000

9,000

11,000

13,000

15,000

17,000

19,000

Q1 Q2 Q3 Q4

2012 2013 20140.5%

39 57 78 95 10 77 183 217 17 42 121

0

20

40

60

80

100

120

140

160

180

200

220

240

Q1 Q2 Q3 Q4

2012 2013 2014

Domestic Sales Volume

In thousand tons Export Sales Volume

In thousand tons

2.1%

0.5%

-0.2%

1.8%

2.7%

Domestic sales volume up

2.1%

14

AGENDA

General Information about Indocement

Current Domestic Market Condition

Financial Update 2010

Investment Plan Strategy

Outlook 2014

Q & A

Financial Update Q3 2014

15

Consolidated Income Statement

Q3 2014 Q3 2013 Change

IDR Bio IDR Bio %

Total Sales Volume (thousand tons) 13,318 13,104 1.6%

In Billion IDR

Net Revenues 14,166.9 13,348.0 6.1%

Cost of Revenues (7,819.2) (7,098.6) 10.2%

GROSS PROFIT 6,347.6 6,249.5 1.6%

% of Net Revenues 44.8% 46.8%

Operating Expenses (2,288.9) (1,902.7) 20.3%

Other Operating Income (Expenses) 75.7 82.6 -8.4%

OPERATING INCOME 4,134.5 4,429.4 -6.7%

% of Net Revenues 29.2% 33.2%

EBITDA 4,781.8 5,031.0 -5.0%

% of Net Revenues 33.8% 37.7%

Finance Income 613.2 341.4 79.6%

Equity in Net Earnings of Associated Companies - Net 17.2 12.3 39.6%

INCOME FOR THE PERIOD 3,719.4 3,609.1 3.1%

Other Comprehensive Income (Expenses) (88.0) 201.6 -143.7%

TOTAL COMPREHENSIVE INCOME FOR THE PERIOD 3,631.4 3,810.6 -4.7%

Description

16

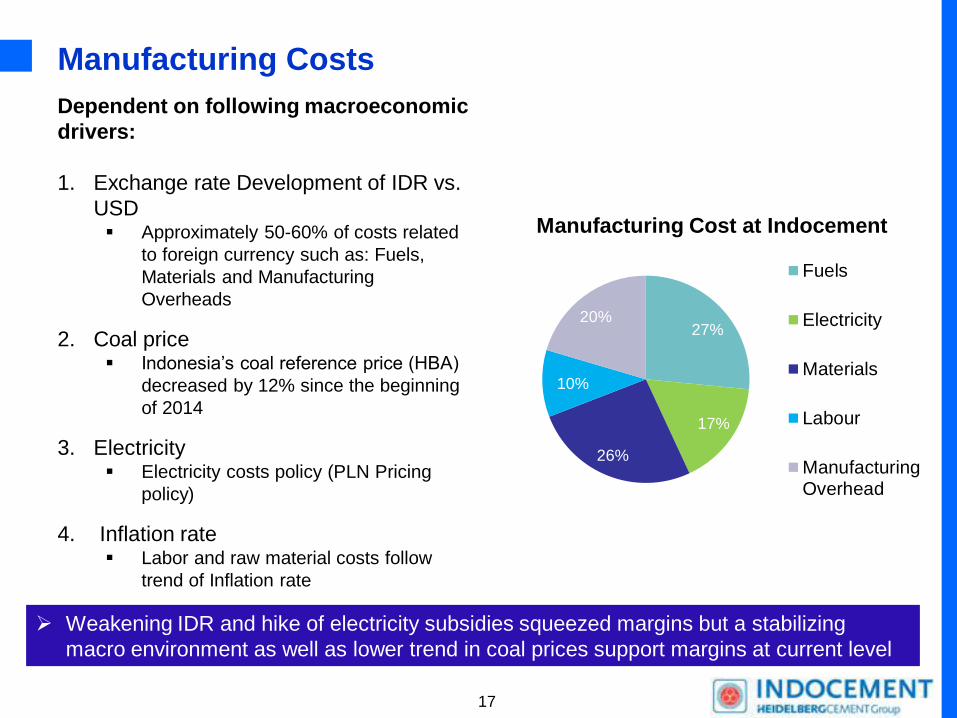

Manufacturing Costs

27%

17%

26%

10%

20%

Fuels

Electricity

Materials

Labour

ManufacturingOverhead

Dependent on following macroeconomic

drivers:

1. Exchange rate Development of IDR vs.

USD Approximately 50-60% of costs related

to foreign currency such as: Fuels,

Materials and Manufacturing

Overheads

2. Coal price Indonesia’s coal reference price (HBA)

decreased by 12% since the beginning

of 2014

3. Electricity Electricity costs policy (PLN Pricing

policy)

4. Inflation rate Labor and raw material costs follow

trend of Inflation rate

Manufacturing Cost at Indocement

Weakening IDR and hike of electricity subsidies squeezed margins but a stabilizing

macro environment as well as lower trend in coal prices support margins at current level

17

Operational efficiency improvements

New vertical raw mill

Capacity: 1.9m tons

In operation since May

Lower energy consumption compared to other

mills

Lower clinker ratio possible due to distinct

technical specifications of the VRM

Capable to grind the slag in significant amount

Slag contract with Posco + Indoferro

Replacement for clinker in cement production, hence lower clinker

ratio

1

2

This will help to further enhance margins

18

AGENDA

General Information about Indocement

Current Domestic Market Condition

Financial Update Q3 2014

Investment Plan Strategy

Outlook 2014

Q & A

Investment Plan Strategy

19

Projects

New cement mill with capacity of 1.9 MT in Citeureup which is in

operation in Q2 2014

1 brownfield project with capacity of 4.4 million tons with an overall

investment value of IDR 5.5 to 6.5 trillion

2 greenfield projects with capacity of 2.5 million tons, one in Central

Java and one outside Java

CAPACITY EXPANSION TO PARTICIPATE IN INDUSTRY GROWTH

16.6 3017.1 18.6 20.6 25

2005 2007 2010 2014 2015/2016 2017/2020

Million Tons

+ 0.6 mt + 1.5 mt

+ 1.9 mt + 4.4 mt

+ 5 mt

Strategically well positioned to capitalize on further demand

20

Potential Capacity Increase

Citeureup

2014: 13.8m tons

2015: Brownfield 4.4m tons

Investment: USD 150/ton

Cirebon

2014: 4.1m tons Central Java

2018: Greenfield 2.5-3m tons

Investment: 200-250 USD/ton

Tarjun

2014: 2.6m tons

North Sumatra

2018: Greenfield 2.5-3m tons

Investment: 200-250 USD/ton

21

READY-MIX CONCRETE EXPANSION

• Indocement keeps strengthening its ready-mix concrete in

order to meet the increase of demand in ready mix concrete

for the construction of residential and high rise building in

Jakarta and West Java area by heavily investing in new

batching plants and mixer trucks. This has brought some

contribution to gain more market share.

• Following the rising trend of cement demand and increased

capacity, the sales volume of ready-mix business growth

significantly in the last 2 years.

• The 2013 sales volume has increased around 26%

• Ytd September 2014 sales volume decreased by 11% YoY

due to slowing down of construction activities across nation.

• One of the market leader in RMC business

800630 683

930 9561,221

2,429

4,430

3,209

2,860

3,517

100

400700

1,0001,300

1,6001,900

2,2002,500

2,800

3,1003,400

3,7004,000

4,3004,600

4,900

20052006

20072008

20092010

20112012

2013

Sep-13

Sep-14

000m3

22

AGENDA

General Information about Indocement

Current Domestic Market Condition

Financial Update Q3 2014

Investment Plan Strategy

Outlook 2011

Q & A

Outlook 2014

23

Outlook for Year-end 2014

Market Environment

• National market 2014 still estimated to grow about 4~5%

• Infrastructure projects expected to pick-up with the election of the new

government

• Changing market environment as new competitors are entering the market

• Hike in electricity costs will hamper the margin of each cement factory in

Indonesia so there is a common need to pass through such costs in near future

Indocement Outlook

Further focus on margin improvement

Will run with the most efficient kilns in operation (P10 & P11 back to their

normal operation from May 2014, after had their major overhaul and stoppage)

Recapture market share while keeping the efforts to pass through the cost

increase to the market if possible

Proceeding with planned capacity expansion projects

24

AGENDA

General Information about Indocement

Current Domestic Market Condition

Financial Update Q3 2014

Investment Plan Strategy

Outlook 2011

Q & A

Outlook 2014

25

Thank you

26