1 manajemen risiko di perbankan syariah associate prof rifki ismal, phd kuliah tamu stie ahmad...

TRANSCRIPT

1

MANAJEMEN RISIKO DI PERBANKAN

SYARIAH

Associate Prof Rifki Ismal, PhD

Kuliah Tamu

STIE AHMAD DAHLAN (Mei 26th, 2012)

2

AGENDAAGENDA

• Risk Management

• Risk Management in Islamic banking

• Products and its risk

• Liquidity risk Management

• Fact in the Industry

3

Curriculum Vitae• Academic Titles

– Sarjana Ekonomi, Fakultas Ekonomi UNIVERSITAS INDONESIA (FEUI).

– Master in Applied Economics, Department of Economics, UNIVERSITY OF MICHIGAN ANN ARBOR, USA.

– PhD in Islamic Finance, DURHAM UNIVERSITY, UK– Associate Professor, Australian Government.

• Pekerjaan– Peneliti Ekonomi di Direktorat Riset Ekonomi dan Kebijakan

Moneter dan Direktorat Perbankan Syariah, BANK INDONESIA.

– Staf Ahli Deputi Gubernur BANK INDONESIA.– Pengajar FEUI Extension (1997- 2002).– Pengajar FEUI regular (1997-2000).– Pengajar MM FEUI (2004-2005 dan sekarang).– Pengajar MAKSI (2004-2007).– Pengajar Strasbourg School of Business (France) (2008)– Pengajar di PSKTTI, Trisakti, Paramadina (sekarang)

4

• Alamat – Kantor : Departemen Perbankan Syariah Bank Indonesia

: Gedung A lt 21: Jl. MH. Thamrin No 2 Jakpus.

– Email : [email protected] atau [email protected]– Telp : 0821 14 320 365 / 3818451

5

What is What is Risk Risk Mgt and How Important Mgt and How Important ::General Ideas of risk managementGeneral Ideas of risk management

• Risk management determines the successfulness of financial institution in managing fund and providing well-expected return to stakeholders.

• It prevents a bank from financial failure, insolvency, liquidity distress, etc and build a good communication/coordination with stakeholders.

• It measures and explains every type of risk which will allow a bank to take necessary actions to anticipate and mitigate any risk.

• In general it is necessity for the robustness of the overall financial system and economic stability at the end.

• Risk management unexceptionally becomes part of Islamic banking institution with its unique characteristics and operations.

• Risk in financial terms is usually defined as the probability that the actual return may differ from the expected return (Howells and Bain, 1999:30). There are in fact three broad categories of risk namely (1) Financial risk, (2) Business risk and lastly (3) Operational risk.

6

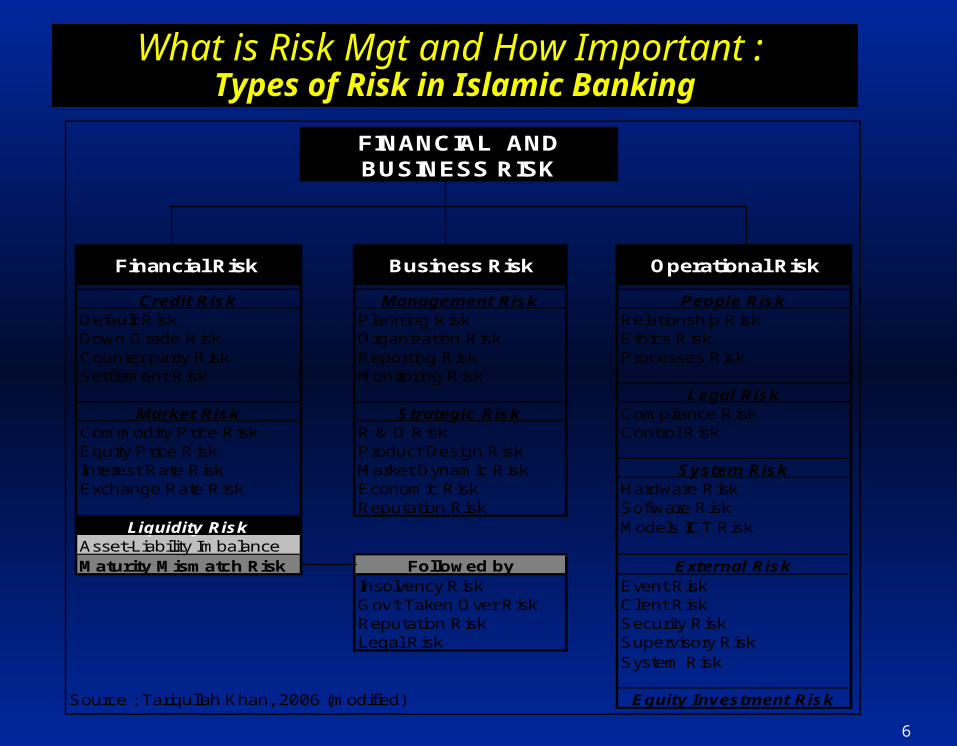

What is What is Risk Risk Mgt and How Important Mgt and How Important : : Types of Risk in Islamic BankingTypes of Risk in Islamic Banking

Credit Risk Management Risk People RiskDefault Risk Planning Risk Relationship RiskDown Grade Risk Organization Risk Ethics RiskCounter party Risk Reporting Risk Processes RiskSettlement Risk Monitoring Risk

Legal RiskMarket Risk Strategic Risk Compliance Risk

Commodity Price Risk R & D Risk Control RiskEquity Price Risk Product Design RiskInterest Rate Risk Market Dynamic Risk System RiskExchange Rate Risk Economic Risk Hardware Risk

Reputation Risk Software RiskLiquidity Risk Models ICT Risk

Asset-Liability ImbalanceMaturity Mismatch Risk Followed by External Risk

Insolvency Risk Event RiskGov't Taken Over Risk Client RiskReputation Risk Security RiskLegal Risk Supervisory Risk

System Risk

Source : Tariqullah Khan, 2006 (modified) Equity Investment Risk

FINANCIAL AND BUSINESS RISK

Financial Risk Business Risk Operational Risk

7

What is What is Risk Risk Mgt and How Important Mgt and How Important : :

Types of Risk in Islamic BankingTypes of Risk in Islamic Banking• Risk can be expressed within a casual and interactive system,

as the impact of each risk can’t be seen isolated, since they correlate and influence each other.

• Financial risk is the exposures that result in a direct financial loss to the assets or liabilities of a bank. Besides credit, market risk and liquidity risk, Islamic banks face equity investment risk.

• Credit risk relates to the performance of entrepreneurs: failure to fulfill their payment obligations, settlement, clearing, etc.

• Market risk happens due to unfavorable price movement or economic/financial condition such as RoR risk, exchange rate, inflation, etc. Unlike conventional one, Islamic banks bear risk of tradable, marketable, leaseable asset and mark up risk.

• Liquidity risk consists of 2 part: (i) Liquidity of financial instruments in financial market and; (ii) Liquidity related to solvency.

8

What is What is Risk Risk Mgt and How Important Mgt and How Important : :

Types of Risk in Islamic BankingTypes of Risk in Islamic Banking• Business risk links with the performance of bank’s business

and internal action such as business policy, infrastructure, payment system, etc.

• Thus business risk deals with (i) management risk which asks how is bank’s planning, organizing, monitoring, reporting, etc and (ii) strategic risk is like R&D, product design, etc.

• Operational risk occurs if a bank fails to manage people, system, legal, external risk and equity investment. It is internal process risk which brings together harmonization of :

– People (relationship, ethics, process, etc); – Legal (compliance and control risk); – System (hardware, software, etc) and;– External risk (event, clients, security, supervisory, etc).– Equity investment (asset, pricing, valuation).

9

What is What is Risk Risk Mgt and How Important Mgt and How Important : :

Types of Risk in Islamic BankingTypes of Risk in Islamic Banking• Mark up risk is risk because of fluctuation of benchmark

rate or inaccurate/unfavorable mark up determination.

• Commodity price risk happens due to the fluctuation of price of a commodity.

• Legal risk is because of improper regulation, lack of regulation, etc.

• Withdrawal risk is when depositors take out their money for regular or irregular reasons.

• Fiduciary risk, when Islamic bank operates unislamically (violating sharia principles).

• Displaced commercial risk occurs when depositors switch their deposit into conventional one which offers more profitable/attractive return.

10

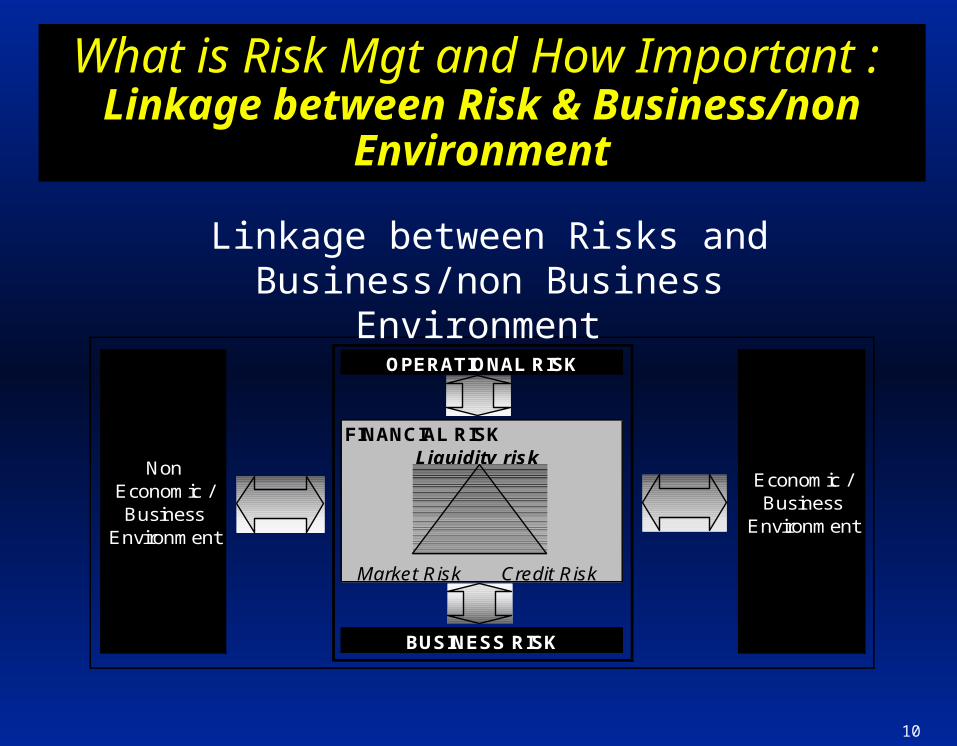

What is What is Risk Risk Mgt and How Mgt and How Important Important : :

Linkage between Linkage between Risk & Risk & Business/non EnvironmentBusiness/non Environment

FINANCIAL RISK

Economic / Business

Environment

Non Economic / Business

Environment

OPERATIONAL RISK

BUSINESS RISK

Liquidity risk

Market Risk Credit Risk

Linkage between Risks and Business/non Business Environment

11

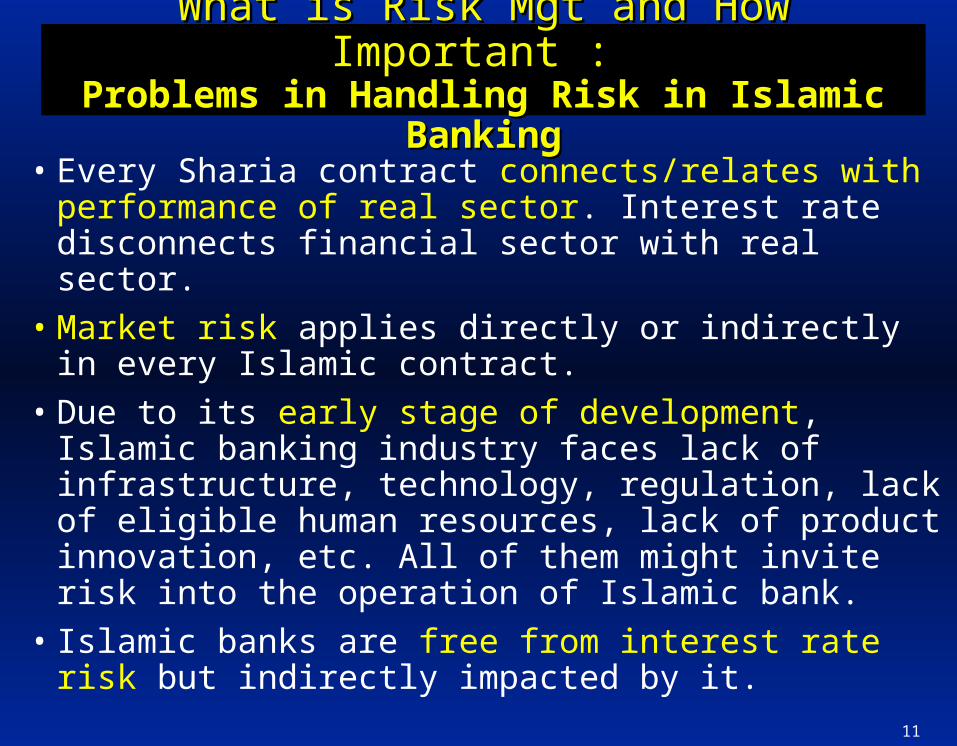

What is What is Risk Risk Mgt and How Important Mgt and How Important : : Problems in Handling Risk in Islamic Problems in Handling Risk in Islamic

BankingBanking

• Every Sharia contract connects/relates with performance of real sector. Interest rate disconnects financial sector with real sector.

• Market risk applies directly or indirectly in every Islamic contract.

• Due to its early stage of development, Islamic banking industry faces lack of infrastructure, technology, regulation, lack of eligible human resources, lack of product innovation, etc. All of them might invite risk into the operation of Islamic bank.

• Islamic banks are free from interest rate risk but indirectly impacted by it.

12

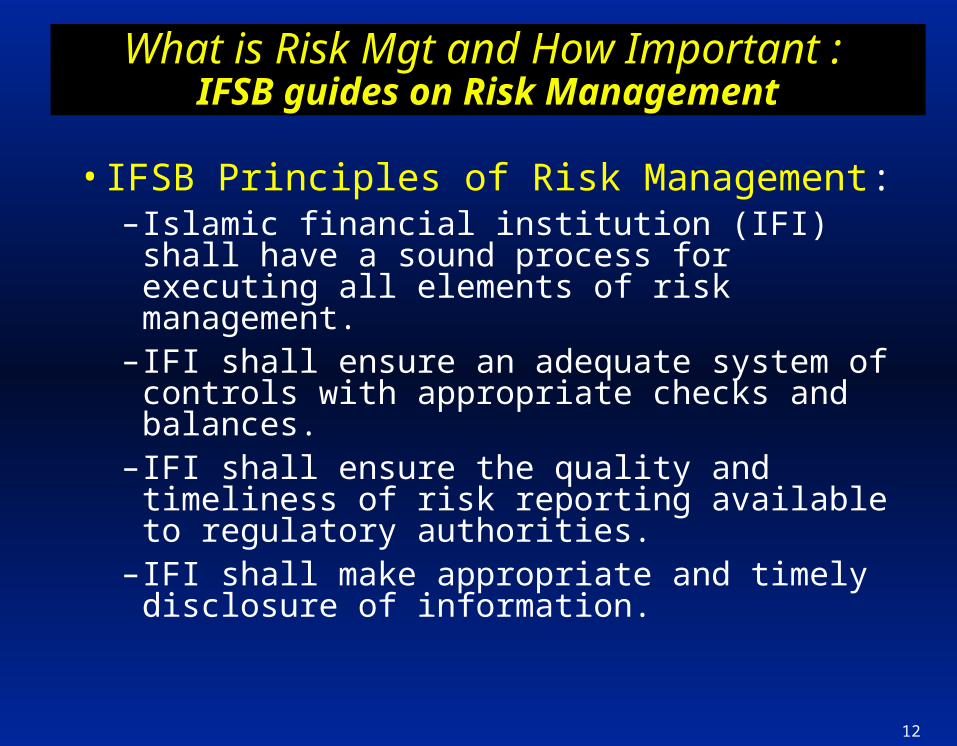

What is What is Risk Risk Mgt and How Important Mgt and How Important : : IFSB guides on Risk ManagementIFSB guides on Risk Management

• IFSB Principles of Risk Management: – Islamic financial institution (IFI) shall have a

sound process for executing all elements of risk management.

– IFI shall ensure an adequate system of controls with appropriate checks and balances.

– IFI shall ensure the quality and timeliness of risk reporting available to regulatory authorities.

– IFI shall make appropriate and timely disclosure of information.

13

What is What is Risk Risk Mgt and How Important Mgt and How Important : :

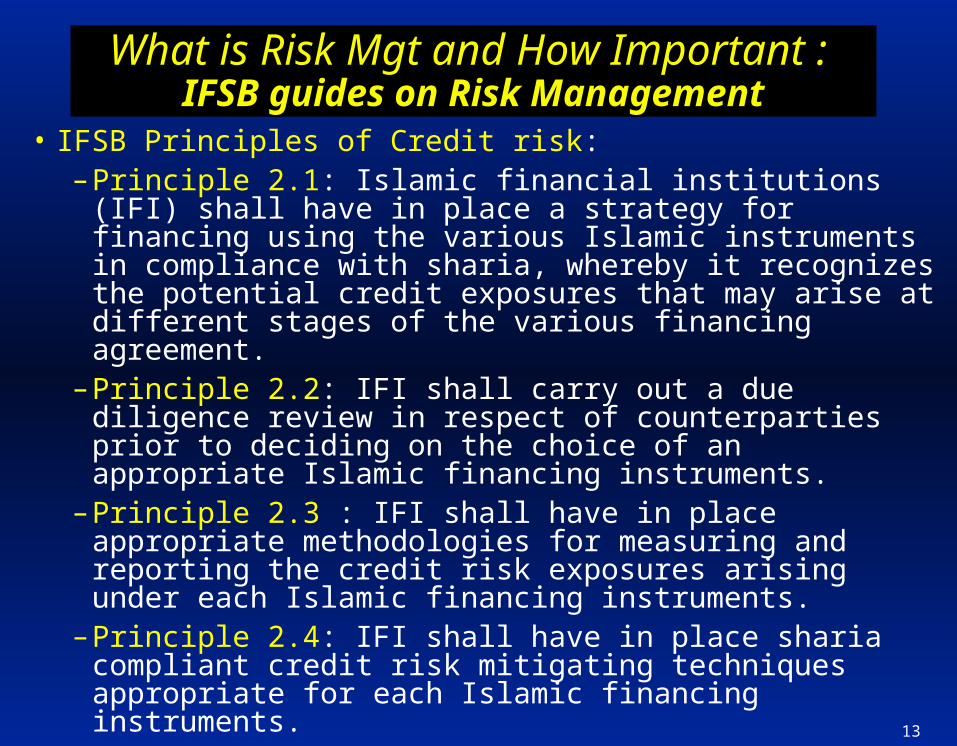

IFSB guides on Risk ManagementIFSB guides on Risk Management• IFSB Principles of Credit risk:

– Principle 2.1: Islamic financial institutions (IFI) shall have in place a strategy for financing using the various Islamic instruments in compliance with sharia, whereby it recognizes the potential credit exposures that may arise at different stages of the various financing agreement.

– Principle 2.2: IFI shall carry out a due diligence review in respect of counterparties prior to deciding on the choice of an appropriate Islamic financing instruments.

– Principle 2.3 : IFI shall have in place appropriate methodologies for measuring and reporting the credit risk exposures arising under each Islamic financing instruments.

– Principle 2.4: IFI shall have in place sharia compliant credit risk mitigating techniques appropriate for each Islamic financing instruments.

14

What is What is Risk Risk Mgt and How Important Mgt and How Important : : IFSB guides on Risk ManagementIFSB guides on Risk Management

• IFSB Principles of Market risk: – Principle 4.1: IFI shall have in place an appropriate

framework for market risk management in respect of all assets held, including those that do not have a ready market and/or are exposed to high price volatility.

• IFSB Principles of Liquidity risk:– Principle 5.1: IFI shall have in place a liquidity

management framework taking into account separately and on an overall basis their liquidity exposure in respect of each category of current accounts, unrestricted and restricted investment accounts.

– Principle 5.2: IFI shall undertake liquidity risk commensurate with their ability to have sufficient recourse to sharia compliant funds to mitigate such risk.

15

Sharia Framework on Risk Mgt Sharia Framework on Risk Mgt : : Risk in Sharia JurisprudenceRisk in Sharia Jurisprudence

• Risk is close to definition of gharar in sharia.• Gharar is any uncertainty or ambiguity created by the lack

of information or control in contract. • By size, there are gharar fahish (big gharar) and gharar

yasir (small gharar). The former should be controlled and minimized while the latter has characteristics of (i) Negligible (ii) Inevitable (iii) Unintentional; and could be borne or ignored.

• In gharar fahish, by behavior, there are natural gharar and created gharar.

• Natural gharar happens without any intervention of any party like business loss, natural disaster, asset destruction, etc. Islamic banks may or may not avoid this risk but can not transfer it to other parties.

16

Sharia Framework on Risk Mgt Sharia Framework on Risk Mgt : : Risk in Sharia JurisprudenceRisk in Sharia Jurisprudence

• Created gharar occurs because of human interventional like gambling, impermissible contracts, fake contracts, invalid contracts, etc. Types of intervention are taghrir al fi’li (fraudulent acts); taghrir al qawli (fraudulent statement); taghrir kithman (fraudulent concealment).

• Islamic banks may not do and must avoid this created gharar because created gharar means creating problem of uncertainty or playing with uncertainty condition.

• Risk management in Islamic banking deals with minimizing lack of information and maximizing control through sharia approaches such as profit and loss sharing, al ghunmu billa ghurmi, al kharaj bid daman, positive or negative sum game, cooperation and coordination and sharia compliance business activities, etc.

17

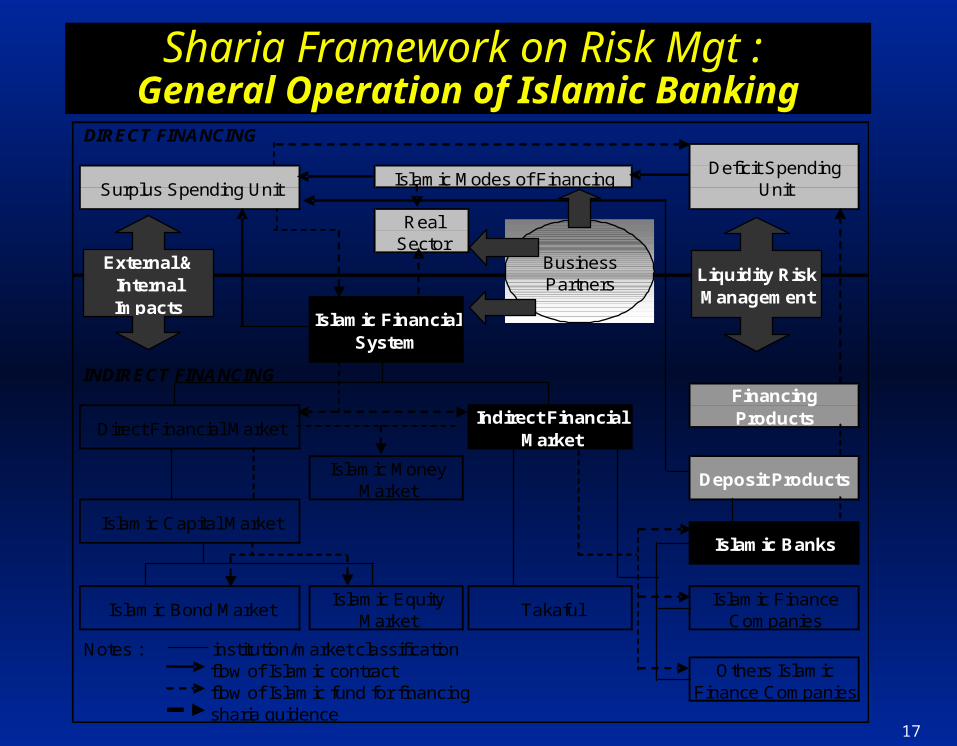

Sharia Framework on Risk Mgt Sharia Framework on Risk Mgt : : General Operation of Islamic BankingGeneral Operation of Islamic BankingDIRECT FINANCING

INDIRECT FINANCING

Notes : institution/market classification flow of Islamic contract flow of Islamic fund for financing sharia guidence

Others Islamic Finance Companies

Islamic Capital Market

Islamic Bond MarketIslamic Equity

Market

Financing Products

Deposit Products

Islamic Finance Companies

Islamic Banks

Surplus Spending UnitDeficit Spending

Unit

Takaful

Islamic Modes of Financing

Islamic Financial System

Indirect Financial Market

Islamic Money Market

Real Sector

Direct Financial Market

Business Partners

External & Internal Impacts

Liquidity Risk Management

18

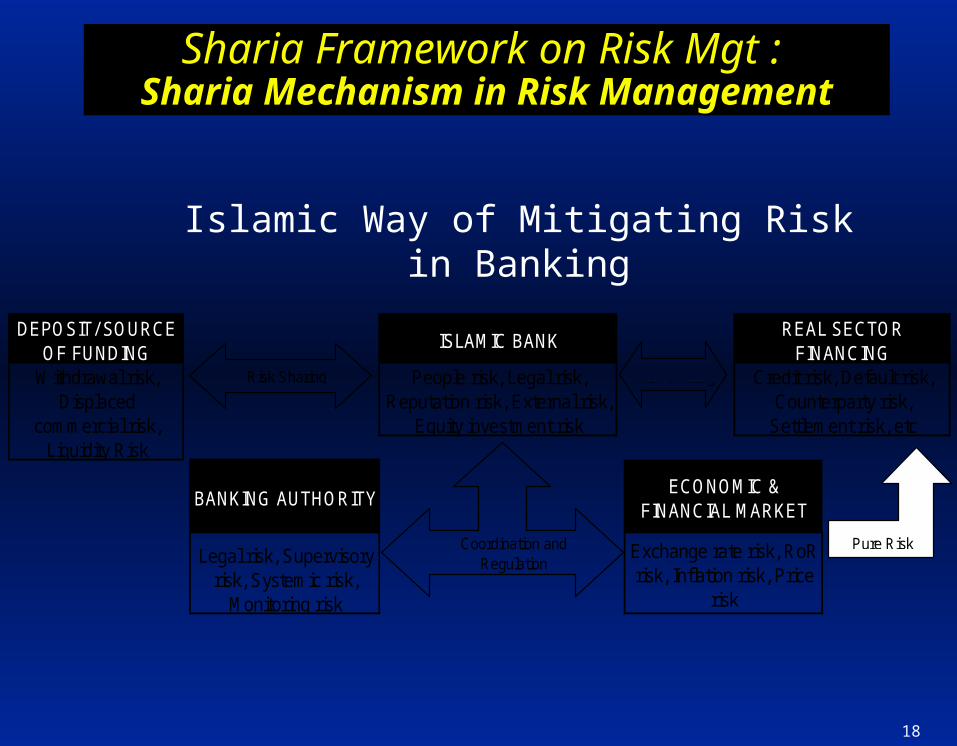

Sharia Framework on Risk Mgt Sharia Framework on Risk Mgt : : Sharia Mechanism in Risk Sharia Mechanism in Risk

ManagementManagement

Islamic Way of Mitigating Risk in Banking

ECONOMIC & FINANCIAL MARKET

Exchange rate risk, RoR risk, Inflation risk, Price

risk

Legal risk, Supervisory risk, Systemic risk,

Monitoring risk

Withdrawal risk, Displaced

commercial risk, Liquidity Risk

DEPOSIT/ SOURCE OF FUNDING

ISLAMIC BANK REAL SECTOR

FINANCING

BANKING AUTHORITY

Credit risk, Default risk, Counterparty risk,

Settlement risk, etc

People risk, Legal risk, Reputation risk, External risk,

Equity investment risk

Risk Sharing Risk Sharing

Coordination and Regulation

Pure Risk

19

Sharia Framework on Risk Mgt Sharia Framework on Risk Mgt : : Sharia Mechanism in Risk Sharia Mechanism in Risk

ManagementManagement• Islamic contracts require depositors to fully understand

consequence of dealing with Islamic bank particularly: no guarantee/fixed return on deposit, no return on demand deposit, periodical withdrawal on long term time deposit and risk/return sharing.

• Islamic bank mitigates its risk through risk sharing with depositors and entrepreneurs particularly profit and loss sharing (PLS) or return sharing scheme.

• Economic / financial market risks are pure risk that can not be hindered by all parties but have to be minimized, avoided and handled properly. Islamic bank does not eliminate risk (interest based) but sharing/handling risk.

• Regulator coordinates and designs proper legal and regulatory standard to control and manage performance of Islamic banking as well as preventing any unfavorable economic/business condition.

20

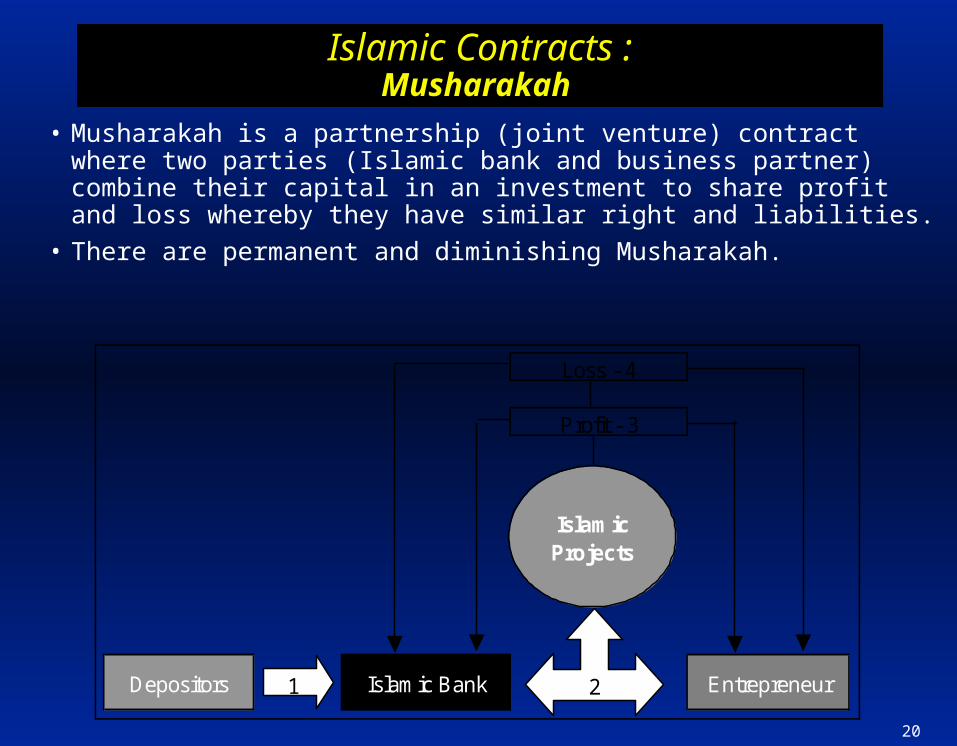

Islamic Contracts Islamic Contracts ::Musharakah Musharakah

• Musharakah is a partnership (joint venture) contract where two parties (Islamic bank and business partner) combine their capital in an investment to share profit and loss whereby they have similar right and liabilities.

• There are permanent and diminishing Musharakah.

Depositors

Profit - 3

Loss - 4

Islamic Bank Entrepreneur2

Islamic Projects

1

21

Islamic Contracts Islamic Contracts ::Musharakah Musharakah

• Credit, Operational, Market and Liquidity risk exposes both permanent and diminishing Musharakah.

• Permanent Musharakah faces operational risk in determination of profit and loss sharing. Profit is shared related/unrelated to capital contribution while loss sharing is precisely based on capital contribution.

• When business fails to produce income, it bears credit risk. This might interrupt payment of PLS to depositors and invite liquidity risk.

• Finally if the business can not be continued, value of final capital faces market risk.

• Diminishing Musharakah exposes operational risk when business partner fails to buy share of diminishing capital.

• Since expected income can’t be fulfilled, credit risk appears.

22

Islamic Contracts Islamic Contracts ::Musharakah Musharakah

• When it disturbs payment of PLS to depositors, liquidity risk comes into the bank.

• At the end of diminishing Musharakah, when value of total equity investment is different with market value, banks bears market risk.

• To handle both operational risk and credit risk, bank must take part in company’s management, do monitoring and insure the business. Bank may have right to sale its share to third party in diminishing Musharakah contract to avoid credit risk.

• Stop the loss of a business is one of the solutions to mitigate market risk.

• Gradually selling bank’s share to business partner is also another solution for credit and market risk. Finally, reserving capital might hinder bank from liquidity risk.

23

Islamic Contracts Islamic Contracts ::Mudarabah Mudarabah

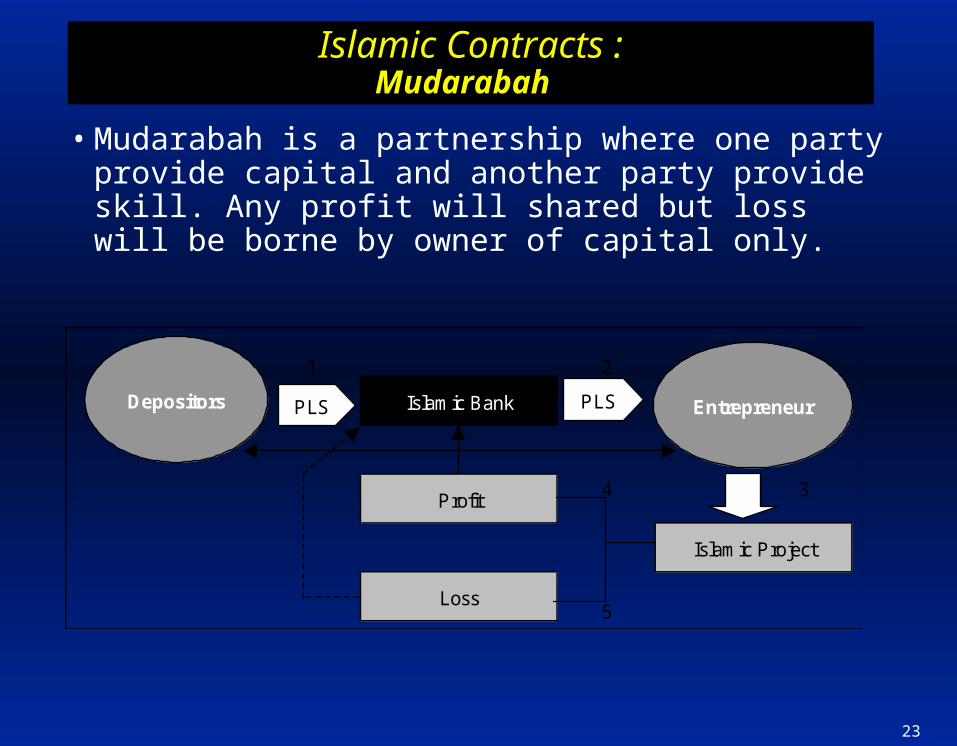

• Mudarabah is a partnership where one party provide capital and another party provide skill. Any profit will shared but loss will be borne by owner of capital only.

1 2

4 3

5

Islamic Bank

Islamic Project

Profit

Loss

Depositors EntrepreneurPLS PLS

24

Islamic Contracts Islamic Contracts ::Mudarabah Mudarabah

• External events like catastrophic and internal business failure might invite operational risk ending with business losses which should be covered by the bank.

• Following it, liquidity of the bank is disturbed (failure to provide cash to depositors) which is liquidity risk.

• Specifically, if mudarib is not capable (skillful) enough to run the business, it can cause credit risk to the bank and because value of the project dropped in the market equity price risk appears.

• Because management of the project can’t be controlled by bank, transparency risk exists.

25

Islamic Contracts Islamic Contracts ::Mudarabah Mudarabah

• To mitigate, bank should be sure the eligibility and capability of the mudarib (business partner).

• Monitoring business performance and balance sheet of company might lessen credit risk.

• Accurately measuring, predicting and anticipating market risk are some ideas to tackle market risk issue in this case.

• Providing capital adequacy and internal reserve are also tools to prevent liquidity risk in Mudarabah contract.

26

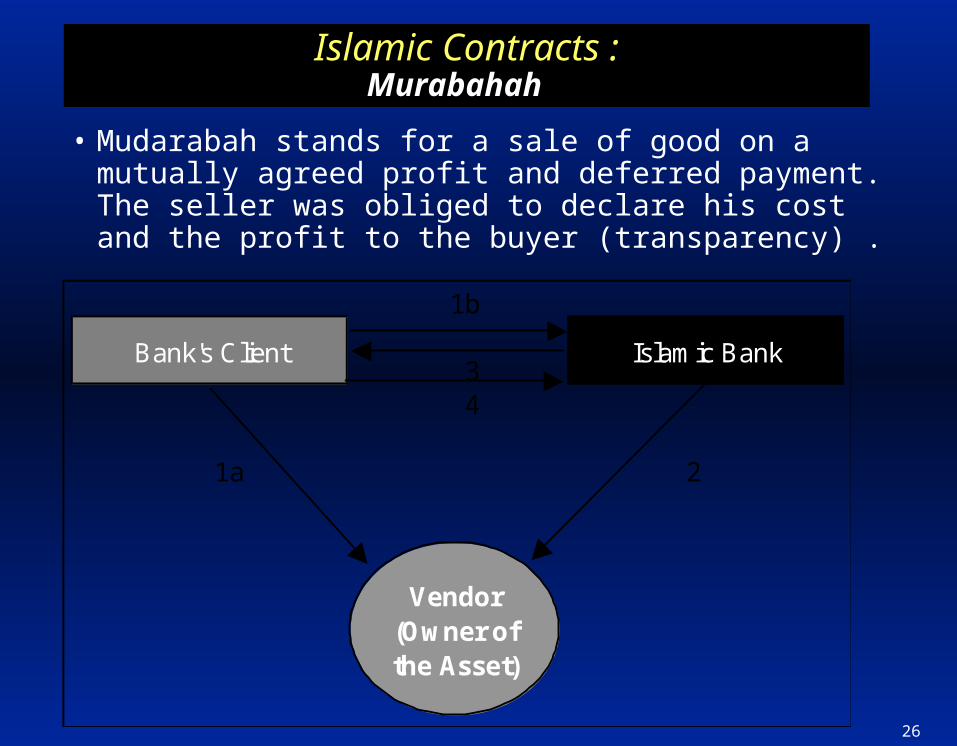

Islamic Contracts Islamic Contracts ::Murabahah Murabahah

• Mudarabah stands for a sale of good on a mutually agreed profit and deferred payment. The seller was obliged to declare his cost and the profit to the buyer (transparency) .

1b

34

1a 2

Bank's Client Islamic Bank

Vendor (Owner of the Asset)

27

Islamic Contracts Islamic Contracts ::Murabahah Murabahah

• Client promises to buy asset under wa’ad contract (unbinding) so it might lead to operational risk or asset risk if he/she declines to buy.

• Before asset being sold to client, bank is responsible for any risk of the asset such as market risk, risk of loss, damage, etc.

• If mark up price is not accurately determined, it may cause mark up risk. At the end or during payment period of Murabahah, the bank faces commodity price risk and market risk.

• When client (buyer) fails to pay the installment, credit risk comes and if he/she is default, price and market risk bear the bank when the asset is sold to market.

• Further, such difficult situation will end up with credit liquidity risk, withdrawal risk and bank rush.

28

Islamic Contracts Islamic Contracts ::Murabahah Murabahah

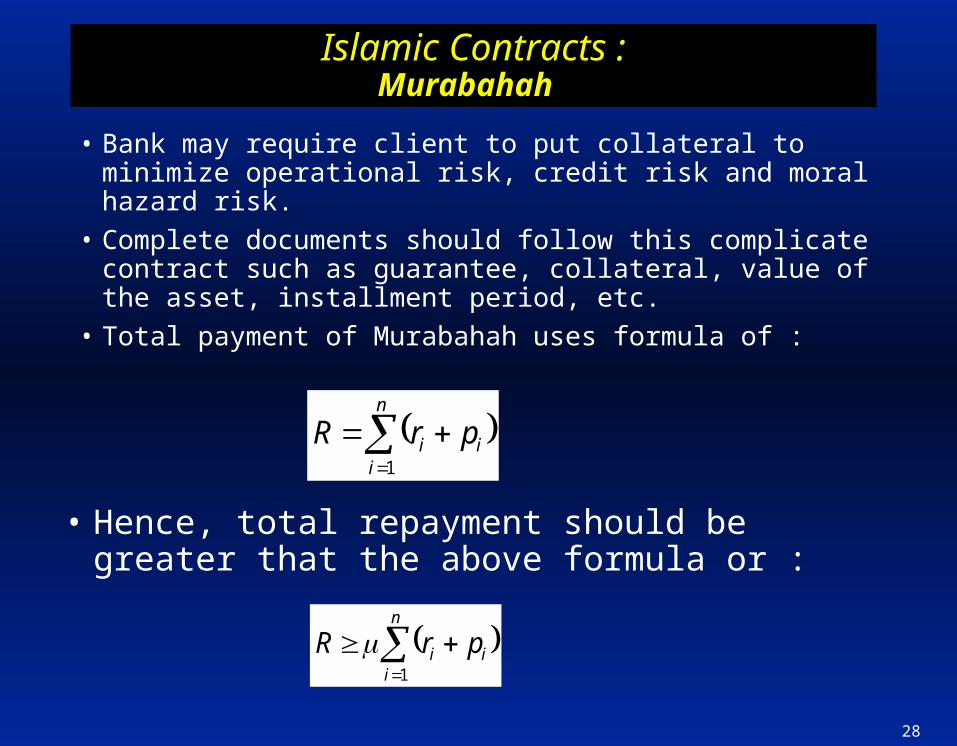

• Bank may require client to put collateral to minimize operational risk, credit risk and moral hazard risk.

• Complete documents should follow this complicate contract such as guarantee, collateral, value of the asset, installment period, etc.

• Total payment of Murabahah uses formula of :

n

iii prR

1

• Hence, total repayment should be greater that the above formula or :

n

iii prR

1

29

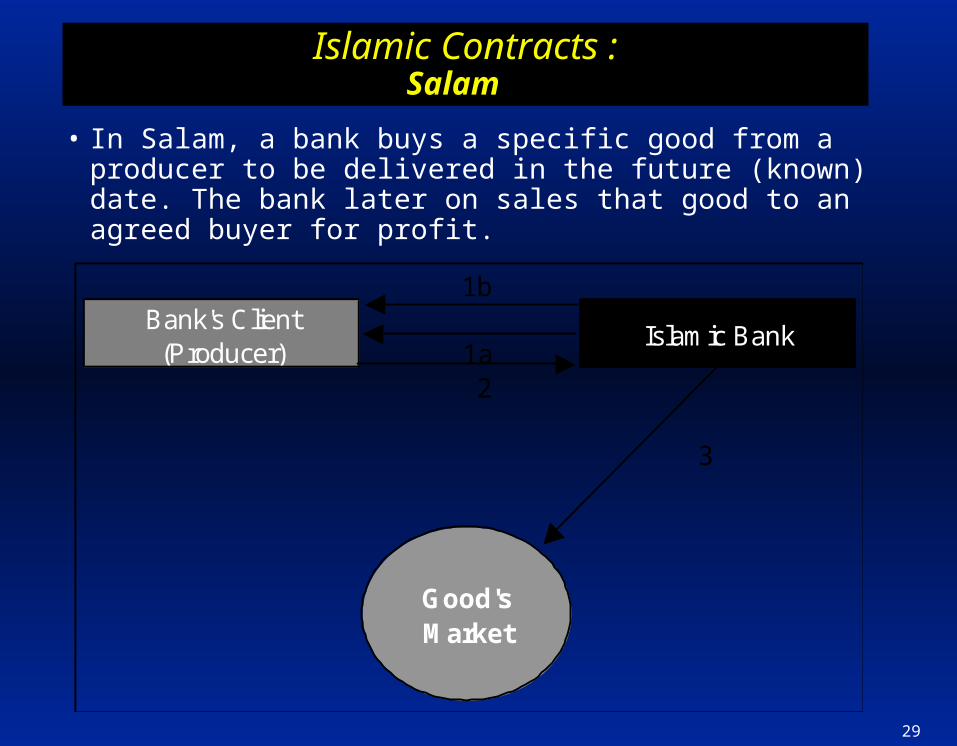

Islamic Contracts Islamic Contracts ::Salam Salam

• In Salam, a bank buys a specific good from a producer to be delivered in the future (known) date. The bank later on sales that good to an agreed buyer for profit.

1b

1a2

3

Bank's Client (Producer)

Islamic Bank

Good's Market

30

Islamic Contracts Islamic Contracts ::SalamSalam

• External events may cause the seller fail to deliver the good in an agreed date. Operational risk occurs.

• Mismatching between specification of the good requested and the one being made may lead to delay of the finished good. This brings business risk and reputation risk.

• Even though salam price is fixed but the final price of the good still has mark up risk and market risk because of fluctuation in price of commodity.

• In the selling time, if buyer delay/fail to buy the salam good from bank, credit risk and liquidity risk hamper the bank.

31

Islamic Contracts Islamic Contracts ::SalamSalam

• To avoid operational risk, bank may ask the seller to follow standard procedure in making the good and insures the salam object.

• Choosing the respected, well-performed, skillful seller can also be adopted by bank.

• Using quantitative and qualitative approaches to predict probability of seller’s default to deliver the good in agreed time.

• Predicting future market price can minimize mark up risk, price risk and market risk. Technically Value at risk can be employed for such purpose.

• To minimize asset risk (damage risk, loss, etc), bank can (i) ask the seller to directly deliver the good to buyer or; (ii) ask the seller to find candidate buyer.

32

Islamic Contracts Islamic Contracts ::IstishnaIstishna

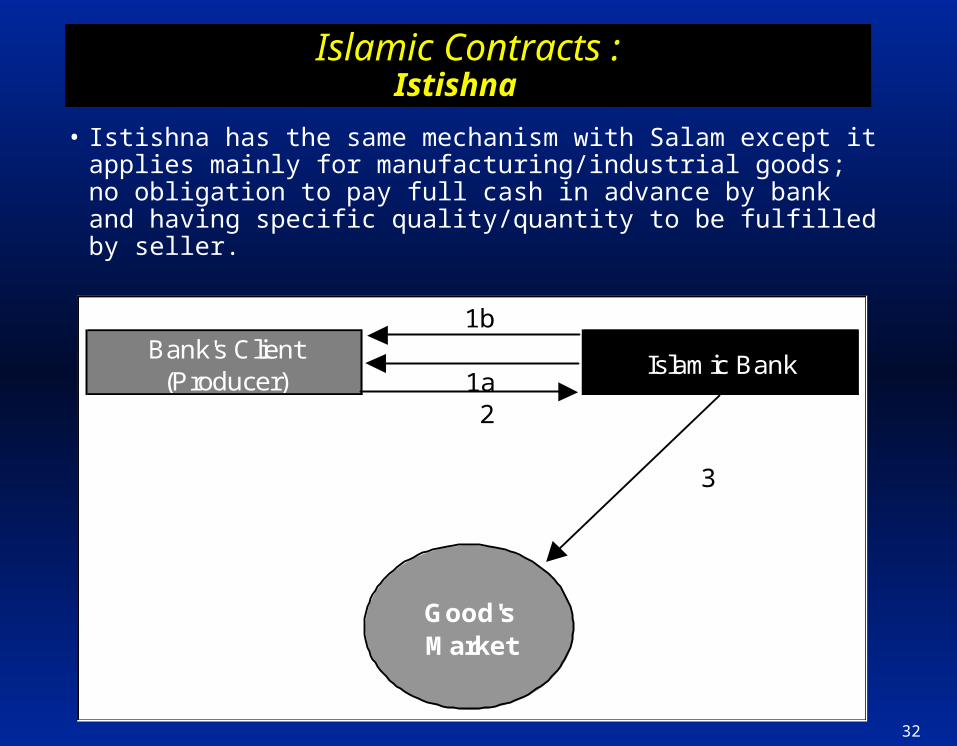

• Istishna has the same mechanism with Salam except it applies mainly for manufacturing/industrial goods; no obligation to pay full cash in advance by bank and having specific quality/quantity to be fulfilled by seller.

1b

1a2

3

Bank's Client (Producer)

Islamic Bank

Good's Market

33

Islamic Contracts Islamic Contracts ::IstishnaIstishna

• During the construction, it is possible to have disruption in supply of raw material, undesirable construction, wrong construction, etc. This is operational risk which may end up with credit risk.

• In such case, when seller asks for a extra time, bank faces business risk, reputation risk and liquidity risk.

• If seller finally can not make the ordered good, default risk, credit risk, liquidity risk are some potential risks to be borne.

• When actual price of the ordered good fluctuates, it causes price and market risk when the bank receives the good and want to resell it to the buyer.

34

Islamic Contracts Islamic Contracts ::IstishnaIstishna

• Carefully and precisely choose the contractor (seller) is one possible action to prevent operational risk, default risk, moral hazard risk, etc.

• Insuring the manufactured good can also be taken into account.

• During the construction process, coordination, intensive monitoring, effective communication, and cooperation are among activities which can minimize risk of product defect, failure, etc.

• Reserving some capital (internal liquidity) for the sake of managing liquidity withdrawal from depositors is another policy to solve liquidity risk.

• Join contract among Islamic banks to order a good under Istishna basis will also lessen risk of default, etc.

35

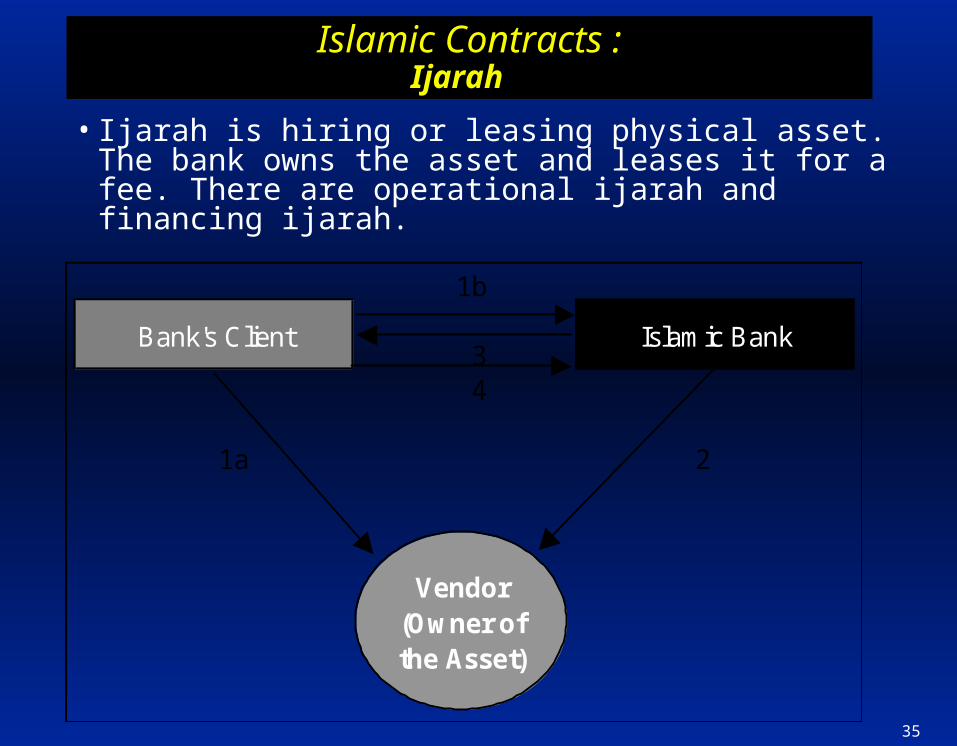

Islamic Contracts Islamic Contracts ::IjarahIjarah

• Ijarah is hiring or leasing physical asset. The bank owns the asset and leases it for a fee. There are operational ijarah and financing ijarah.

1b

34

1a 2

Bank's Client Islamic Bank

Vendor (Owner of the Asset)

36

Islamic Contracts Islamic Contracts ::IjarahIjarah

• Any default of payment by the lessee may generate credit risk and operational risk.

• There is also commodity price risk and market risk to the asset being rented.

• Any damage/defect in the asset is under responsibility of the bank. It can invite moral hazard risk and personal risk.

• Rate of return risk appears when determination of ijarah fee is not appropriately calculated.

• In ijarah muntahia bitamlik/ ijarah tumma al baik/ijarah wa iqtina, the lessee and lessor bear market risk when settling the asset at the end of ijarah period.

37

Islamic Contracts Islamic Contracts ::IjarahIjarah

• Accurately measuring the value of the asset and rental rate. Since rental rate can be adjusted, bank has to determine it precisely.

• Insuring the asset and monitoring the usage of the asset might be lowering moral hazard risk, credit risk, operational risk, etc.

• Estimating future market price may allow Islamic bank to anticipate market risk.

• Financing lease by mechanism prevents Islamic bank from asset risk (damage, loss, defect, etc) but it needs more effort compared to operational lease.

38

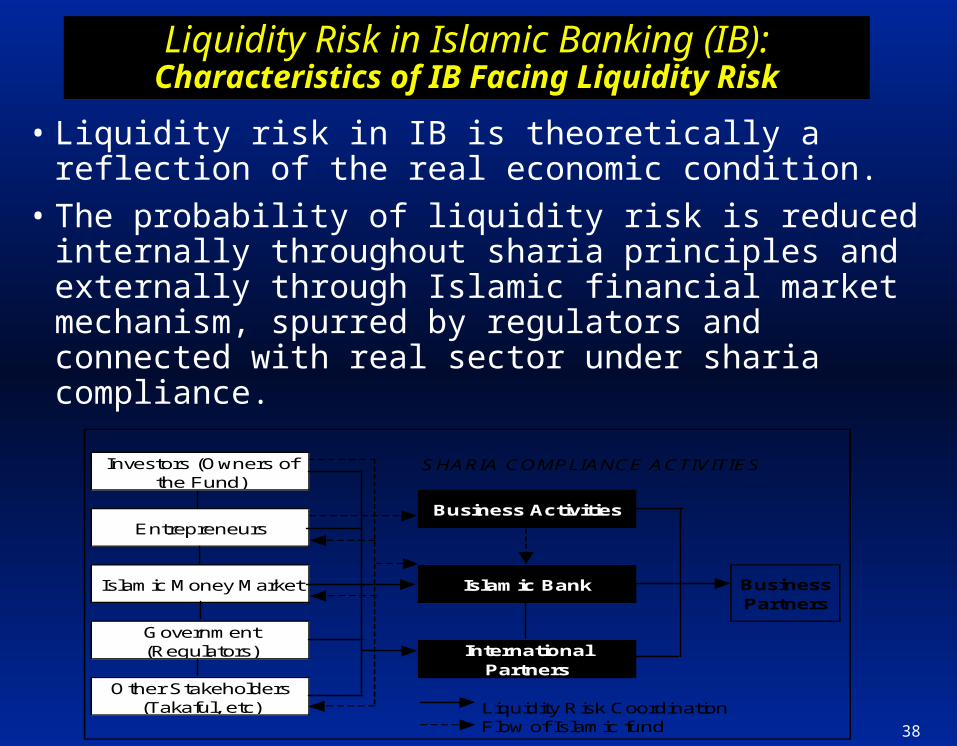

Liquidity Risk in Islamic Banking (IB):Liquidity Risk in Islamic Banking (IB):Characteristics of IB Facing Liquidity RiskCharacteristics of IB Facing Liquidity Risk

• Liquidity risk in IB is theoretically a reflection of the real economic condition.

• The probability of liquidity risk is reduced internally throughout sharia principles and externally through Islamic financial market mechanism, spurred by regulators and connected with real sector under sharia compliance.

SHARIA COMPLIANCE ACTIVITIES

Liquidity Risk Coordination Flow of Islamic fund

Business Partners

Investors (Owners of the Fund)

Islamic Bank

Entrepreneurs

Islamic Money Market

Government (Regulators)

Other Stakeholders (Takaful, etc)

Business Activities

International Partners

39

Liquidity Risk in Islamic Banking (IB):Liquidity Risk in Islamic Banking (IB):Characteristics of IB Facing Liquidity RiskCharacteristics of IB Facing Liquidity Risk

• Islamic bank ties its financing contract with real asset and this is typically another unique attribute of its operation.

• As a result, they face commodity risk such as price risk, asset loose, amortization, etc that could all interrupt asset side and end up with asset liability imbalances.

• Therefore, in Islamic banking, liquidity risk can happen as a result of attaching financing contract with real asset, which is not a typical conventional business transaction.

40

Liquidity Risk in Islamic Banking (IB):Liquidity Risk in Islamic Banking (IB):IB Risk Related to Liquidity ManagementIB Risk Related to Liquidity Management

• IB is expected to see its liquidity risk from holistic perspective (IFSB) due to current economic condition and interconnection among financial and business risk.

• Financing risk in IB exposes direct loss to asset or liabilities followed by asset liability mismatch risk and liquidity run risk. As Islamic bank replaces lending with investment and partnership terminology. Credit risk (part of financing risk) becomes another problem to be anticipated.

• Market risk and commodity risk such as mark up risk, price risk, leased asset value risk, securities price risk and foreign exchange risk.

• Business risk, which incorporates rate of return risk, displaced commercial risk, withdrawal risk and treasury risk.

41

Liquidity Risk in Islamic Banking (IB):Liquidity Risk in Islamic Banking (IB):IB Risk Related to Liquidity ManagementIB Risk Related to Liquidity Management

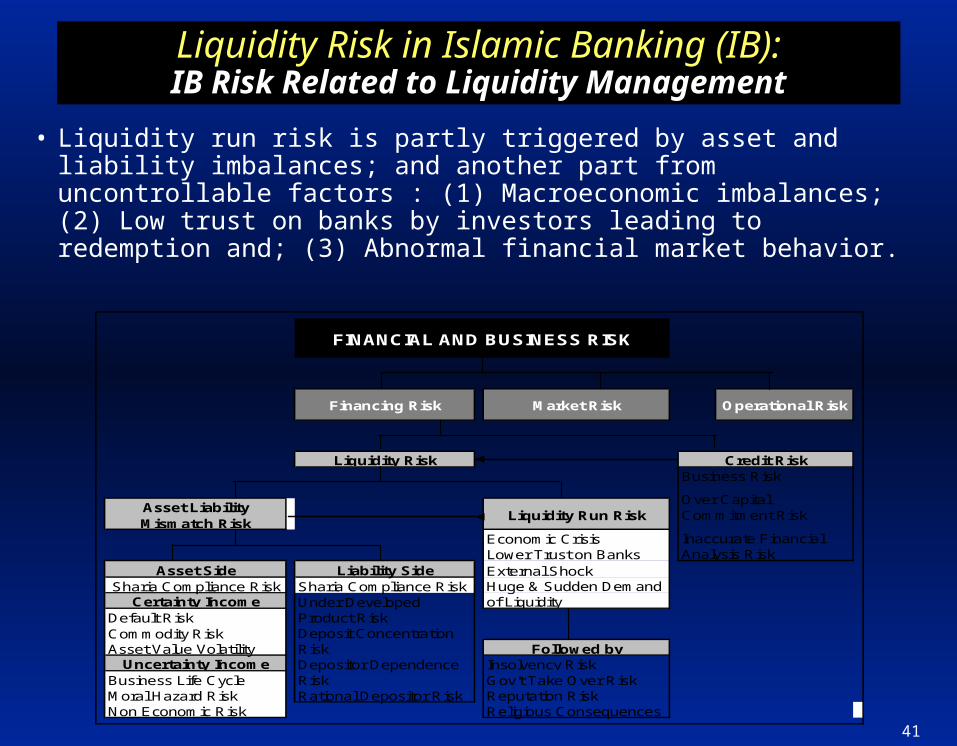

• Liquidity run risk is partly triggered by asset and liability imbalances; and another part from uncontrollable factors : (1) Macroeconomic imbalances; (2) Low trust on banks by investors leading to redemption and; (3) Abnormal financial market behavior.

Liquidity Risk

Asset Liability Mismatch Risk

Liquidity Run Risk

Economic Crisis Lower Trust on Banks

Asset Side Liability Side External Shock Sharia Compliance Risk Sharia Compliance Risk

Certainty IncomeDefault RiskCommodity RiskAsset Value Volatility Followed by

Uncertainty Income Insolvency RiskBusiness Life Cycle Gov't Take Over RiskMoral Hazard Risk Rational Depositor Risk Reputation RiskNon Economic Risk Religious Consequences

Over Capital Commitment Risk

Under Developed Product RiskDeposit Concentration Risk

Inaccurate Financial Analysis Risk

Depositor Dependence Risk

Financing Risk Market Risk

FINANCIAL AND BUSINESS RISK

Huge & Sudden Demand of Liquidity

Operational Risk

Credit RiskBusiness Risk

42

Liquidity Risk in Islamic Banking (IB):Liquidity Risk in Islamic Banking (IB):IB Risk Related to Liquidity ManagementIB Risk Related to Liquidity Management

• Reputation risk arising from failure in governance, business strategy and process; government takes over risk; up into the risk of religious consequences .

• Persistent asset liabilities mismatches should be traced seriously. In liability side, it emerges in under developed banking products; specific time deposit concentration; reliance on big investors; rational depositors consequences.

• In asset side, if there are disturbances in both certainty and uncertainty financing. Certainty income, for example, Murabahah financing is very sensitive to its long term deferred payment; Ijarah has problems of assets being leased; Bay Salam and Bay Istisna have problems of non-deliverable objects or drop of objects’ price risk.

43

Liquidity Risk in Islamic Banking (IB):Liquidity Risk in Islamic Banking (IB):IB Risk Related to Liquidity ManagementIB Risk Related to Liquidity Management

• Uncertainty income is determined by business risk such as changes in market, counter parties, product and economic/political environment.

• Fortunately, sharia equips Islamic bank with the profit and loss sharing concept that potentially reduces a deep loss of liquidity risk when it occurs (Alsayed, 2007:1).

44

Sharia Approaches on Liquidity Risk:Sharia Approaches on Liquidity Risk:Challenges Related to Liquidity Challenges Related to Liquidity

ManagementManagement

• From liability side: the requirement to maintain adequate liquidity as a standby reserve. It contains two modes of reserves, namely cash reserve requirement in the central bank and statutory liquidity requirement in the bank itself .

• Another type of liquidity reserved for such purpose is placement in money market instrument essentially the very short-term basis. Usually, the instruments take form of debt based such as Murabahah inter bank or equity based such as Musharakah and Mudarabah inter bank and ready to be liquidated whenever the bank needs.

45

Sharia Approaches on Liquidity Risk:Sharia Approaches on Liquidity Risk:Challenges Related to Liquidity Challenges Related to Liquidity

ManagementManagement

• From asset side: Islamic bank tends to allocate fund in just short-term investment basis (Gafoor, 1995:8). Even, in the short investment period, Islamic bank prefers debt based Islamic financing to equity based.

• The necessary challenge appears in the case of default by business partners because Islamic bank is prohibited from charging any accrued interest or imposing any penalty .

• The other challenges are lack of easily liquidated long-term investment, immature financial market, etc.

46

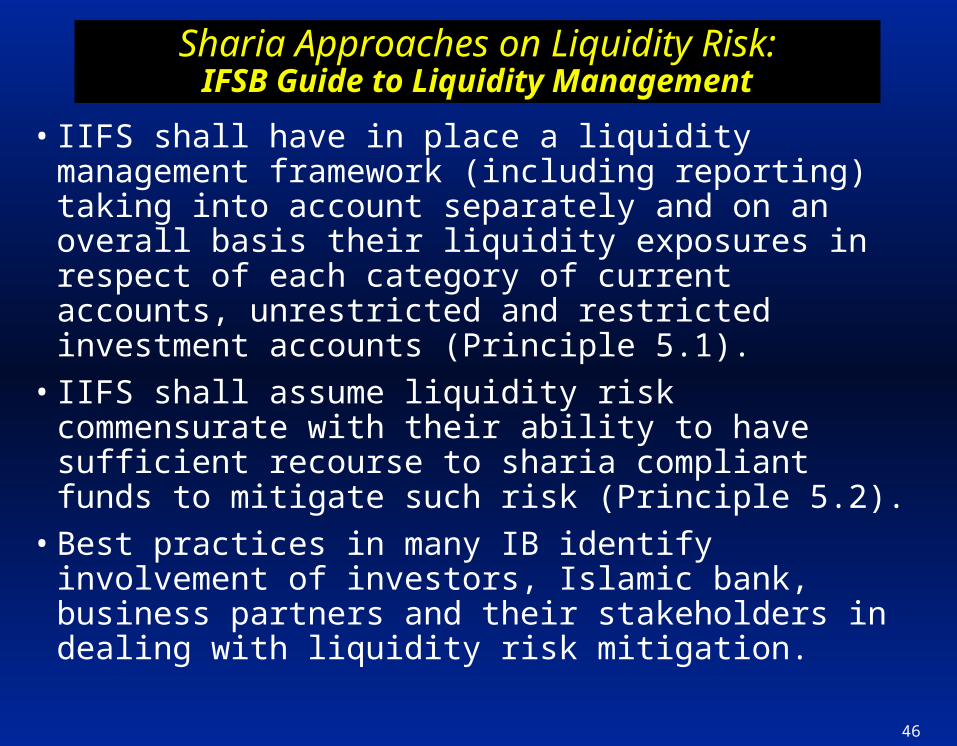

Sharia Approaches on Liquidity Risk:Sharia Approaches on Liquidity Risk:IFSB Guide to Liquidity ManagementIFSB Guide to Liquidity Management

• IIFS shall have in place a liquidity management framework (including reporting) taking into account separately and on an overall basis their liquidity exposures in respect of each category of current accounts, unrestricted and restricted investment accounts (Principle 5.1).

• IIFS shall assume liquidity risk commensurate with their ability to have sufficient recourse to sharia compliant funds to mitigate such risk (Principle 5.2).

• Best practices in many IB identify involvement of investors, Islamic bank, business partners and their stakeholders in dealing with liquidity risk mitigation.

47

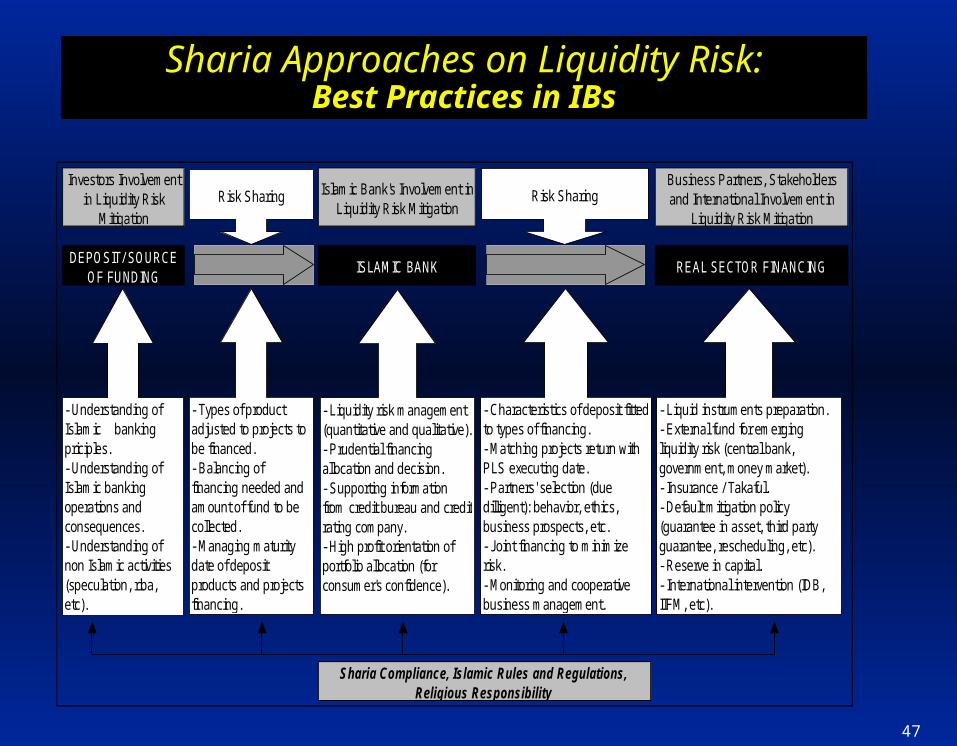

Sharia Approaches on Liquidity Risk:Sharia Approaches on Liquidity Risk:Best Practices in IBsBest Practices in IBs

Business Partners, Stakeholders and International Involvement in

Liquidity Risk Mitigation

Sharia Compliance, Islamic Rules and Regulations, Religious Responsibility

Investors Involvement in Liquidity Risk

Mitigation

Islamic Bank's Involvement in Liquidity Risk Mitigation

DEPOSIT/ SOURCE OF FUNDING

ISLAMIC BANK REAL SECTOR FINANCING

Risk Sharing

- Understanding of Islamic banking priciples.- Understanding of Islamic banking operations and consequences.- Understanding of non Islamic activities (speculation, riba, etc).

- Types of product adjusted to projects to be financed.- Balancing of financing needed and amount of fund to be collected.- Managing maturity date of deposit products and projects financing.

- Liquidity risk management (quantitative and qualitative).- Prudential financing allocation and decision.- Supporting information from credit bureau and credit rating company.- High profit orientation of portfolio allocation (for consumer's confidence).

- Characteristics of deposit fitted to types of financing.- Matching projects return with PLS executing date.- Partners' selection (due dilligent): behavior, ethics, business prospects, etc. - Joint financing to minimize risk.- Monitoring and cooperative business management.

Risk Sharing

- Liquid instruments preparation.- External fund for emerging liquidity risk (central bank, government, money market).- Insurance / Takaful.- Default mitigation policy (guarantee in asset, third party guarantee, rescheduling, etc).- Reserve in capital. - International intervention (IDB, IIFM, etc).

48

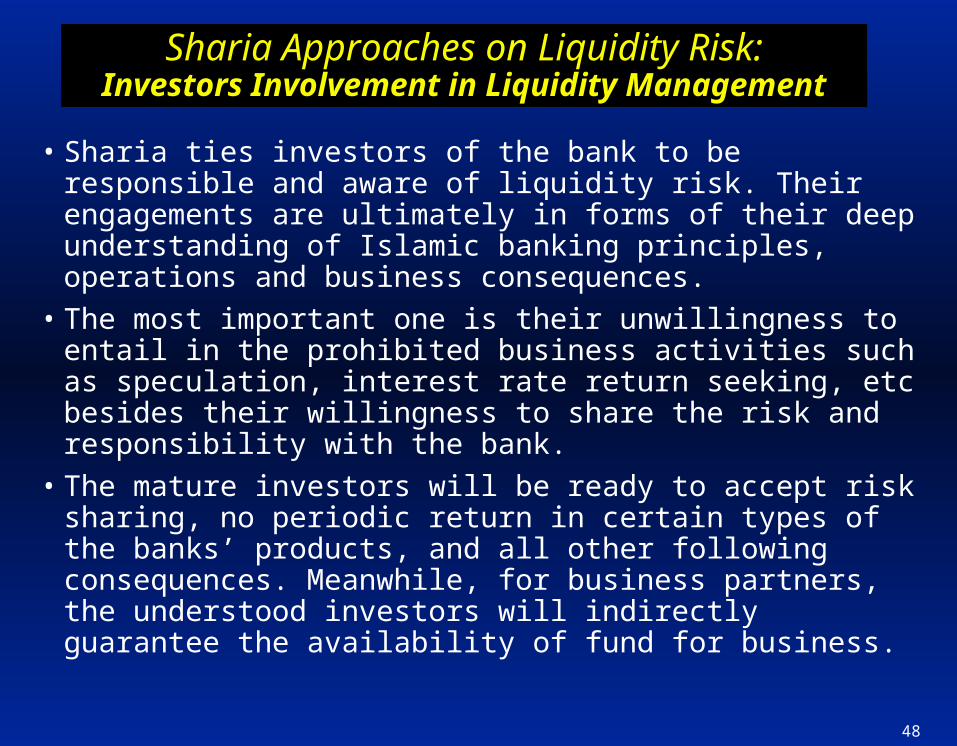

Sharia Approaches on Liquidity Risk:Sharia Approaches on Liquidity Risk:Investors Involvement in Liquidity Investors Involvement in Liquidity

ManagementManagement

• Sharia ties investors of the bank to be responsible and aware of liquidity risk. Their engagements are ultimately in forms of their deep understanding of Islamic banking principles, operations and business consequences.

• The most important one is their unwillingness to entail in the prohibited business activities such as speculation, interest rate return seeking, etc besides their willingness to share the risk and responsibility with the bank.

• The mature investors will be ready to accept risk sharing, no periodic return in certain types of the banks’ products, and all other following consequences. Meanwhile, for business partners, the understood investors will indirectly guarantee the availability of fund for business.

49

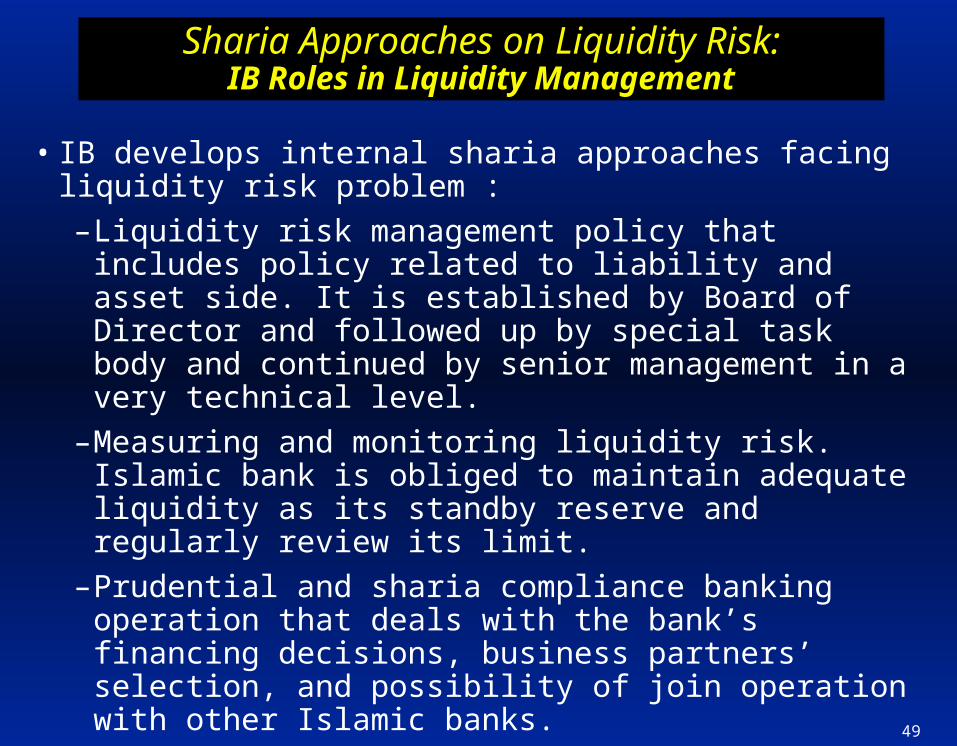

Sharia Approaches on Liquidity Risk:Sharia Approaches on Liquidity Risk:IB Roles in Liquidity ManagementIB Roles in Liquidity Management

• IB develops internal sharia approaches facing liquidity risk problem :

– Liquidity risk management policy that includes policy related to liability and asset side. It is established by Board of Director and followed up by special task body and continued by senior management in a very technical level.

– Measuring and monitoring liquidity risk. Islamic bank is obliged to maintain adequate liquidity as its standby reserve and regularly review its limit.

– Prudential and sharia compliance banking operation that deals with the bank’s financing decisions, business partners’ selection, and possibility of join operation with other Islamic banks.

50

Sharia Approaches on Liquidity Risk:Sharia Approaches on Liquidity Risk:IB Roles in Liquidity ManagementIB Roles in Liquidity Management

– Sharia based liability management. IB follows three approaches, (a) Adjusting types of deposit products into projects to be financed; (b) Balancing of financing needed and amount to be collected and; (c) Managing maturity date of both deposit products and projects financing.

– Sharia based asset management. IB approaches are, (a) Fitting characteristics of deposit and projects financing; (b) Matching the flow of projects’ return with the due date of PLS payment; (c) Selecting business partners through due diligence; (d) Employing joint financing with other Islamic banks to share the risk and; (e) Monitoring and conducting cooperative business

51

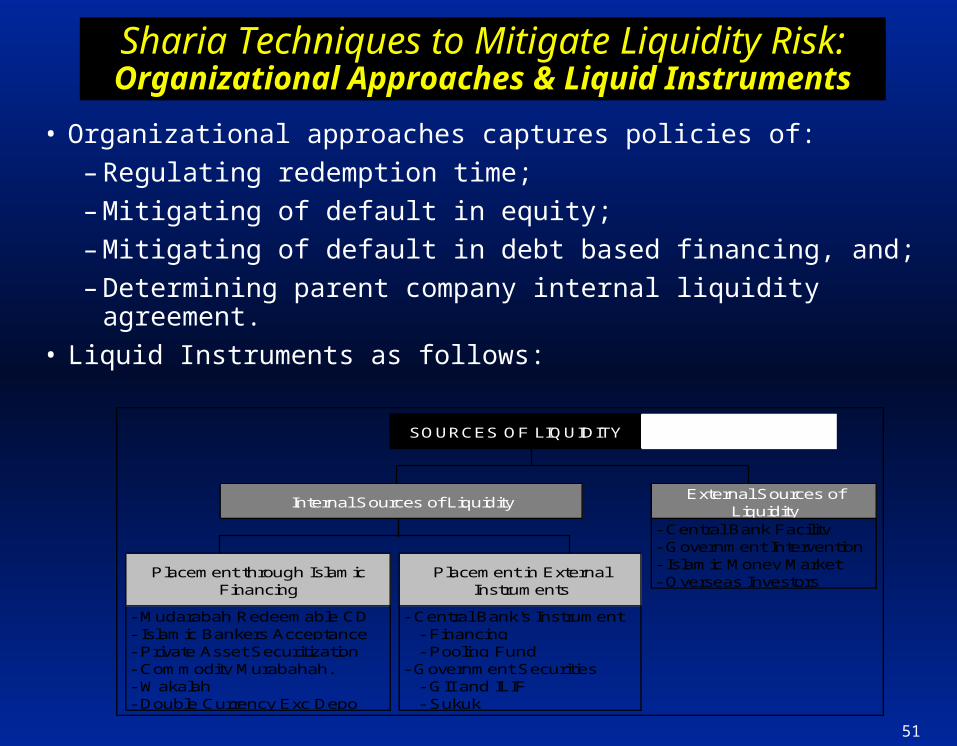

Sharia Techniques to Mitigate Liquidity Sharia Techniques to Mitigate Liquidity Risk:Risk:

Organizational Approaches & Liquid Organizational Approaches & Liquid InstrumentsInstruments

• Organizational approaches captures policies of:

– Regulating redemption time;

– Mitigating of default in equity;

– Mitigating of default in debt based financing, and;

– Determining parent company internal liquidity agreement.

• Liquid Instruments as follows:

- Overseas Investors

- Double Currency Exc Depo - Sukuk- Wakalah

Internal Sources of Liquidity

- Central Bank's Instrument - Financing - Pooling Fund- Government Securities - GII and ILIF

- Mudarabah Redeemable CD

- Commodity Murabahah.

External Sources of Liquidity

Placement through Islamic Financing

Placement in External Instruments

- Central Bank Facility

- Islamic Money Market

SOURCES OF LIQUIDITY

- Government Intervention

- Islamic Bankers Acceptance- Private Asset Securitization

52

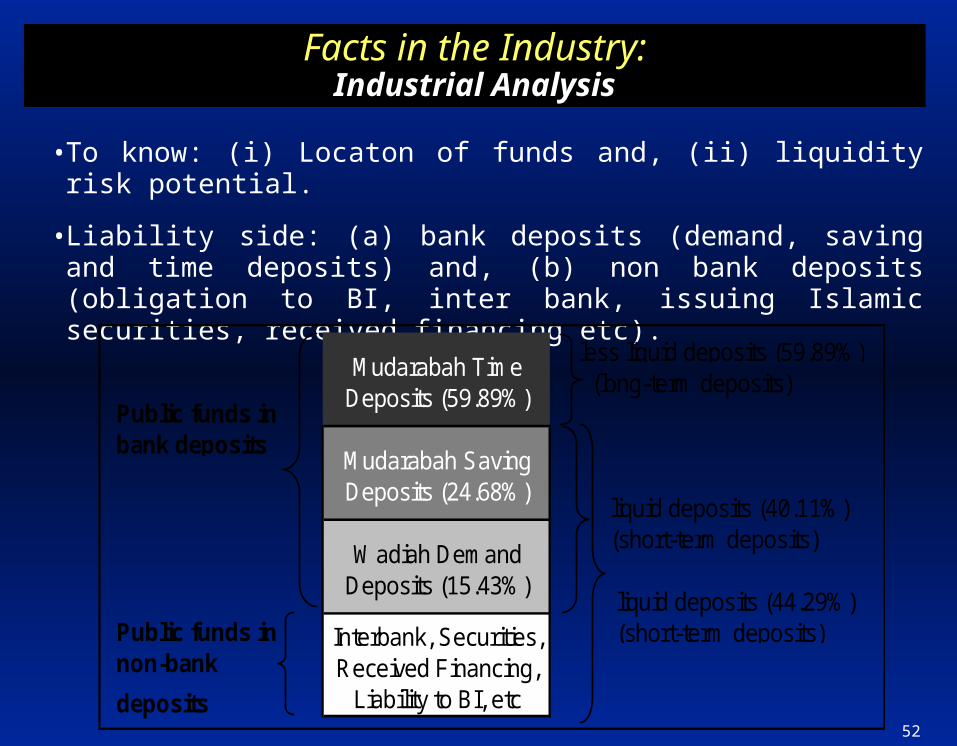

• To know: (i) Locaton of funds and, (ii) liquidity risk potential.

• Liability side: (a) bank deposits (demand, saving and time deposits) and, (b) non bank deposits (obligation to BI, inter bank, issuing Islamic securities, received financing etc).

less liquid deposits (59.89%) (long-term deposits)

Public funds in bank deposits

liquid deposits (40.11%) (short-term deposits)

liquid deposits (44.29%)Public funds in (short-term deposits)non-bank

deposits

Mudarabah Saving Deposits (24.68%)

Wadiah Demand Deposits (15.43%)

Interbank, Securities, Received Financing,

Liability to BI, etc

Mudarabah Time Deposits (59.89%)

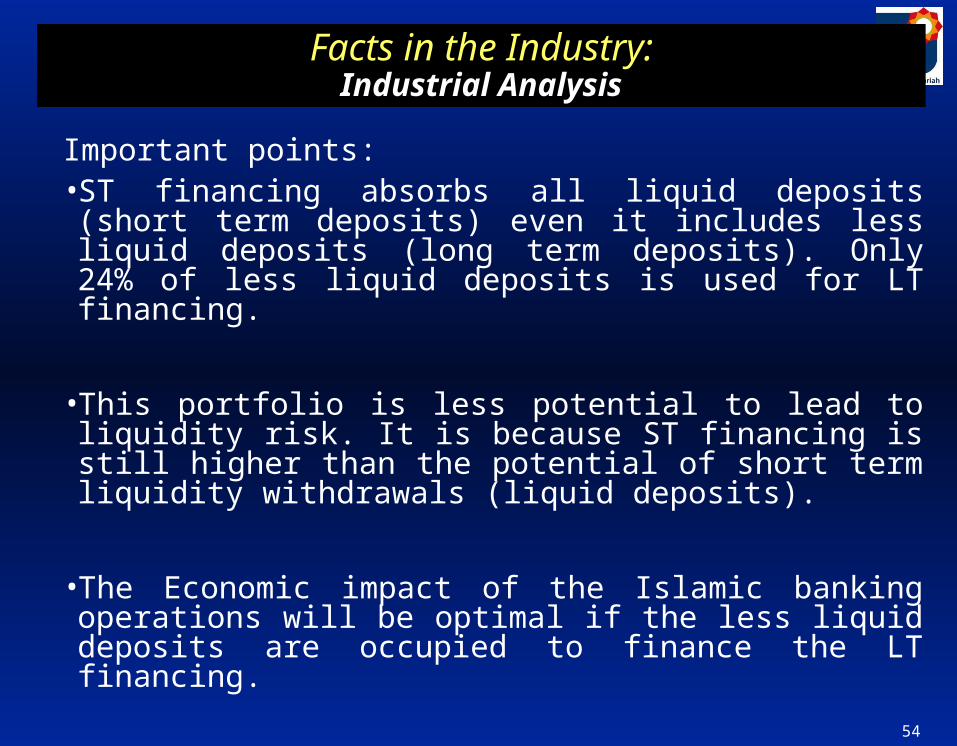

Facts in the IndustryFacts in the Industry::Industrial AnalysisIndustrial Analysis

53

Facts in the IndustryFacts in the Industry::Industrial AnalysisIndustrial Analysis

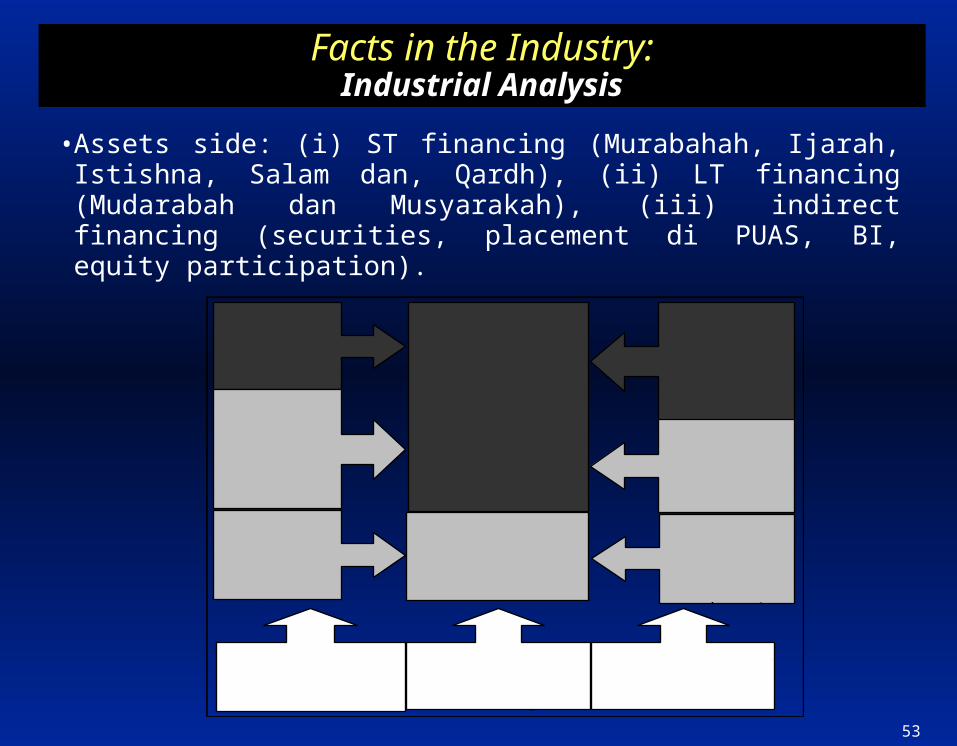

• Assets side: (i) ST financing (Murabahah, Ijarah, Istishna, Salam dan, Qardh), (ii) LT financing (Mudarabah dan Musyarakah), (iii) indirect financing (securities, placement di PUAS, BI, equity participation).

Short-Term Deposits (40%

of total deposits)

Long-Term Deposits (36%

of total deposits)

Long-Term Deposits (24%

of total deposits)

Short-Term Financing (76% of total

financing)

Long-Term Financing (24% of total

financing)

Short-Term Deposits (44%

of total deposits)

Long-Term Deposits (32%

of total deposits)

Long-Term Deposits (24%

of total deposits)

Public Funds in Banks Deposits + Non Banks' Deposits

Public Funds in Banks' Deposit

Total Direct Financings + Indirect

Financing

54

Facts in the IndustryFacts in the Industry::Industrial AnalysisIndustrial Analysis

Important points: • ST financing absorbs all liquid deposits (short term deposits) even it includes less liquid deposits (long term deposits). Only 24% of less liquid deposits is used for LT financing.

• This portfolio is less potential to lead to liquidity risk. It is because ST financing is still higher than the potential of short term liquidity withdrawals (liquid deposits).

• The Economic impact of the Islamic banking operations will be optimal if the less liquid deposits are occupied to finance the LT financing.

55

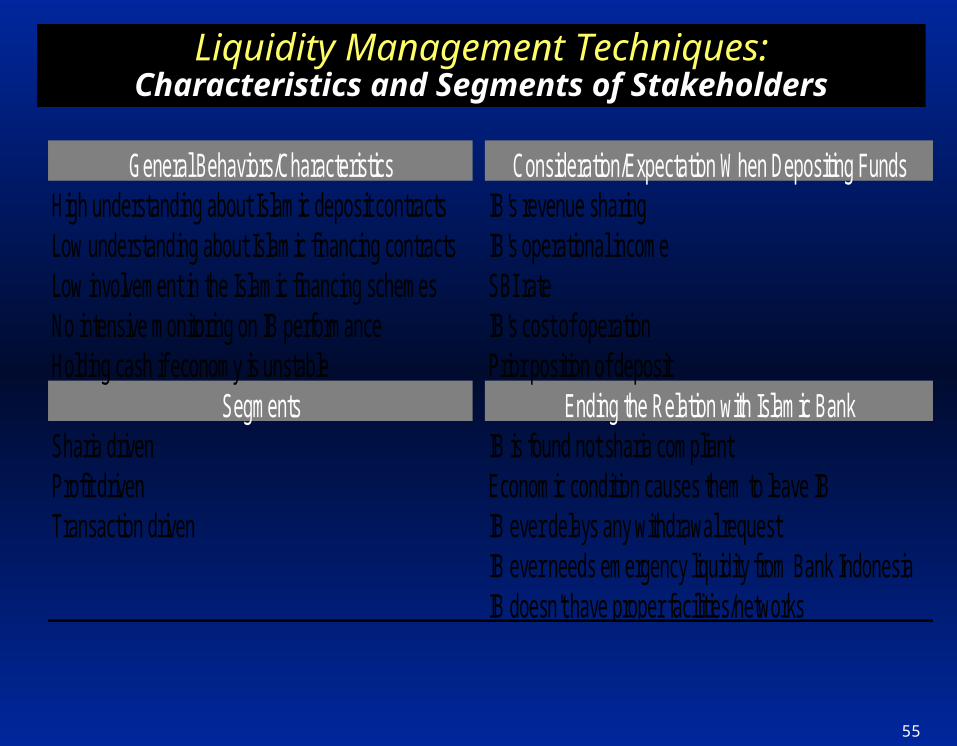

Liquidity ManagementLiquidity Management Techniques: Techniques:Characteristics and Segments of StakeholdersCharacteristics and Segments of Stakeholders

General Behaviors/Characteristics Consideration/Expectation When Depositing FundsHigh understanding about Islamic deposit contracts IB's revenue sharingLow understanding about Islamic financing contracts IB's operational incomeLow involvement in the Islamic financing schemes SBI rateNo intensive monitoring on IB performance IB's cost of operationHolding cash if economy is unstable Prior position of deposit

Segments Ending the Relation with Islamic BankSharia driven IB is found not sharia compliantProfit driven Economic condition causes them to leave IBTransaction driven IB ever delays any withdrawal request

IB ever needs emergency liquidity from Bank IndonesiaIB doesn't have proper facilities/networks

56

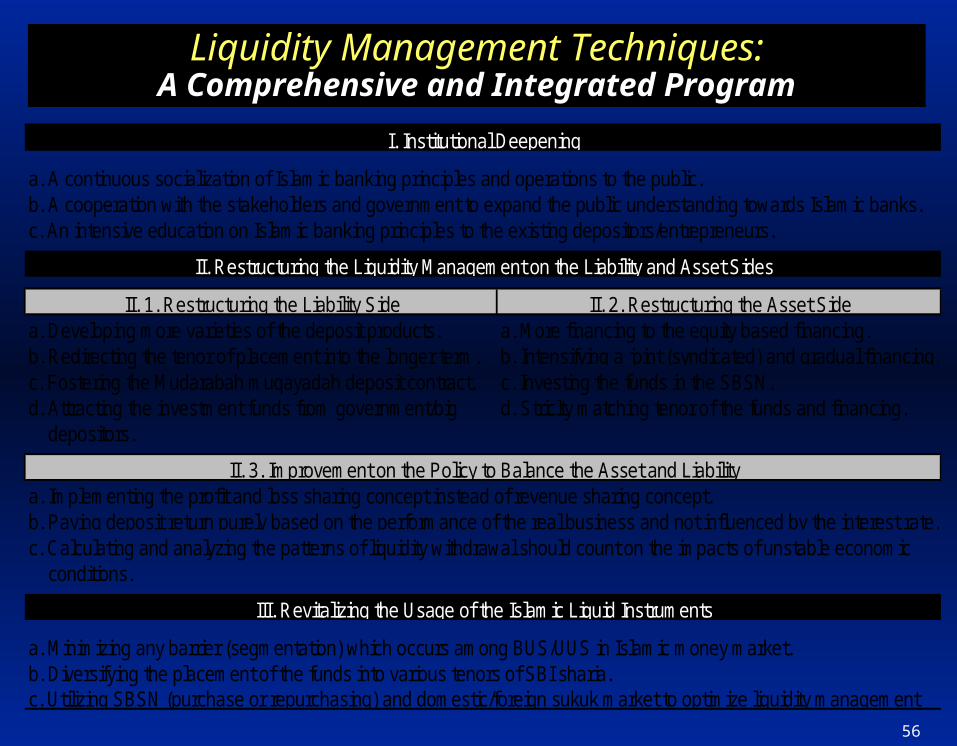

Liquidity ManagementLiquidity Management Techniques: Techniques:A Comprehensive and Integrated ProgramA Comprehensive and Integrated Program

a. A continuous socialization of Islamic banking principles and operations to the public.b. A cooperation with the stakeholders and government to expand the public understanding towards Islamic banks.c. An intensive education on Islamic banking principles to the existing depositors/entrepreneurs.

a. Developing more varieties of the deposit products. a. More financing to the equity based financing.b. Redirecting the tenor of placement into the longer term. b. Intensifying a joint (syndicated) and gradual financing.c. Fostering the Mudarabah muqayadah deposit contract. c. Investing the funds in the SBSN.d. Attracting the investment funds from government/big d. Striclty matching tenor of the funds and financing. depositors.

a. Implementing the profit and loss sharing concept instead of revenue sharing concept.b. Paying deposit return purely based on the performance of the real business and not influenced by the interest rate.c. Calculating and analyzing the patterns of liquidity withdrawal should count on the impacts of unstable economic conditions.

a. Minimizing any barrier (segmentation) which occurs among BUS/UUS in Islamic money market.b. Diversifying the placement of the funds into various tenors of SBI sharia.c. Utilizing SBSN (purchase or repurchasing) and domestic/foreign sukuk market to optimize liquidity management

III. Revitalizing the Usage of the Islamic Liquid Instruments

II. 3. Improvement on the Policy to Balance the Asset and Liability

I. Institutional Deepening

II. Restructuring the Liquidity Management on the Liability and Asset Sides

II. 1. Restructuring the Liability Side II. 2. Restructuring the Asset Side