chapter 16 - planning the firm’s financing mix

DESCRIPTION

Chapter 16 - Planning the Firm’s Financing Mix. Chapter 17 – Dividend Policy and International Financing. Tujuan Pembelajaran 1. Mahasiswa mampu untuk : Menjelaskan konsep struktur modal yang optimal Menjelaskan inti dari teori struktur modal - PowerPoint PPT PresentationTRANSCRIPT

1IIS

Chapter 16 - Planning the Firm’s Financing Mix

Chapter 17 – Dividend Policy and International Financing

2IIS

Tujuan Pembelajaran 1

Mahasiswa mampu untuk: Menjelaskan konsep struktur modal yang optimalMenjelaskan inti dari teori struktur modalMemasukkan konsep agency cost dan arus kas bebas dalam siskusi manajemen struktur modal Menggunakan alat dasar pengelolaan struktur modal

3IIS

Pokok Bahasan 1

Struktur keuangan dan struktur modalSekilas teori struktur modalAgency cost, arus kas bebas, dan struktur modalAlat dasar pengelolaan struktur modal

4IIS

Tujuan Pembelajaran 2

Mahasiswa mampu untuk: Menjelaskan untung rugi antara membayar dividen dan menahan laba di dalam perusahaanMenjelaskan hubungan antara kebijakan dividen terhadap harga sahamMenjelaskan pertimbangan praktis dalam kebijakan dividen Membedakan jenis–jenis kebijakan dividen yang seringkali digunakan Menjelaskan tujuan dan prosedur pembelian kembali saham

5IIS

Pokok Bahasan 2

Pembayaran dividen vs menahan labaApakah kebijakan dividen mempengaruhi harga saham?Kebijakan dividen dalam praktekProsedur pembayaran dividenDividen saham dan pemecaham sahamPembelian kembali saham

6IIS

Balance Sheet Current Current Assets Liabilities

Debt and Fixed Preferred Assets Shareholders’ Equity

FinancialStructure

7IIS

Balance Sheet Current Current Assets Liabilities

Debt and Fixed Preferred Assets Shareholders’ Equity

CapitalStructure

8IIS

Why is Capital Structure Important?

1) Leverage: Higher financial leverage means higher returns to stockholders, but higher risk due to fixed payments.

2) Cost of Capital: Each source of financing has a different cost. Capital structure affects the cost of capital.

The Optimal Capital Structure is the one that minimizes the firm’s cost of capital and maximizes firm value.

9IIS

What is the Optimal Capital Structure?

In a “perfect world” environment with no taxes, no transaction costs and perfectly efficient financial markets, capital structure does not matter.This is known as the Independence hypothesis: firm value is independent of capital structure.

10IIS

Independence Hypothesis

Firm value does not depend on capital structure.

11IIS

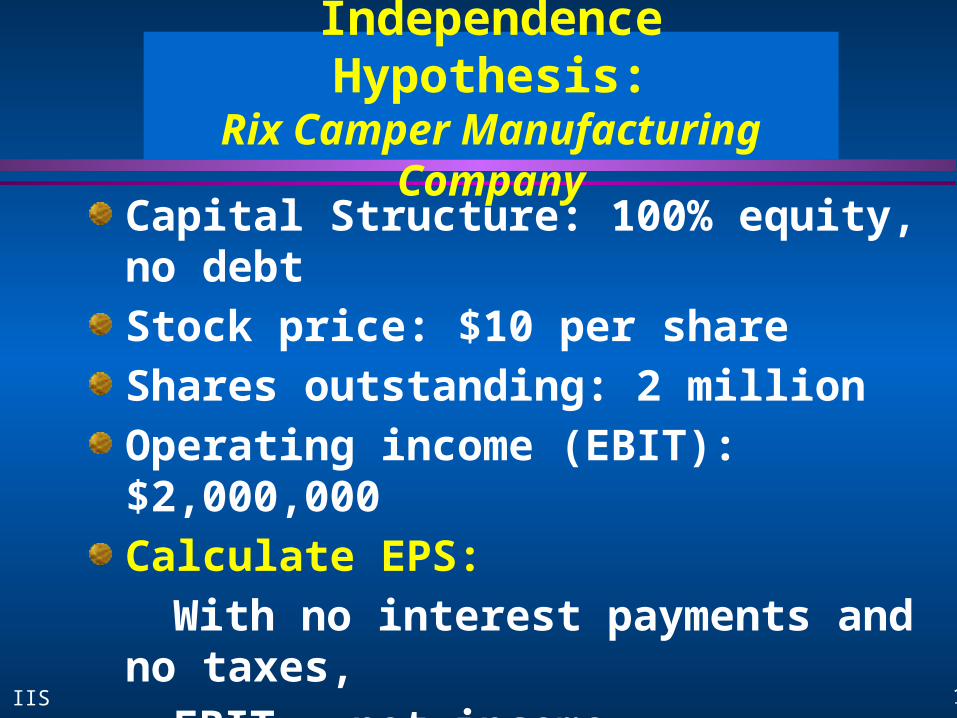

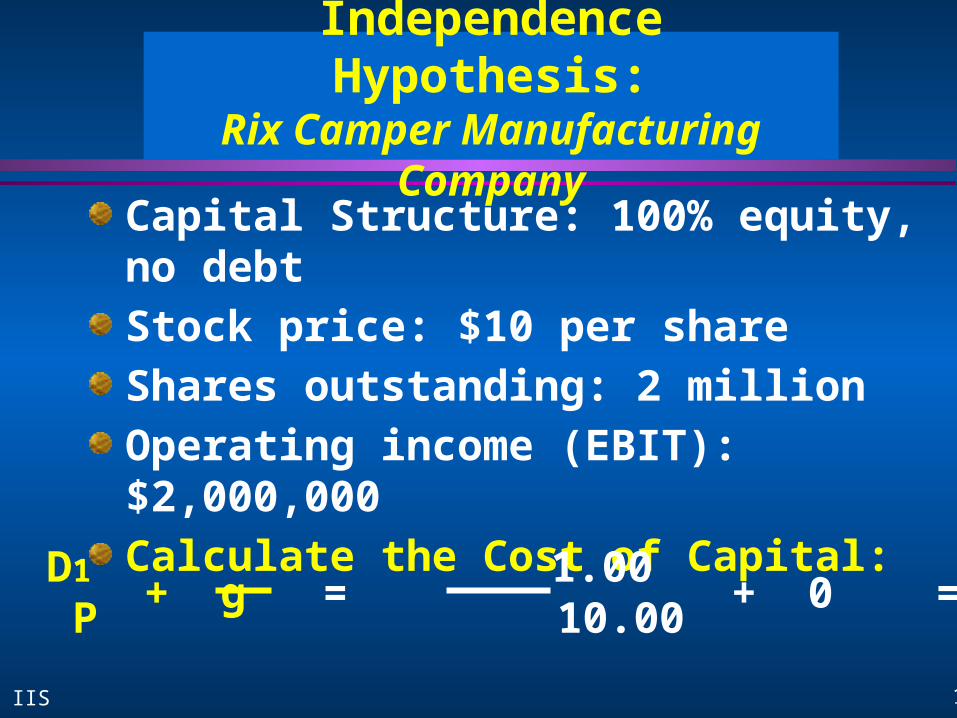

Independence Hypothesis:Rix Camper Manufacturing Company

Capital Structure: 100% equity, no debtStock price: $10 per shareShares outstanding: 2 millionOperating income (EBIT): $2,000,000Calculate EPS:

With no interest payments and no taxes,

EBIT = net income.$2,000,000/2,000,000 shares = $1.00

12IIS

Independence Hypothesis:Rix Camper Manufacturing Company

Capital Structure: 100% equity, no debtStock price: $10 per shareShares outstanding: 2 millionOperating income (EBIT): $2,000,000Calculate the Cost of Capital:

k = + g = + 0 = 10%D1 1.00 P 10.00

13IIS

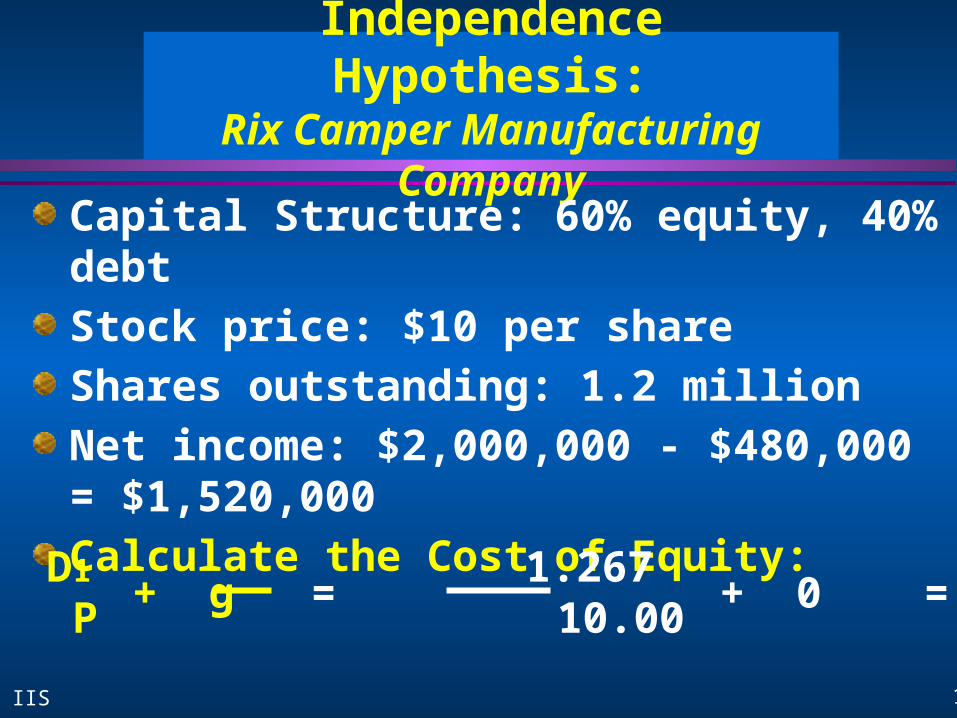

Independence Hypothesis:Rix Camper Manufacturing Company

$20 million capitalization$8 million in debt issued to retire $8 million in equity.Equity = $12m / $20m = 60%Debt = $8m / $20m = 40%Capital Structure: 60% equity, 40% debtShares outstanding: $12 million / $10 = 1,200,000 shares.Interest = $8m x .06 = $480,000

14IIS

Independence Hypothesis:Rix Camper Manufacturing Company

Capital Structure: 60% equity, 40% debtStock price: $10 per shareShares outstanding: 1.2 millionNet income: $2,000,000 - $480,000 = $1,520,000Calculate EPS:

$1,520,000/1,200,000 shares = $1.267

15IIS

Independence Hypothesis:Rix Camper Manufacturing Company

Capital Structure: 60% equity, 40% debtStock price: $10 per shareShares outstanding: 1.2 millionNet income: $2,000,000 - $480,000 = $1,520,000Calculate the Cost of Equity:

k = + g = + 0 = 12.67%D1 1.267 P 10.00

16IIS

Independence Hypothesis:Rix Camper Manufacturing Company

Capital Structure: 60% equity, 40% debtStock price: $10 per shareShares outstanding: 1.2 millionNet income: $2,000,000 - $480,000 = $1,520,000Calculate the Cost of Capital:

.6 (12.67%) + .4 (6%) = 10%

17IIS

Cost ofCapital

kc

0% debt Financial Leverage 100% debt

.

kc = cost of equitykd = cost of debtko = cost of capital

Independence Hypothesis

18IIS

Increasing leverage causesthe cost of equityto rise.

Independence Hypothesis

Cost ofCapital

kc

kd kd

0% debt Financial Leverage 100% debt

19IIS

Independence Hypothesis

Cost ofCapital

kc

kd

kc

kd

Increasing leverage causesthe cost of equityto rise.

What will be the net effect

on the overall cost of capital?

0% debt Financial Leverage 100% debt

20IIS

Independence Hypothesis

Cost ofCapital

kc

kd

kc

kd

Increasing leverage causesthe cost of equityto rise.

What will be the net effect

on the overall cost of capital?

0% debt Financial Leverage 100% debt

21IIS

kc

kd

Independence Hypothesis

Cost ofCapital

kc

kokd

0% debt Financial Leverage 100% debt

22IIS

Independence Hypothesis

If we have perfect capital markets, capital structure is irrelevant. In other words, changes in capital structure do not affect firm value.

23IIS

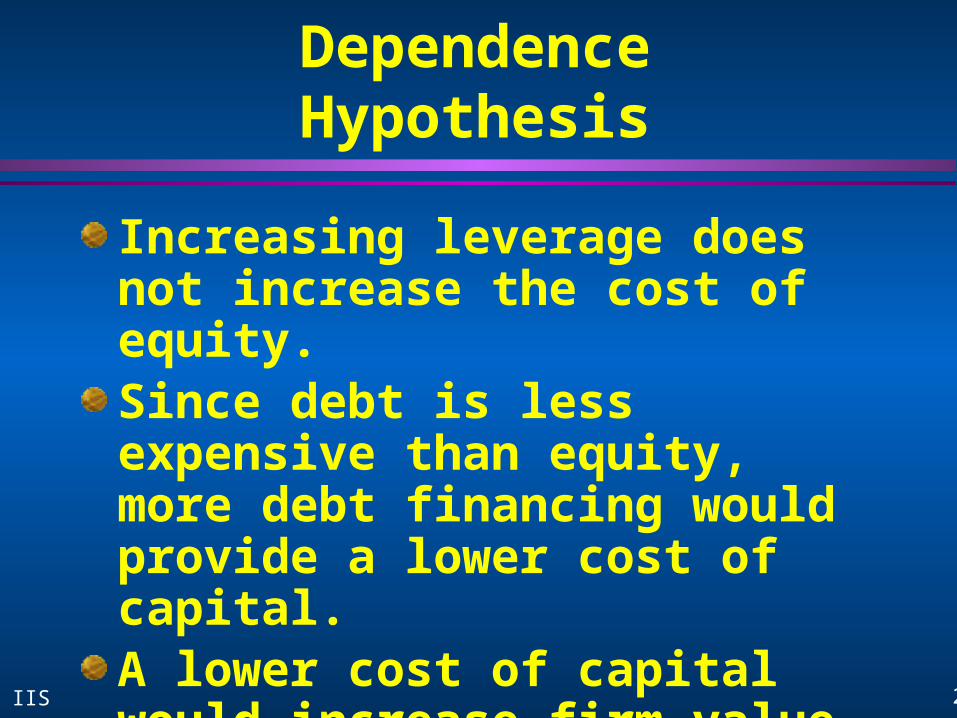

Dependence Hypothesis

Increasing leverage does not increase the cost of equity.Since debt is less expensive than equity, more debt financing would provide a lower cost of capital. A lower cost of capital would increase firm value.

24IIS

Dependence HypothesisSince the cost of debt is lowerthan the cost of equity…increasing leverage reduces thecost of capital.

Cost ofCapital

kc

kd

Financial Leverage

kc

kdko

25IIS

Moderate Position

The previous hypothesis examines capital structure in a “perfect market.”The moderate position examines capital structure under more realistic conditions.For example, what happens if we include corporate taxes?

26IIS

Rix Camper example:Tax effects of financing with debt

unlevered leveredEBIT 2,000,000 2,000,000- interest expense 0 (480,000)EBT 2,000,000

1,520,000- taxes (50%) (1,000,000)

(760,000)Earnings available to stockholders 1,000,000

760,000Payments to all securityholders 1,000,000 1,240,000

27IIS

Moderate Position

Cost ofCapital

kc

kd

Financial Leverage

kc

kd

becauseof the tax benefit

associated with debt financing.

Even if the cost of equity risesas leverage increases, the cost of debt is very low...

28IIS

Moderate Position

Cost ofCapital

kc

kd

Financial Leverage

kc

kd

The low cost of debt reduces the cost of capital.

ko

29IIS

Moderate Position

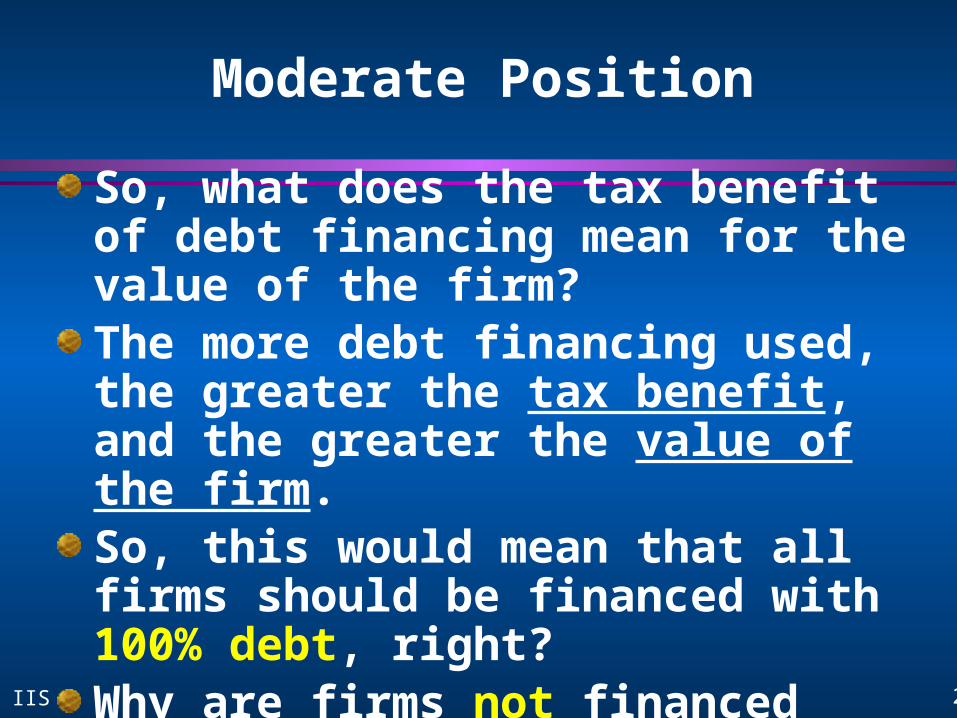

So, what does the tax benefit of debt financing mean for the value of the firm?The more debt financing used, the greater the tax benefit, and the greater the value of the firm.So, this would mean that all firms should be financed with 100% debt, right?Why are firms not financed with 100% debt?

30IIS

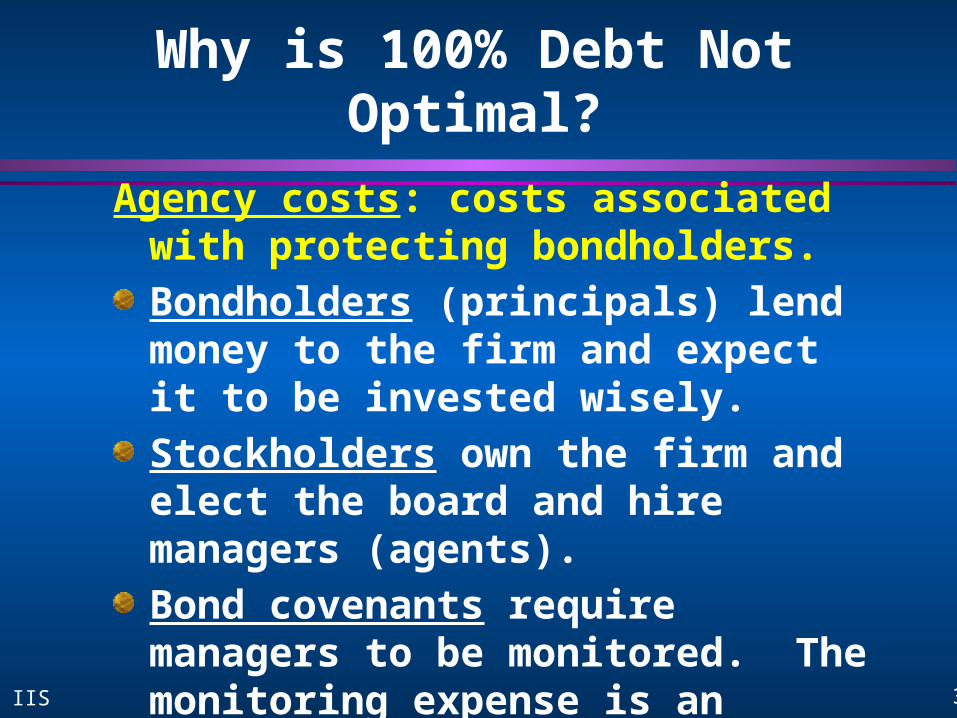

Why is 100% Debt Not Optimal?

Bankruptcy costs: costs of financial distress.Financing becomes difficult to get.Customers leave due to uncertainty.Possible restructuring or liquidation costs if bankruptcy occurs.

31IIS

Why is 100% Debt Not Optimal?

Agency costs: costs associated with protecting bondholders.Bondholders (principals) lend money to the firm and expect it to be invested wisely.Stockholders own the firm and elect the board and hire managers (agents).Bond covenants require managers to be monitored. The monitoring expense is an agency cost, which increases as debt increases.

32IIS

Cost ofCapital

Financial Leverage

kc

kd

kc

kd

Moderate Positionwith Bankruptcy and Agency Costs

33IIS

Cost ofCapital

Financial Leverage

kc

kd

kc

kd

If a firm borrows too much, thecosts of debt and equity will spike upward, due to bankruptcy costsand agency costs.

Moderate Positionwith Bankruptcy and Agency Costs

34IIS

Cost ofCapital

Financial Leverage

kc

kd

kc

kd

Moderate Positionwith Bankruptcy and Agency Costs

35IIS

Cost ofCapital

Financial Leverage

kc

kd

kc

kd

ko

Moderate Positionwith Bankruptcy and Agency Costs

36IIS

Cost ofCapital

Financial Leverage

kc

kd

kc

kd

ko

Ideally, a firm should use leverageto obtain their optimum capital structure, which will minimize thefirm’s cost of capital.

Moderate Positionwith Bankruptcy and Agency Costs

37IIS

Cost ofCapital

Financial Leverage

kc

kd

kc

kd

ko

Moderate Positionwith Bankruptcy and Agency Costs

38IIS

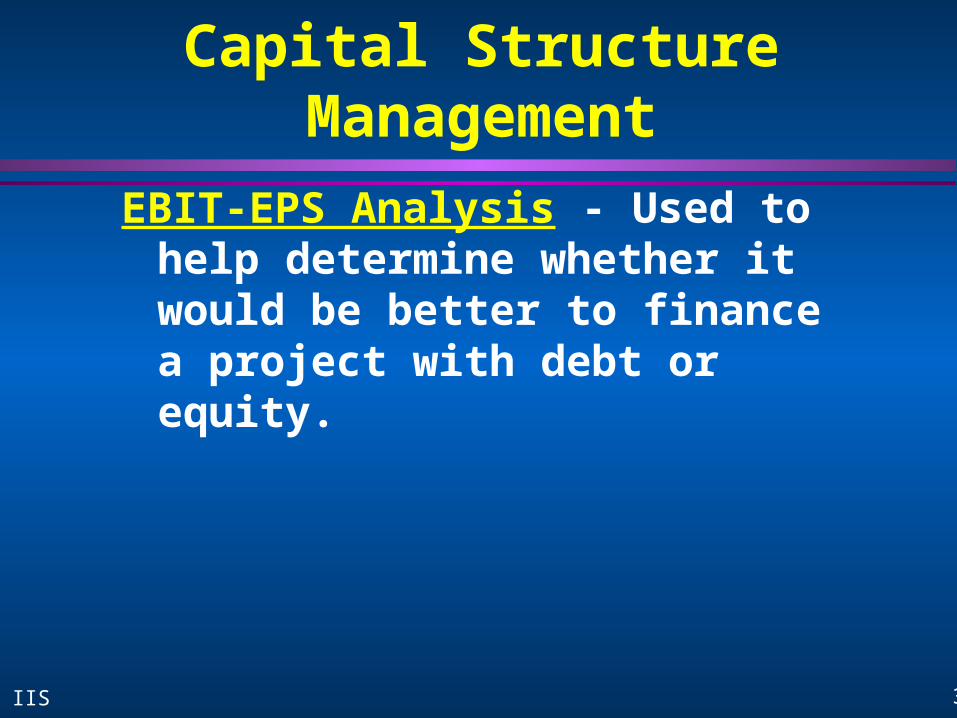

Capital Structure Management

EBIT-EPS Analysis - Used to help determine whether it would be better to finance a project with debt or equity.

39IIS

Capital Structure Management

EBIT-EPS Analysis - Used to help determine whether it would be better to finance a project with debt or equity.

EPS = (EBIT - I)(1 - t) - P S

I = interest expense, P = preferred dividends,S = number of shares of common stock outstanding.

40IIS

EBIT-EPS Example

Our firm has 800,000 shares of common stock outstanding, no debt, and a marginal tax rate of 40%. We need $6,000,000 to finance a proposed project. We are considering two options:Sell 200,000 shares of common stock at $30 per share,Borrow $6,000,000 by issuing 10% bonds.

41IIS

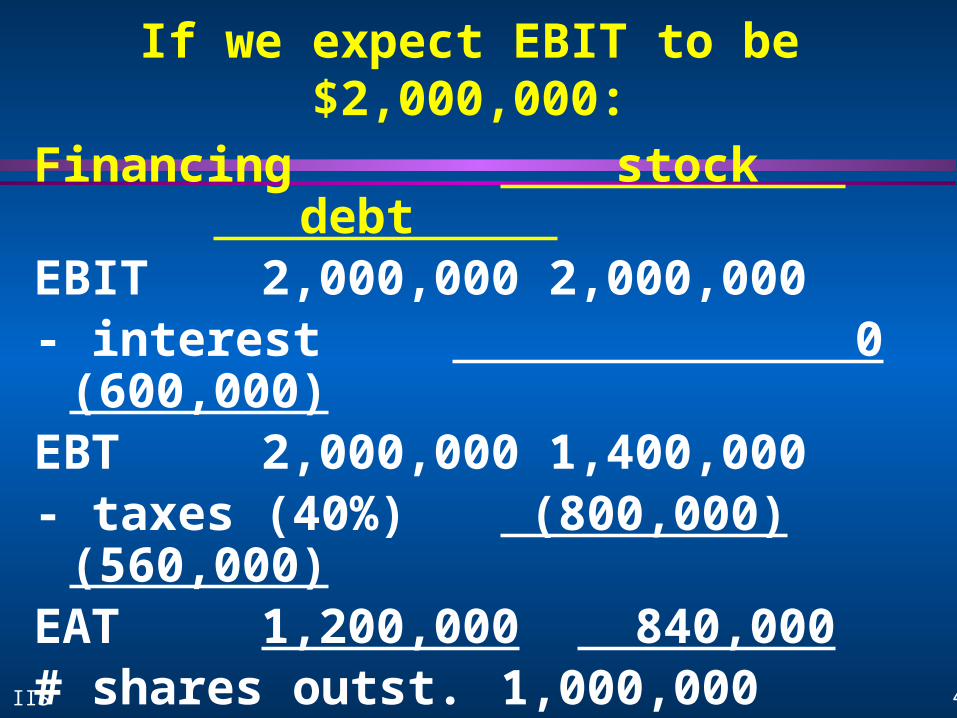

If we expect EBIT to be $2,000,000:

Financing stock debt EBIT 2,000,000 2,000,000- interest 0 (600,000)EBT 2,000,000 1,400,000- taxes (40%) (800,000) (560,000)EAT 1,200,000 840,000# shares outst. 1,000,000 800,000EPS $1.20 $1.05

42IIS

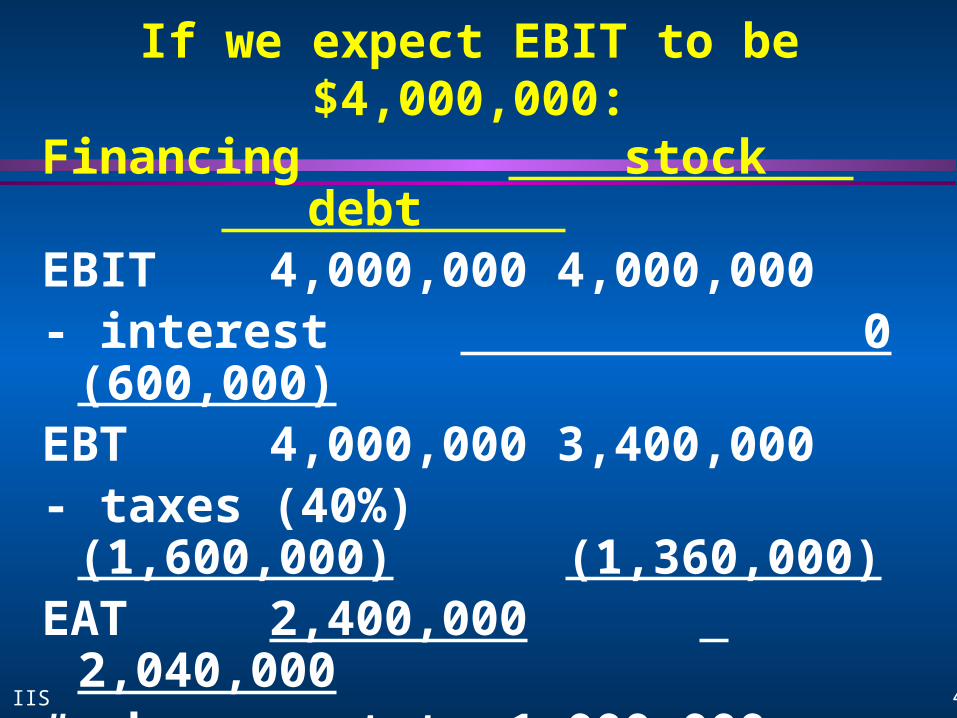

If we expect EBIT to be $4,000,000:

Financing stock debt EBIT 4,000,000 4,000,000- interest 0 (600,000)EBT 4,000,000 3,400,000- taxes (40%) (1,600,000)

(1,360,000)EAT 2,400,000 2,040,000# shares outst. 1,000,000 800,000EPS $2.40 $2.55

43IIS

If EBIT is $2,000,000, common stock financing is best. If EBIT is $4,000,000, debt financing is best.So, now we need to find a breakeven EBIT where neither is better than the other.

44IIS

If we choose stock financing:EPS

EBIT$1m $2m $3m $4m

stock financing

0

3

2

1

45IIS

If we choose bond financing:EPS

EBIT$1m $2m $3m $4m

bond financing

0

3

2

1

46IIS

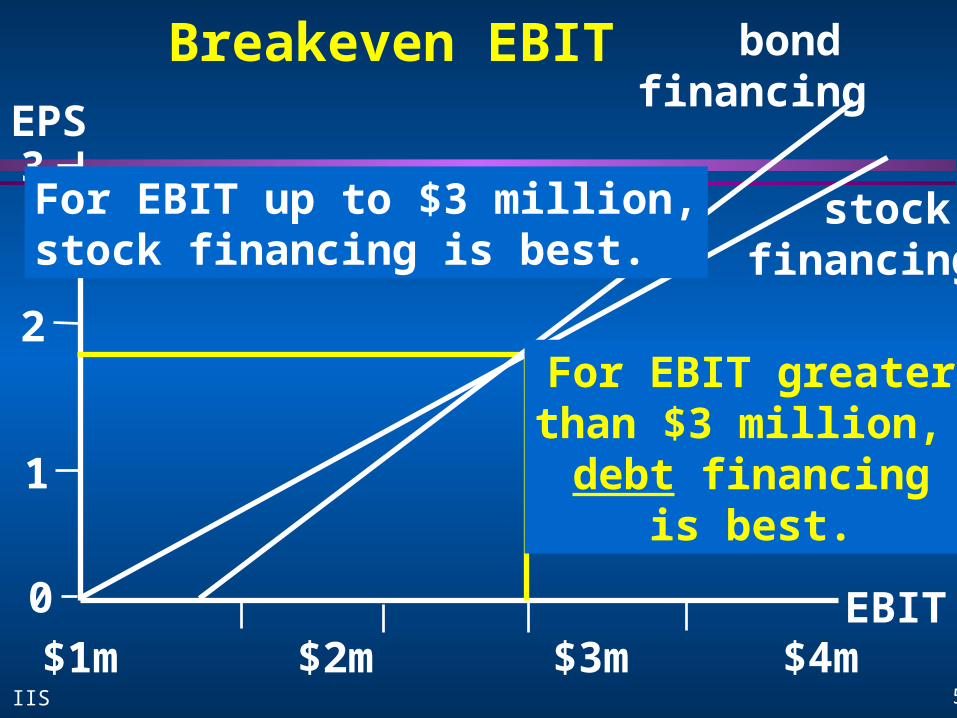

Breakeven EBITEPS

EBIT$1m $2m $3m $4m

bond financing

stock financing

0

3

2

1

47IIS

Breakeven PointSet two EPS calculations equal to each

other and solve for EBIT: Stock Financing Debt Financing(EBIT-I)(1-t) - P = (EBIT-I)(1-t) - P S S

48IIS

Breakeven Point

Stock Financing Debt Financing(EBIT-I)(1-t) - P = (EBIT-I)(1-t) - P S S

(EBIT-0) (1-.40) = (EBIT-600,000)(1-.40) 800,000+200,000 800,000

49IIS

Breakeven Point

Stock Financing Debt Financing .6 EBIT = .6 EBIT - 360,000 1 .8

.48 EBIT = .6 EBIT - 360,000

.12 EBIT = 360,000

EBIT = $3,000,000

50IIS

Breakeven EBITEPS

EBIT$1m $2m $3m $4m

bond financing

stock financing

0

3

2

1

For EBIT up to $3 million,stock financing is best.

For EBIT greaterthan $3 million, debt financing

is best.

51IIS

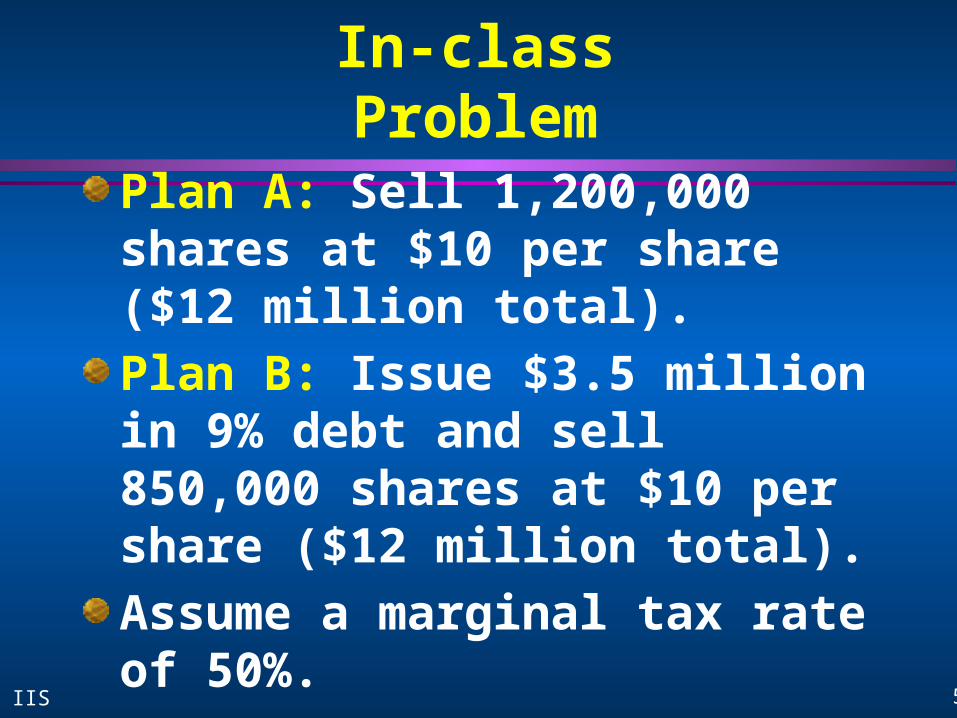

In-class Problem

Plan A: Sell 1,200,000 shares at $10 per share ($12 million total).Plan B: Issue $3.5 million in 9% debt and sell 850,000 shares at $10 per share ($12 million total).Assume a marginal tax rate of 50%.

52IIS

Breakeven EBIT

Stock Financing Levered Financing(EBIT-I) (1-t) - P = (EBIT-I) (1-t) - P S S

EBIT-0 (1-.50) = (EBIT-315,000)(1-.50) 1,200,000 850,000

EBIT = $1,080,000

53IIS

Analytical Income Statement

Stock LeveredEBIT 1,080,000 1,080,000I 0 (315,000)EBT 1,080,000 765,000Tax (540,000) (382,500)NI 540,000 382,500

Shares 1,200,000 850,000

EPS .45 .45

54IIS

Breakeven EBITFor EBIT up to $1.08 m,

stock financing is

best. For EBIT greaterthan $1.08 m,

the levered planis best.

levered financing

stock financing

EPS

EBIT$.5m $1m $1.5m $2m

0

.65

.45

.25

55IIS

In-class Problem

Plan A: Sell 1,200,000 shares at $20 per share ($24 million total).Plan B: Issue $9.6 million in 9% debt and sell shares at $20 per share ($24 million total).Assume a 35% marginal tax rate.

56IIS

Breakeven EBIT

Stock Financing Levered Financing(EBIT-I) (1-t) - P = (EBIT-I) (1-t) - P S S

(EBIT-0) (1-.35) = (EBIT-864,000)(1-.35) 1,200,000 720,000

EBIT = $2,160,000

57IIS

Analytical Income Statement

Stock LeveredEBIT 2,160,000 2,160,000I 0 (864,000)EBT 2,160,000 1,296,000Tax (756,000) (453,600)NI 1,404,000 842,400

Shares 1,200,000 720,000EPS 1.17 1.17

58IIS

Breakeven EBITlevered

financingstock

financingEPS

EBIT$1m $2m $3m $4m

0

1.5

1.17

.5

For EBIT greaterthan $2.16 m,

the levered planis best.

For EBIT up to $2.16 m,

stock financing

is best.

59IIS

Chapter 17 – Dividend Policy and International Financing

60IIS

Return =

Capital Gain Dividend Yield

+=

Stock Returns:

P1 - Po + D1

Po

P1 - Po D1

Po Po

61IIS

Dilemma: Should the firm use retained earnings for:

a) Financing profitable capital investments?

b) Paying dividends to stockholders?

62IIS

If we retain earnings for profitable investments, dividend yield will be zero,

P1 - Po D1

Po Po+Return =

Financing Profitable Capital Investments:

63IIS

If we retain earnings for profitable investments, dividend yield will be zero, but the stock price will increase, resulting in a higher capital gain.

P1 - Po D1

Po Po+Return =

Financing Profitable Capital Investments:

64IIS

If we pay dividends, stockholders receive an immediate cash reward for investing,

Paying Dividends:

P1 - Po D1

Po Po+Return =

65IIS

If we pay dividends, stockholders receive an immediate cash reward for investing, but the capital gain will decrease, since this cash is not invested in the firm.

P1 - Po D1

Po Po+Return =

Paying Dividends:

66IIS

So, dividend policy really involves two decisions:

How much of the firm’s earnings should be distributed to shareholders as dividends, andHow much should be retained for capital investment?

67IIS

Is Dividend Policy Important?

Three viewpoints: 1) Dividends are Irrelevant2) High Dividends are Best3) Low Dividends are Best

68IIS

Three viewpoints:

1) Dividends are Irrelevant. If we assume perfect markets (no taxes, no transaction costs, etc.) dividends do not matter. If we pay a dividend, shareholders’ dividend yield rises, but capital gains decrease.

69IIS

With perfect markets, investors are concerned only with total returns and do not care whether returns come in the form of capital gains or dividend yields.

P1 - Po D1

Po Po+Return =

Dividends are Irrelevant

70IIS

Therefore, one dividend policy is as good as another.

P1 - Po D1

Po Po+Return =

Dividends are Irrelevant

71IIS

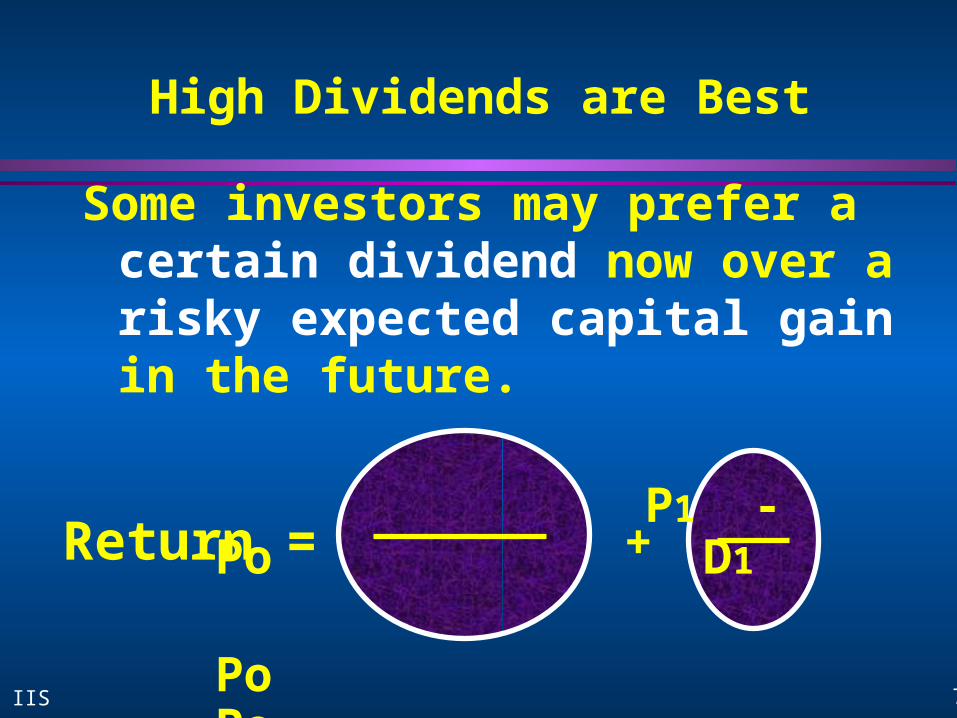

High Dividends are Best

Some investors may prefer a certain dividend now over a risky expected capital gain in the future.

P1 - Po D1

Po Po+Return =

72IIS

Low Dividends are Best

Dividends are taxed immediately. Capital gains are not taxed until the stock is sold.Therefore, taxes on capital gains can be deferred indefinitely.

73IIS

Do Dividends Matter?

Other Considerations:1) Residual Dividend Theory2) Clientele Effects3) Information Effects4) Agency Costs5) Expectations Theory

74IIS

Other Considerations

1) Residual Dividend Theory: The firm pays a dividend only if it has retained earnings left after financing all profitable investment opportunities.This would maximize capital gains for stockholders and minimize flotation costs of issuing new common stock.

75IIS

Other Considerations

2) Clientele Effects: Different investor clienteles prefer different dividend payout levels.Some firms, such as utilities, pay out over 70% of their earnings as dividends. These attract a clientele that prefers high dividends.Growth-oriented firms which pay low (or no) dividends attract a clientele that prefers price appreciation to dividends.

76IIS

Other Considerations

3) Information Effects: Unexpected dividend increases usually cause stock prices to rise, and unexpected dividend decreases cause stock prices to fall. Dividend changes convey information to the market concerning the firm’s future prospects.

77IIS

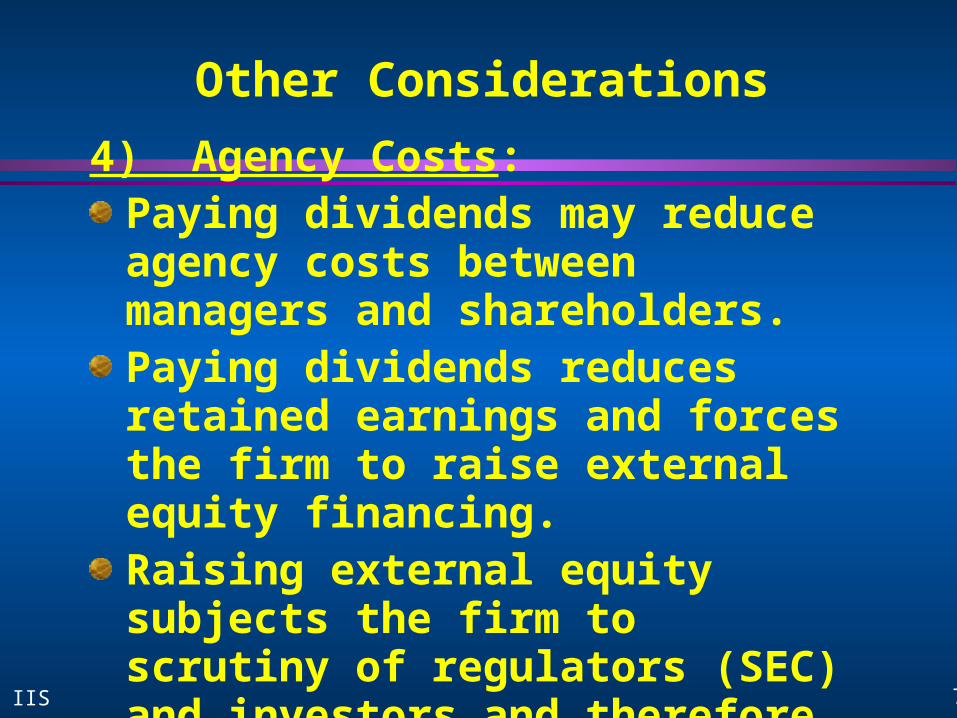

Other Considerations4) Agency Costs:

Paying dividends may reduce agency costs between managers and shareholders.Paying dividends reduces retained earnings and forces the firm to raise external equity financing.Raising external equity subjects the firm to scrutiny of regulators (SEC) and investors and therefore helps monitor the performance of managers.

78IIS

Other Considerations

5) Expectations Theory: Investors form expectations concerning the amount of a firm’s upcoming dividend.Expectations are based on past dividends, expected earnings, investment and financing decisions, the economy, etc.The stock price will likely react if the actual dividend is different from the expected dividend.

79IIS

Dividend Policies

1) Constant Dividend Payout Ratio: If directors declare a constant payout ratio of, for example, 30%, then for every dollar of earnings available to stockholders, 30 cents would be paid out as dividends.The ratio remains constant over time, but the dollar value of dividends changes as earnings change.

80IIS

Dividend Policies

2) Stable Dollar Dividend Policy: The firm tries to pay a fixed dollar dividend each quarter.Firms and stockholders prefer stable dividends. Decreasing the dividend sends a negative signal!

81IIS

Dividend Policies3) Small Regular Dividend plus Year-

End Extras The firm pays a stable quarterly dividend and includes an extra year-end dividend in prosperous years.By identifying the year-end dividend as “extra,” directors hope to avoid signaling that this is a permanent dividend.

82IIS

Dividend Payments

1) Declaration Date: The board of directors declares the dividend, determines the amount of the dividend, and decides on the payment date.

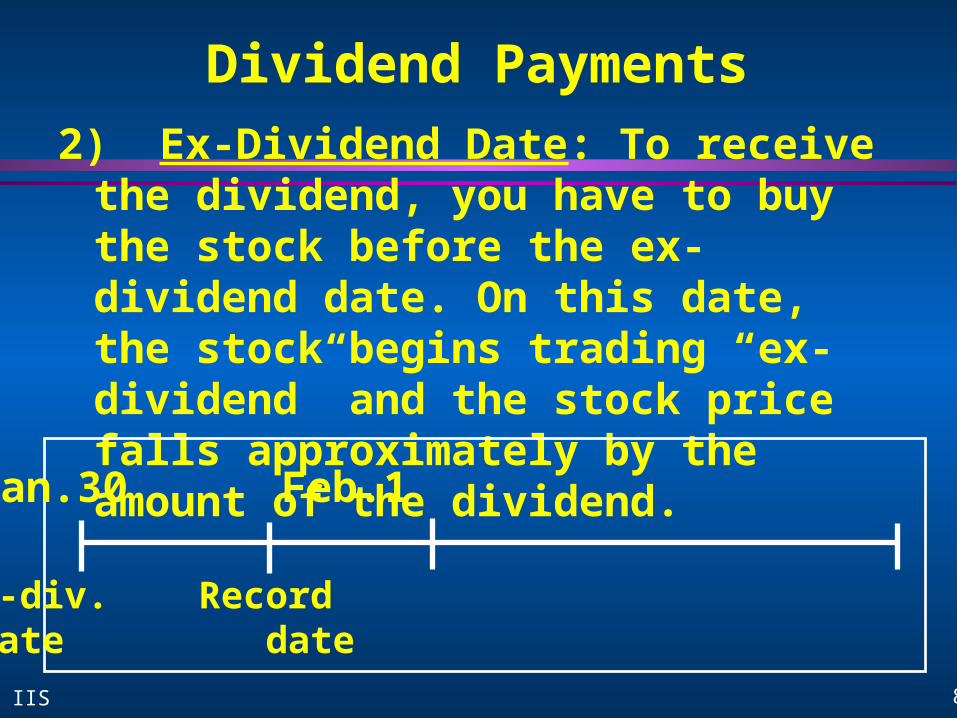

Jan.4 Jan.30 Feb.1 Mar. 11

Declare Ex-div. Record Paymentdividend date date date

83IIS

Dividend Payments2) Ex-Dividend Date: To receive the dividend,

you have to buy the stock before the ex-dividend date. On this date, the stock begins trading “ex-dividend” and the stock price falls approximately by the amount of the dividend.

Jan.4 Jan.30 Feb.1 Mar. 11

Declare Ex-div. Record Paymentdividend date date date

84IIS

Dividend Payments3) Date of Record: Two days after the ex-

dividend date, the firm receives the list of stockholders eligible for the dividend. Often, a bank trust department acts as registrar and maintains this list for the firm.

Jan.4 Jan.30 Feb.1 Mar. 11

Declare Ex-div. Record Paymentdividend date date date

85IIS

Dividend Payments

4) Payment Date: Date on which the firm mails the dividend checks to the shareholders of record.

Jan.4 Jan.30 Feb.1 Mar. 11

Declare Ex-div. Record Paymentdividend date date date

86IIS

Stock Dividends and Stock Splits

Stock Dividend: Payment of additional shares of stock to common stockholders.Example: Citizens Bancorporation of Maryland announces a 5% stock dividend to all shareholders of record. For each 100 shares held, shareholders receive another five shares.Does the shareholders’ wealth increase?

87IIS

Stock Dividends and Stock Splits

Stock Split: The firm increases the number of shares outstanding and reduces the price of each share.Example: Joule, Inc. announces a 3-for-2 stock split. For each 100 shares held, shareholders receive another 50 shares.Does this increase shareholder wealth?Are a stock dividend and a stock split the same?

88IIS

Stock Dividends and Stock Splits

Stock Splits and Stock Dividends are economically the same: The number of shares outstanding increases and the price of each share drops. The value of the firm does not change.

Example: A 3-for-2 stock split is the same as a 50% stock dividend. For each 100 shares held, shareholders receive another 50 shares.

89IIS

Stock Dividends and Stock Splits

Effects on Shareholder Wealth: These will cut the company “pie” into more pieces but will not create wealth. A 100% stock dividend (or a 2-for-1 stock split) gives shareholders two half-sized pieces for each full-sized piece they previously owned.

Example: This would double the number of shares, but would cause a $60 stock price to fall to $30.

90IIS

Stock Dividends and Stock Splits

Why bother? Proponents argue that these are used to reduce high stock prices to a “more popular” trading range (generally $15 to $70 per share).Opponents argue that most stocks are purchased by institutional investors who have millions of dollars to invest and are indifferent to price levels. Plus, stock splits and stock dividends are expensive!

91IIS

Stock Dividend Example

An investor has 120 shares. Does the value of the investor’s shares change?Shares outstanding: 1,000,000.Net income = $6,000,000. P/E = 10.25% stock dividend.

92IIS

Before the 25% stock dividend: EPS = 6,000,000/1,000,000 = $6.P/E = P/6 = 10, so P = $60 per share.Value = $60 x 120 shares = $7,200.

After the 25% stock dividend:# shares = 1,000,000 x 1.25 = 1,250,000.EPS = 6,000,000/1,250,000 = $4.80.P/E = P/4.80 = 10, so P = $48 per share.Investor now has 120 x 1.25 = 150 shares.Value = $48 x 150 = $7,200.

93IIS

Stock DividendsIn-class Problem

What is the new stock price?Shares outstanding: 250,000.Net income = $750,000.Stock price = $84. 50% stock dividend.

94IIS

Hint:

stock price P/E = net income # shares( )

95IIS

Before the 50% stock dividend: EPS = 750,000 / 250,000 = $3.P/E = 84 / 3 = 28.

After the 50% stock dividend:# shares = 250,000 x 1.50 = 375,000.EPS = 750,000 / 375,000 = $2.P/E = P / 2 = 28, so P = $56 per share.

(A 50% stock dividend is equivalent to a 3-for-2 stock split.)

96IIS

Stock Repurchases

Stock Repurchases may be a good substitute for cash dividends.If the firm has excess cash, why not buy back common stock?

97IIS

Stock Repurchases

Stock Repurchases may be a good substitute for cash dividends.If the firm has excess cash, why not buy back common stock?

98IIS

Stock Repurchases

Repurchases drive up the stock price, producing capital gains for shareholders.Repurchases increase leverage, and can be used to move toward the optimal capital structure.Repurchases signal positive information to the market—which increases stock price.

99IIS

Stock Repurchases

Repurchases may be used to avoid a hostile takeover.

Example: T. Boone Pickens attempted raids on Phillips Petroleum and Unocal in 1985. Both were unsuccessful because the target firms undertook stock repurchases.

100IIS

Stock RepurchasesMethods:

Buy shares in the open market through a broker.Buy a large block by negotiating the purchase with a large block holder, usually an institution (targeted stock repurchase).Tender offer: offer to pay a specific price to all current stockholders.

101IIS

Penutup

Tugas