international accounting, 6/e - · pdf filebiaya modal yang lebih rendah. choi/meek, ......

TRANSCRIPT

Choi/Meek, 6/e 1

International Accounting, 6/eMAHSINA, SE., MSI

by Frederick D.S. ChoiGary K. Meek

Chapter 5: Reporting and Disclosure

Choi/Meek, 6/e 2

Learning Objectives

Dapat membedakan pengungkapan kesukarelaan & wajib dan aturan pengukuran yang bisa diterapkan (Distinguish voluntary and mandatory disclosure and the applicable regulatory measures).

Mengidentifikasikan tujuan global dari sistem pengungkapan akuntansi terhadap investor – orientasi pada pasar model (Identify the broad objectives for accounting disclosure systems in investor-oriented equity markets).

Mendiskusikan laporan 'Triple-bottom line' & latar belakang kenapa tumbuh dengan pesat diantara beberapa perusahaan besar. (Discuss “triple-bottom line” reporting and why it is a growing tendency among large multinational corporations).

Choi/Meek, 6/e 3

Learning Objectives

Mengerti dasar -dasar praktek pengungkapan laporan keuangan perusahaan: (a) Pengungkapan informasi kedepan (b) Segmen Pengungkapan (c) Pelaporan tanggungjawab sosial (d) pengungkapan khusus untuk laporan non domestik (e) pengungkapan pengaturan perusahaan (f) laporan & pengungkapan perdagangan internet. (Have a basic understanding of the following selected corporate financial-disclosure practices: (a) disclosures of forward-looking information, (b) segment disclosures, (c) social responsibility reporting, (d) special disclosures for non-domestic financial statement users, and (e) corporate governance disclosures).(f)Internet business reporting & disclosure

Choi/Meek, 6/e 4

Perkembangan Pengungkapan Development of Disclosure

Pengungkapan Sukarela (Voluntary disclosure) Pengungkapan sukarela meningkat seiring dengan tuntutan informasi yang

detail dan berkala dari investor. Voluntary disclosures are increasing as investors demand more detailed and timely information

Keuntungan pengungkapan sukarela, menyangkut:Keuntungan pengungkapan sukarela, menyangkut: Biaya transaksi yg lebih rendah Bunga yg lebih tinggi dari analis keuangan & investor Meningkatkan likuiditas saham Biaya modal yang lebih rendah

Choi/Meek, 6/e 5

Voluntary Disclosure = Financial Reporting

Mekanisme CacatManajer Investor

• Manajer memiliki informasi kuat tentang perusahaan• Insentif manajer tidak sesuai dengan bunga dari semua pemegang saham

• Pengaturan akuntansi dan audit yang tidak sempurna

kompensasi Bonus ==> Saham

Solusi

....But managers’ incentives for disclosure aren’t always aligned with those of investors.....

Choi/Meek, 6/e 6

... Disclosure regulations and third party certification can improve the functioning of capital markets....

Regulasi & Sertifikasi Pihak Ketiga

Contoh: Regulasi pembukuan & pengungkapan Contoh: Auditing

Regulasi Pembukuan --> mengurangi kemampuan manajer untuk mencatat transaksi ekonomi dg cara bahwa tdk dengan bunga

pemegang saham terbaikRegulasi Pengungkapan --> menentukan keperluan untuk memastikan

bahwa pemegang saham menerima informasi dg lengkap, berkala & akurat

Auditing --> Auditor memastikan bahwa manajer menggunakan kebijakan akuntansiyang tepat

Choi/Meek, 6/e 7

Development of Disclosure (contin)Kebutuhan Pengaturan Pengungkapan -

Regulatory disclosure requirements Semua Otoritas Pasar Modal ingin memastikan

bahwa investor memiliki informasi yang cukup untuk memperbolehkan mereka mengevaluasi kinerja dan prospek perusahaan. Stock exchanges want to be sure that investors have enough information to evaluate a company’s performance and prospects.

Pengungkapan melindungi Investor, tapi perlindungan rerhadap pemegang saham ini bermacam2x di seluruh negara. Disclosure protects investors, but shareholder protection varies across countries. Contoh: Insider trading di China – forbidden tp di Jerman tdk dianggap kriminal s.d Akta Perdagangan Sekuritas diumumkan.

Choi/Meek, 6/e 8

Development of Disclosure (contin)Twin objectives of investor oriented markets (Frost and

Lang 1996): Investor protection

Investors are provided with material information.

And are protected through monitoring and enforcement.

Market quality Markets are fair, orderly, and efficient. And free from abuse and misconduct.

FairFair Akses Wajar & Bisnis Opportunity

OrderlyOrderly Meningkatkan likuiditas dan mengurangi biaya transaksi

EfficientEfficient Ditandai dg Investor Trust dan Pembentukan Modal

Choi/Meek, 6/e 9

Development of Disclosure (contin)Frost & Lang 4 prinsip investor yg berorientasi

pasar yg harus dijalankan: Keefektifan biaya, Regulasi biaya pasar

sebaiknya dibandingkan dengan keuntungan sekuritasnya.

Fleksibilitas & kebebasan pasar. Regulasi tidak seharusnya menghalangi kompetisi & evoludi pasar.

Laporan keuangan transparan & pengungkapan menyeluruh

Perlakuan setara perusahaan domestik dan asing

Choi/Meek, 6/e 10

Development of Disclosure (contin)

SEC financial reporting debate Foreign registrants must furnish financial information

substantially similar to that required of domestic companies.

Must reconcile net income and stockholders’ equity to U.S. GAAP if the registrant uses another GAAP.

Do SEC requirements deter foreign companies from listing their securities in the U.S.?

Or do the requirements protect investors and ensure the quality of U.S. capital markets?

Sarbanes-Oxley requirements are also believed to deter foreign companies from listing in the U.S.

Choi/Meek, 6/e 11

Reporting and Disclosure Practices Forward-looking information – Progressive Information

(Informasi kedepan – Informasi progressive) Includes

Forecasts of revenues, income, cash flows, capital expenditures

Prospective information about future economic performance or position

Statements of management’s plans and objectives for future operations

Ketiga informasi progressive diatas umum - - (1) Perkiraan , (2) Informasi potensial , (3) Sasaran & Tujuan Why?

Forecasts are inherently unreliable. -- menggabungkan subyek2x peristiwa yg blm pasti

Legal repercussions if forecasts aren’t met. -- Ada akibat bagi manajemen jika forecast tidak tepat

Choi/Meek, 6/e 12

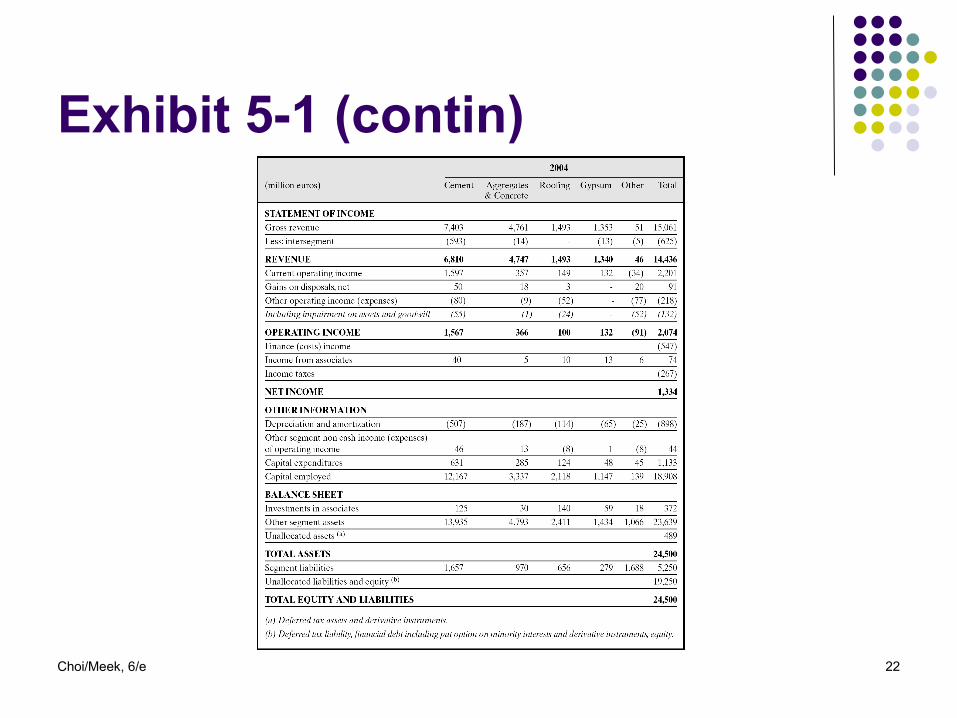

Reporting and Disclosure Practices (contin) Segment disclosures

Disaggregated information about a firm’s industry and geographic operations and results - - Sementara analis dan investor menuntut informasi yg signifikan & berkembang

Includes disaggregated information on Revenue Income Depreciation and amortization Capital expenditures Assets Liabilities

Helps users understand how the parts make up the whole Product lines and areas of the world vary in terms of risks,

returns, and opportunities

Choi/Meek, 6/e 13

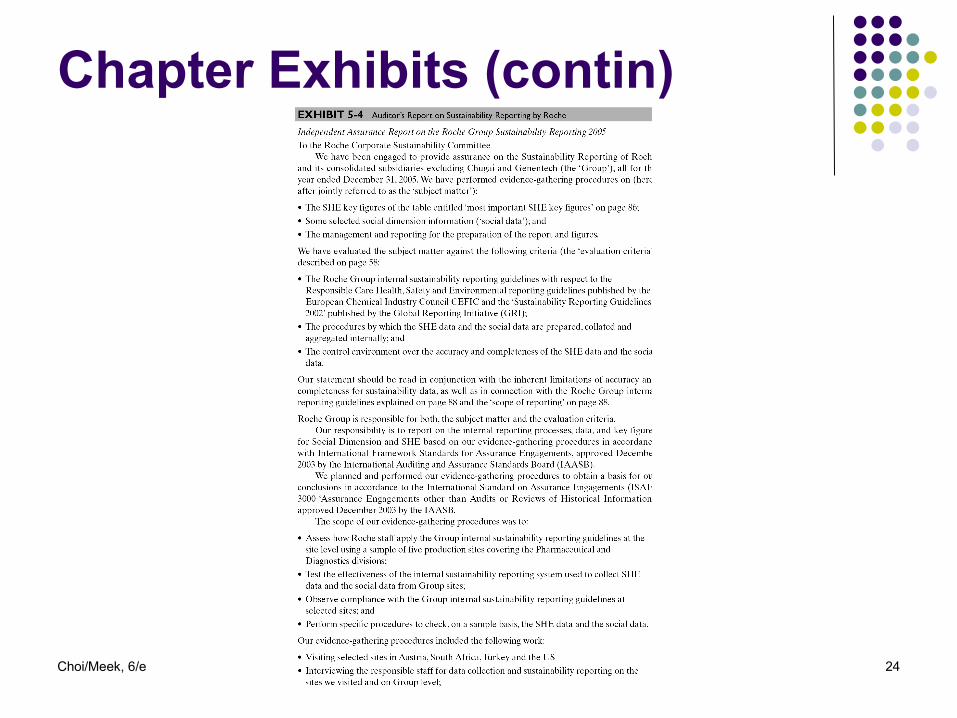

Reporting and Disclosure Practices (contin) Social responsibility reporting

Reporting to “stakeholders”: employees, customers, suppliers, governments, activist groups, the general public, in addition to investors

The measurement and communication of information about a company’s effects on employee welfare, the local employee welfare, the local community, and the environmentcommunity, and the environment

A way to demonstrate corporate citizenship – perusahaan perusahaan pendudukpenduduk

“Sustainability” reports integrate economic, social, and environmental performance “Triple-bottom line reporting”: profits, people, planet

Increasingly being audited to avoid the charge of “green-washing” (Hub dg masyarakat secara alamiah)

Choi/Meek, 6/e 14

Reporting and Disclosure Practices (contin)

Examples: Employee reporting

Employment levels and personnel costs by division and region of the world Management development Compensation Diversity Human rights

Environmental reporting Impact of production processes, products, and services on

Air Water Land Biodiversity Human health

Water, raw material, and energy consumption Activities to reduce pollution Spending on all of the above

Despite criticisms, becoming mainstream among multinational companies

Global Reporting Initiative has issued guidelines

Choi/Meek, 6/e 15

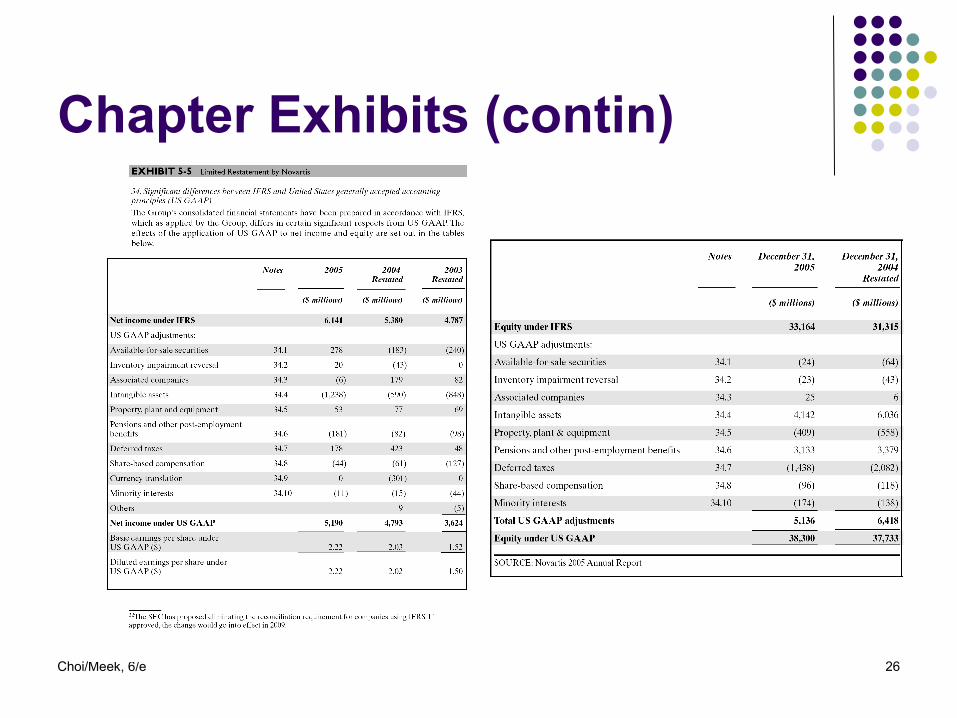

Reporting and Disclosure Practices (contin) Special disclosures for non-domestic

financial statement users Language translations and currency restatements Discussion of GAAP differences Limited restatement of income and stockholders’

equity to another GAAP This is the SEC requirement

Complete financial statements using another GAAP, such as IFRS

Choi/Meek, 6/e 16

Reporting and Disclosure Practices (contin) Corporate governance disclosures

Governance means the responsibilities, accountability, and relationships among shareholders, board members, and managers to meet corporate objectives.

Governance issues include: Rights and treatment of shareholders Responsibilities of the board Disclosure and transparency Role of stakeholders

Choi/Meek, 6/e 17

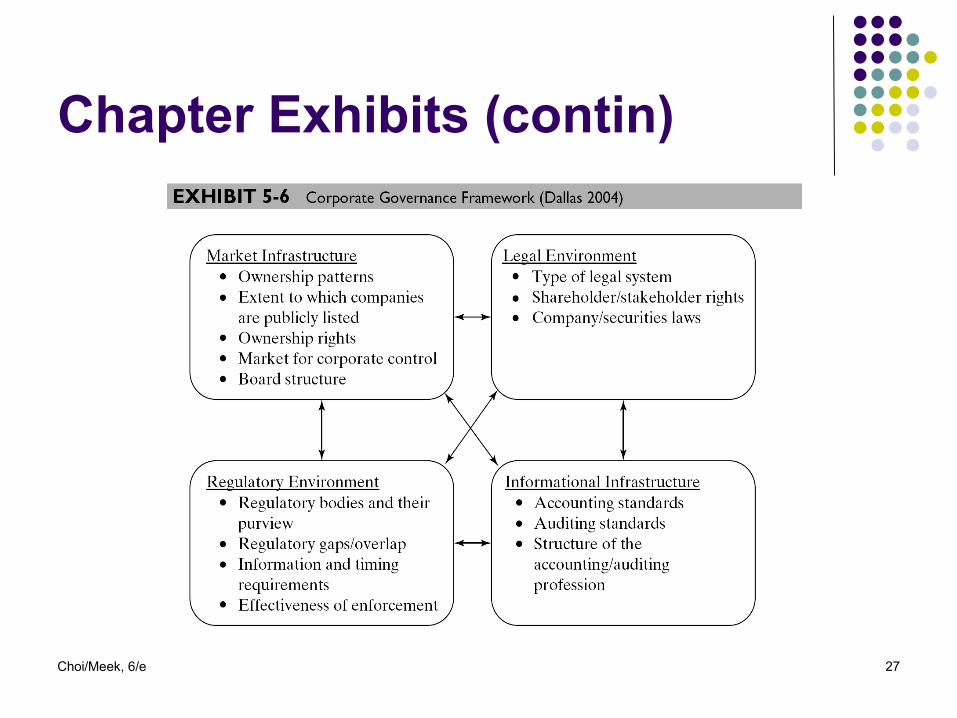

Reporting and Disclosure Practices (contin)

Governance framework (Dallas 2004) Market infrastructure

Ownership patterns Extent to which companies are publicly listed Ownership rights Market for corporate control Board structure

Legal environment Type of legal system Shareholder/stakeholder rights Company/securities laws

Regulatory environment Regulatory bodies and their purview Regulatory gaps/overlap Information and timing requirements Effectiveness of enforcement

Informational infrastructure Accounting standards Auditing standards Structure of the accounting/auditing profession

Governance mechanisms and disclosures are improving around the world. OECD issued its revised Principles of Corporate Governance in 2004. Disclosure is a key element of any good system of corporate governance.

Choi/Meek, 6/e 18

Reporting and Disclosure Practices (contin) Internet business reporting and

disclosure World Wide Web increasingly used as an

information dissemination channel. XBRL will allow users to easily manipulate

companies’ financial statement data.

Choi/Meek, 6/e 19

Annual Report Disclosures in Emerging-Market Countries

Generally less extensive and less credible than disclosures of companies from developed countries.

Empirical evidence shows that earnings are less opaque in developed countries than in developing countries.

Monitoring and enforcement of disclosure requirements are also less extensive in developing countries.

Choi/Meek, 6/e 20

Implications for Financial Statement Users Expect wide variation in disclosure levels and

financial reporting practices. The levels of mandatory and voluntary disclosure

are increasing worldwide. Managers of companies from low-disclosure

countries should consider adopting enhanced disclosure.

Enhanced disclosures can result in competitive advantage over companies with restrictive disclosure policies.

Choi/Meek, 6/e 21

Chapter Exhibits

Choi/Meek, 6/e 22

Exhibit 5-1 (contin)

Choi/Meek, 6/e 23

Exhibit 5-1 (contin)

Choi/Meek, 6/e 24

Chapter Exhibits (contin)

Choi/Meek, 6/e 25

Exhibit 5-4 (contin)

Choi/Meek, 6/e 26

Chapter Exhibits (contin)

Choi/Meek, 6/e 27

Chapter Exhibits (contin)

Choi/Meek, 6/e 28

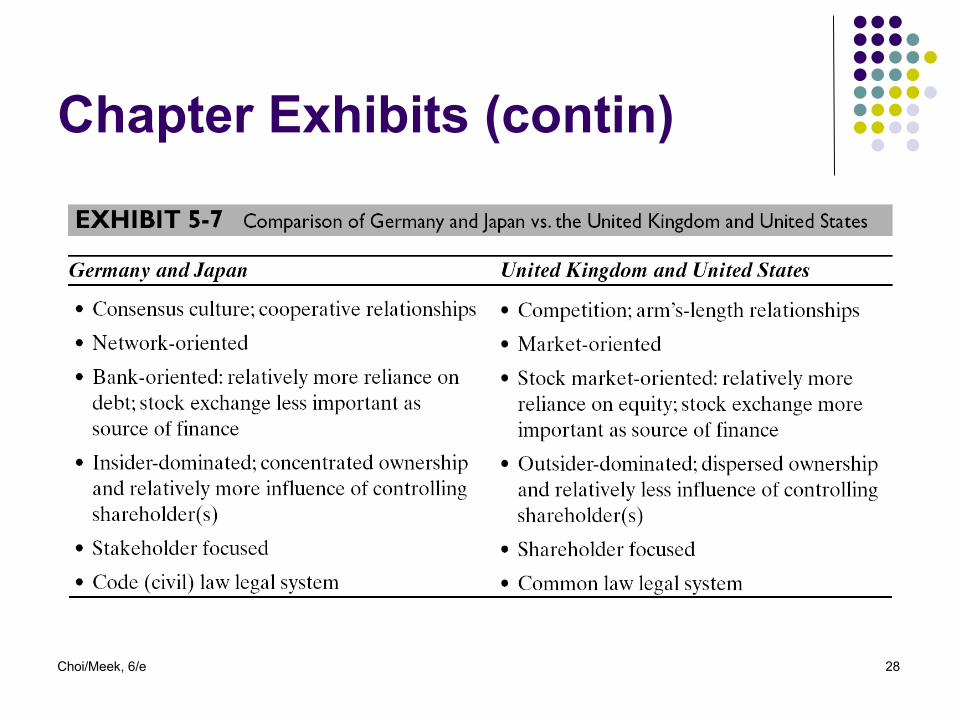

Chapter Exhibits (contin)

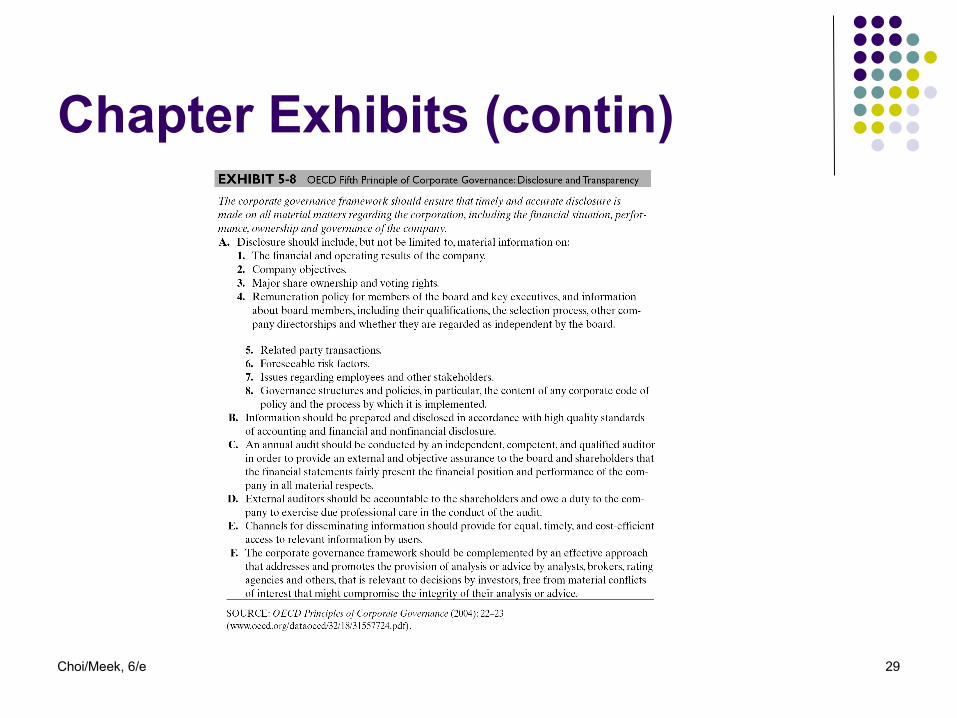

Choi/Meek, 6/e 29

Chapter Exhibits (contin)

Choi/Meek, 6/e 30

Chapter Exhibits (contin)